Buying your next home?

See our home loan tools, articles and resources to help you explore your home loan options. We'll help you get to a good place.

3-minute read

Get closer to your savings goals. Here are some tips to help speed up your journey.

Create separate savings accounts for your short term goals, a house deposit and holidays as well as one for bills and set up automatic transfers from your everyday account to make saving automatic.

When you have a decent sum of money saved up, use a term deposit to lock it away until the term ends. This could remove the temptation to access your money.

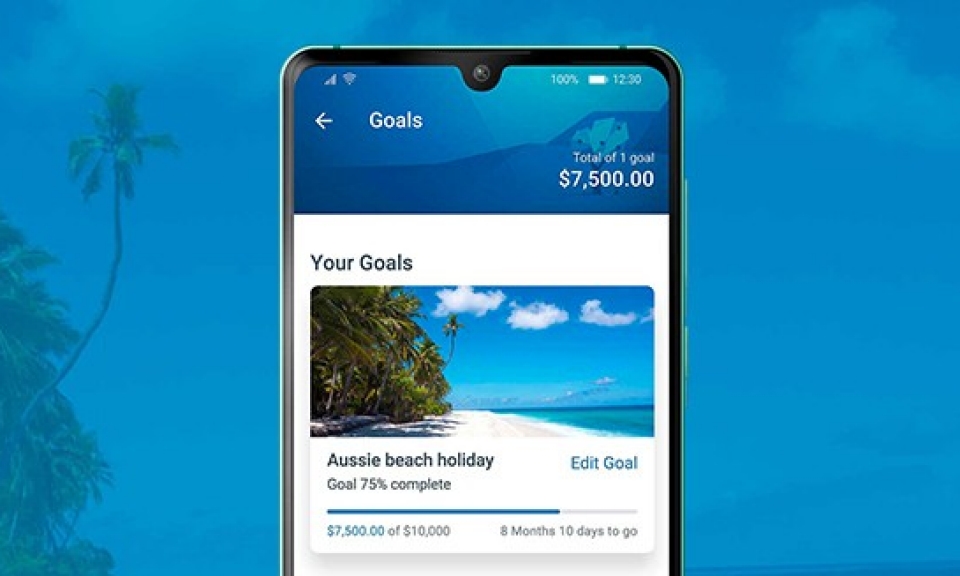

Saving for something? No matter how big or small, it won’t feel so far away when you know what you need to save and how you’re tracking. You can set a goal in the ANZ App on your ANZ Online Saver or ANZ Progress Saver account today.

If you have multiple bank accounts, check what transaction fees you could incur. You can also try asking about fee exemptions or packages for which you might be eligible.

Whether you go for a tried-and-tested thermometer, a pie chart, or a fancy savings app on your phone, tracking your progress can help you keep your eye on the prize.

Keep track of your spending using a diary or a mobile app. Make sure to look at not only your everyday spending but your large bills such as car registration and insurance.

Think about how often you will need to access your savings and how you would like to earn interest. Make sure you consider things like bonus interest offers and incentives for making regular deposits when you choose your accounts.

Talk to someone about whether consolidating existing debts could help you save on interest.

Bill smoothing is a payment plan offered by some utility providers (electricity, gas and water). Instead of being overwhelmed with large bills all at once, you may be able to pay fortnightly or monthly. This may help make budgeting a little easier and align with your pay cycle. On the other hand, in some cases you may pay less if you pay your bill in one hit, so you need to carefully weigh up the pros and cons of each option.

![]()

Make sure to eat before you go shopping so that you don’t end up buying things you don’t need. If you find yourself at the super market with a grumbly tummy, buy a healthy snack such as a piece of fruit or a small tub of nuts before you get started.

Prone to straying from the shopping list for that goody in the candy aisle? Buying online may be the option for you. This could keep you out of the aisles and only buying what you need.

Growing your own food at home may help you to save on those weekly grocery bills.

Swapping out branded products for cheaper generic brands may save money and who knows, you might not even notice the difference.

Swap your soft drinks and juice for tap water to save on your grocery bill.

Buying in bulk is often cheaper than buying small quantities every week. This may be great for cooking large batches of meals and storing in the freezer.

By planning out your menu a week in advance you could reduce the amount of food you throw out. Spend less by minimising the number of times you go to the market and only buying what's on the list.

Meat can cost a lot. Try a meat-free Monday meal or add a few vegetarian meals to your weekly plan.

Try having a yard sale, opening a spot at the local marketplace or selling on Ebay. This will clear out your closet and declutter your home and could put some money into your pocket.

Before clicking ‘checkout’, try waiting a few days. Sometimes you’ll find yourself questioning if you really wanted that dress or realising that you already have that top in a similar design.

Cheap staples such as lentil, rice and pasta can be jazzed up hundreds of different ways with a few simple ingredients. Try looking up recipes online for cheap meal ideas.

Hunt for bargains online or plan your shopping around sales - for example End of Financial Year or Boxing Day sales. You could also plan your gifts in advance or try handmade gifts instead of that expensive wine.

Put a pause on any purchases that are expensive or unnecessary by giving yourself some time to think. If you are shopping online, leave the item in the shopping cart for a day or two.

![]()

Taking the kids to the zoo or aquarium every month can become expensive. Instead, consider exploring new parks or look for free events in your local city. If the trip to the zoo is something the kids really love, consider annual passes as these may work out to be cheaper than single pass trips, provided that you use them.

Buying food can get expensive on the road especially when there aren’t many options and you’re hungry. Packing snacks or even meals saves money on food costs.

If you find that you can never finish your meal, try splitting with a friend or order a set of entrees to share with the group.

Ignore the expensive costume stores and check out the op-shops for cheap inspiration. Or you could grab some cheap trimmings to jazz up an outfit.

Buying lunches at work can cost a lot more than bringing home cooked meals.

![]()

Switch out expensive fun for cheap fun. For instance instead of going to an expensive café for lunch, do a BYO picnic with friends.

Every time you walk past, transfer all your loose change into the jar. To fast-track your savings and make things a little more interesting, you could add a ‘note rule’. Every time your wallet has a note of a certain colour (start easy, with a pink $5 note), then it goes in the jar, too. If you are living a digital lifestyle, set up a daily transfer of $1 every day or $10 a week.

![]()

Identify what triggers (like people, places, occasions, emotions, or thoughts) precede a behaviour you want to change. Using the Friday night $50 spend on dinner after work as an example. Try to change things – for example, you could make a date with a friend outside of work to go see a movie instead. Or, invite your workmates home.

Instead of thinking about how you’re $50 worse off each week because the money is being re-directed into your savings account, think about the round-the-world trip that the $50 is going towards.

The information set out above is general in nature and has been prepared without taking into account your objectives, financial situation or needs. Before acting on the information, you should consider whether the information is appropriate for you having regard to your objectives, financial situation and needs. By providing this information ANZ does not intend to provide any financial advice or other advice or recommendations. You should seek independent financial, legal, tax and other relevant advice having regard to your particular circumstances.