-

New Zealanders felt less financially secure in the three months to September, according to a survey by the country’s largest bank. However, there are reasons to be hopeful about the future.

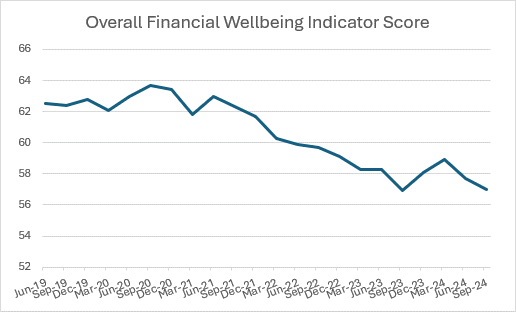

The ANZ Financial Wellbeing Indicator score dropped to 57.0 in the July to September period, down from 57.7 in the previous three months. This score is now close to the low of 56.9 recorded in the same quarter last year.

IMAGE

“This fall comes as no great surprise considering we are at what we hope is the tail end of a recession, and the labour market tends to lag economic activity,” said Grant Knuckey, ANZ Managing Director, Personal.

“We have seen a close correlation between interest rates and the Financial Wellbeing Indicator score, with higher rates driving the score lower.”

The Official Cash Rate (OCR) only started to fall in the middle of the September quarter, decreasing by 0.25 per cent to 5.25 per cent on 14 August. A larger decline of 0.5 per cent occurred on 9 October, after the end of this survey period.

Another interest rate cut is widely predicted in November which will provide further relief to borrowers, though this will depend on the term of their current lending.

A Financial ‘Pulse Check’

The ANZ Financial Wellbeing Index provides an overview of the personal financial wellbeing of New Zealanders and acts as a ‘pulse check’ on how Kiwis feel about their financial situation.

The Indicator Score comprises three components:

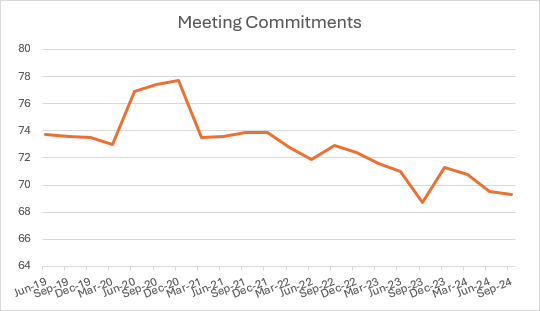

Meeting Commitments: This measures how well people can pay their bills, mortgage or rent, and other living costs. This measure fell in the September quarter, suggesting that many people are still feeling the squeeze of the cost-of-living crisis despite inflation dropping to 2.2% in the third quarter. The score of 69.3 for meeting commitments remains above the low seen at the end of 2023.

IMAGE

The number of people who say they have been keeping track of their money has been steadily climbing over the past two years and hit a fresh high in the September quarter.

While keeping close track of money is beneficial, the fact that more people feel the need to do so suggests ongoing pressure on household budgets.

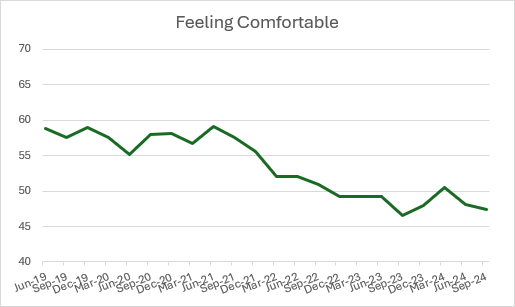

Feeling Comfortable: The second component of the Indicator Score is whether people are feeling comfortable financially—this score also fell.

For many people, the family home is their single largest asset, and house prices have been stagnant. Consumer confidence—while still weak—did pick up slightly over the quarter, but this has yet to impact the ‘feeling comfortable’ metric.

IMAGE

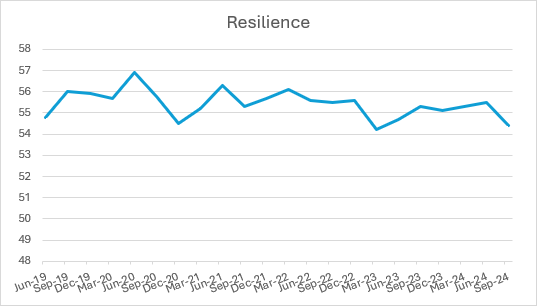

Resilience: The third element of the Indicator Score is resilience. Given the ongoing recession, it’s not surprising to see this dipping.

Employment levels fell, and the median reported savings balance dropped to $4,030 in the September quarter, down around 20 per cent from over $5,000 in the second quarter.

Overall, though, ‘resilience’ has been the most stable indicator, remaining in a narrow band while other indicators trend down.

IMAGE

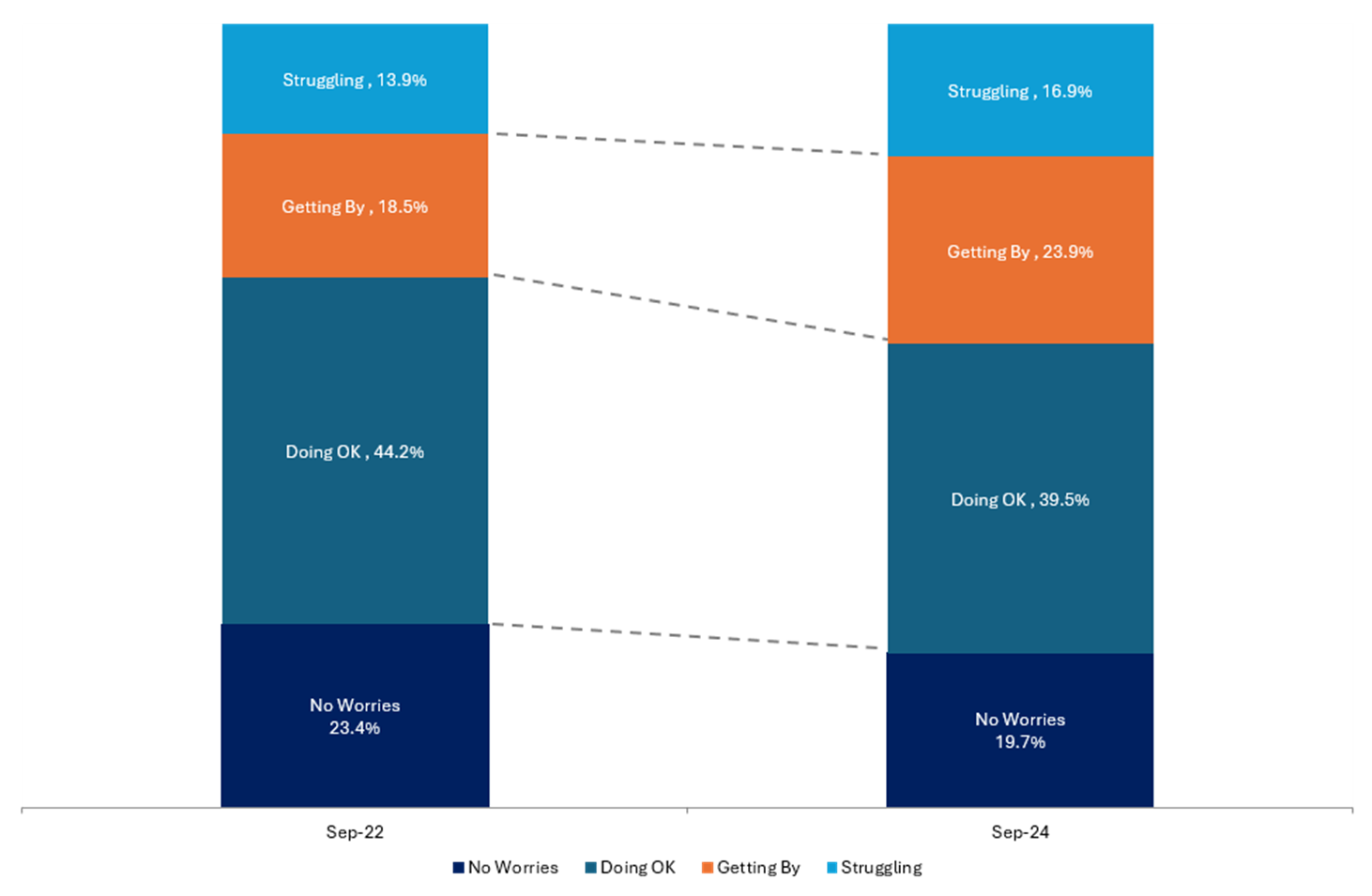

Depending on their financial metrics, people are categorised into four segments: ‘struggling’, ‘getting by’, ‘doing OK’, or ‘no worries.’

Over the past two years, we have seen the composition of the four financial wellbeing segments change for the worse. Both the ‘struggling’ and ‘getting by’ segments have grown significantly, while both the ‘doing OK’ and ‘no worries’ segments have declined.

IMAGE

Looking Forward

There are some signs of improvement in the economy. Interest rates are falling, and firms are seeing light at the end of the tunnel, which hopefully means job losses will start to tail off sooner than otherwise. These declining interest rates also offer many people a way to lift their own financial wellbeing in the meantime.

For those with mortgages, when the time comes for their fixed rates to roll over, they will likely have the opportunity to move onto lower rates. This can provide options: either reduce the maturity date of the loan and pay less each period, freeing up cash, or keep the payment amount the same to pay off the home loan faster, potentially saving thousands in interest over the loan’s course.

If affordable, this is a great way to increase financial wellbeing. It doesn’t have to be an all-or-nothing approach; reducing payments slightly can ease household budget pressure while still paying more than the minimum required with the new interest rate. Every little bit helps.

-

-

-

-

-

Share

anzcomau:newsroom/news/NZ-Consumer

Financial Wellbeing of NZers Declines, Optimism Remains

2024-11-21

/content/dam/anzcomau/news/New-Zealand/2023/September/wellbeing-AI-budget-NZ.jpg

RELATED ARTICLES

-

ANZ NZ is warning customers to be aware of a new text message phishing scam, that exploits vulnerabilities in the aging 2G mobile phone network.

19 August 2024 -

As high energy costs put the squeeze on many of the country’s businesses, ANZ has highlighted the value of long-term investment in clean energy technology.

9 September 2024 -

A 5-year old joining a KiwiSaver scheme today could save $100k by their mid-30s.

31 October 2024