-

Last year, markets finally reclaimed the peak from early 2022 and managed to sustainably hold above this level.

"We believe the world is moving from an extended period of disinflationary growth to one where investors will need to adjust to more upward sloping inflation and higher resting rates.” - Lakshman Anantakrishnan, Chief Investment Officer, ANZ Private.

This is a positive sign for momentum and market sentiment this year.

In 2025, against a more supportive macro backdrop, we see room for risk assets to extend these gains further.

Nonetheless, as the year continues, and as the impact of policy decisions is felt unevenly across the globe, investors will need to remain alert to changing conditions.

The ANZ Private 2025 Global Market Outlook report serves as guide to some of the potential risks and opportunities in this year – illustrating how shorter-term events intertwine with longer-term forces, and how we intend to navigate client portfolios over the period.

You can read our full report here.

A fertile environment

We start 2025 with our most ‘constructive’ outlook for risk assets in several years.

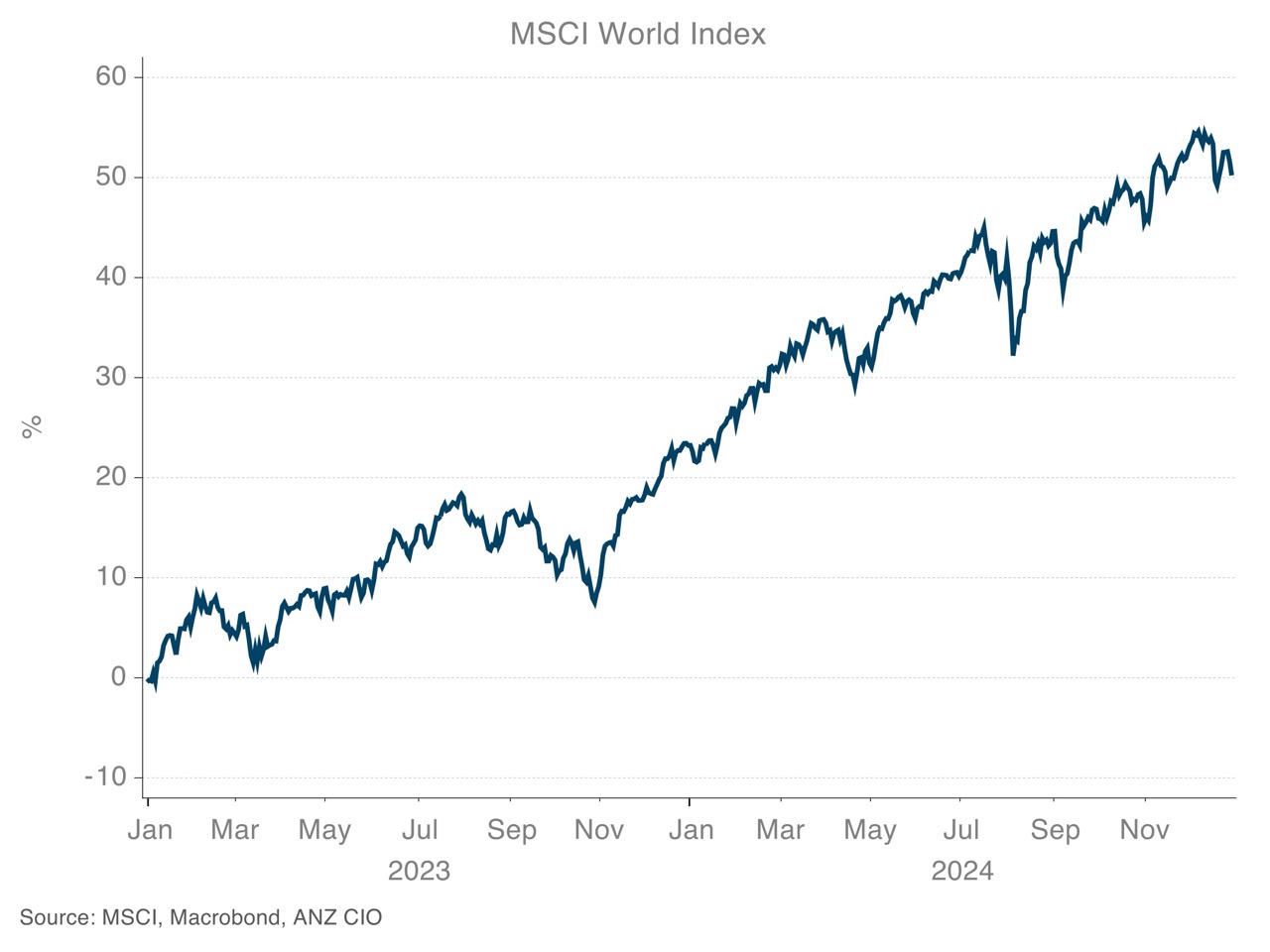

Given the Morgan Stanley Capital International (MSCI) World Index registered back-to-back gains of more than 20 per cent over 2023 and 2024, this may seem a somewhat foolish statement.

That we expect global equities to register low single digit returns in 2025 may make it more so.

But ignoring end outcomes, as 2025 commences, the conditions for markets appear the most fertile that we have seen in recent years. Central banks are lowering rates, fiscal policy remains expansive, a new US President looks likely to drive a pro-growth agenda and the contribution to global growth should be more even, with a modest pick-up to 3.3 per cent expected over 2025.

Markets rose appreciably over the past two years

[image1]

A rising tide

We believe the world is moving from an extended period of disinflationary growth to one where investors will need to adjust to more upward sloping inflation and higher resting rates.

This is the culmination of numerous structural forces including changing demographics, rising inequality, a fractured world order and the green transition.

In this environment, we believe monetary policy is more likely to be used as a means of controlling inflation through the cycle, rather than as a lever for growth.

Not only does this have potential to impact long-standing asset class correlations, but it is likely to see officials look to less conventional measures as a means of extending the cycle and supporting financial markets.

Trump 2.0

Although we remain constructive toward equities, the path higher over 2025 is unlikely to be linear.

Indeed, we expect significant dispersion between asset prices throughout the year. For investors, correctly navigating this volatility should provide opportunity to add significant alpha to portfolios.

One of the primary drivers of this dispersion will be the new Trump presidency.

In our view, the return of Trump is significant, and not just because his policy agenda is likely to testing oth the Federal Reserve and markets alike. Rather, his return is emblematic of a larger issue, changing demographics (one of our four structural thematics) and rising inequality.

More broadly, the parallels between the early part of the 1900s and today should not be ignored — a time when significant market dislocations and financial crises unfolded against a backdrop of wealth inequality, rising populism, unconventional policy, a loss of trust in institutions and the clash of global superpowers.

Trump’s return, and more broadly, the significant failure of incumbents to retain government globally last year should serve as a warning for investors who hope the fiscal spigots may be closed as quickly as they were opened during the pandemic.

Inflationary pressures

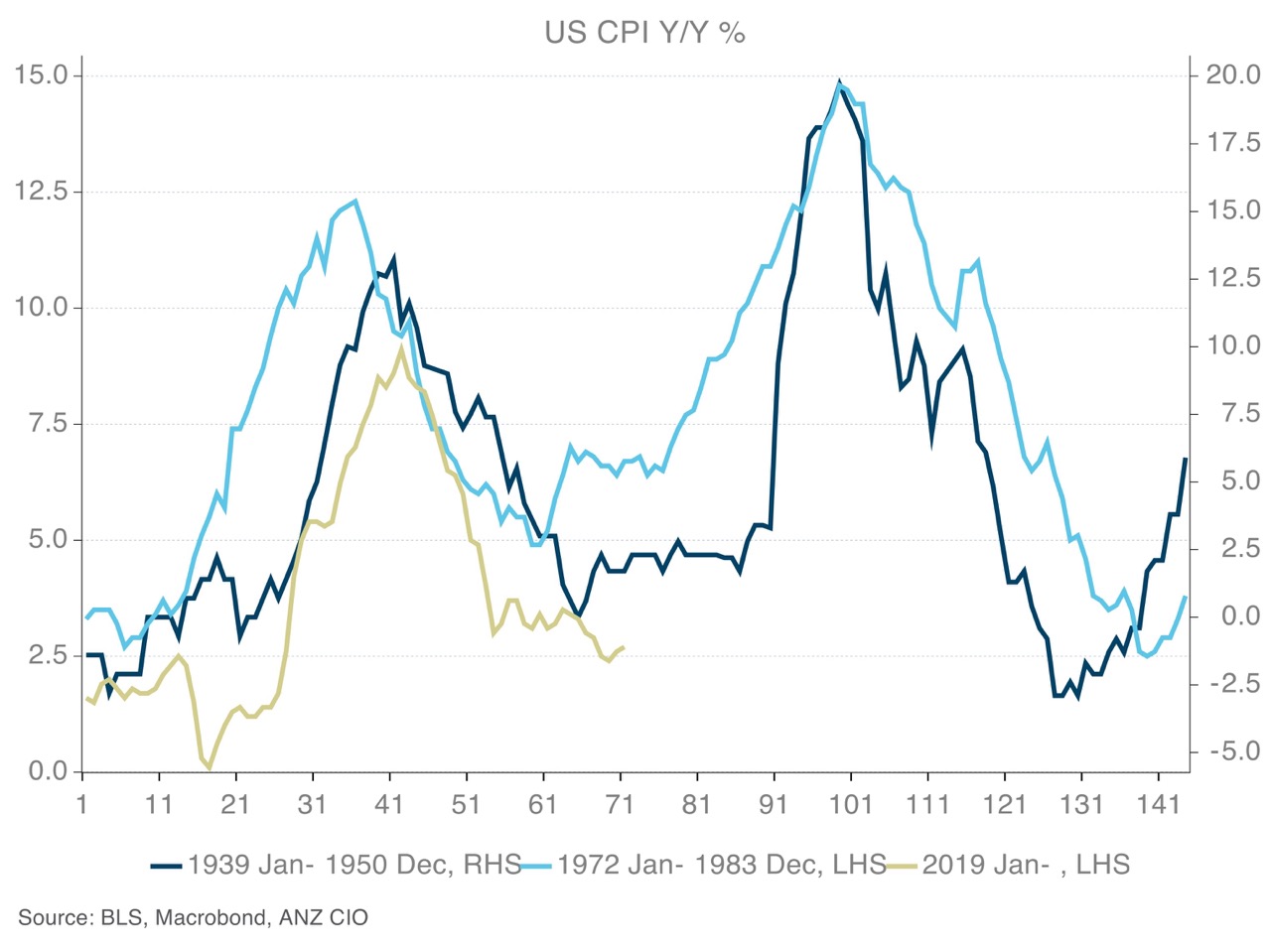

Putting Trump aside for a moment, the world is still grappling with inflationary pressures. Indeed, whether central banks have successfully tamed inflation is a question for late 2025 or more likely 2026.

As we have covered extensively in the past, second waves of inflation are not uncommon.

Central banks cannot declare victory yet

[image2]

Moreover, the approach this time has been different.

In prior periods, inflation has been quashed at the expense of employment.

This time, a number of central banks, including the Federal Reserve, have employment mandates within their charters, alongside a need to manage the business cycle. As a result, the ‘pain’ inflicted on society has been different also.

Trump policy agenda

At a high level, Trump’s policy agenda seeks to appease the voting populace by dealing with taxation (we will give you more money), tariffs (we will make foreign products less competitive), and immigration (we will protect you).

But despite his recent shift in rhetoric toward a more fiscally responsible government, this policy agenda is likely to come at a great cost. Modelling by the Committee for Responsible Federal Budget suggests Trump’s plan could increase US debt by US$7.8 trillion over a decade.

Trump’s policy approach looks likely to continue the protectionist agenda from his first term and is likely to lead to reshoring, the duplication of supply chains and continued fiscal expansion — both by the US and foreign countries in response to US policy. All else being equal, we expect this to support our thesis of upward sloping inflation and higher resting rates over the longer-term.

Of course, for all the consternation surrounding Trump 2.0 it is worthwhile remembering that he pursues a strong economy and share market. Announcements on taxation, spending and a reduction in regulation should favour these goals in the near-term. While an aggressive approach to tariffs and immigration from the start of his term would run counter to these objectives.

Rather, we expect Trump to adopt a more nuanced approach to America-first, using threats as a bargaining chip to help meet other policy objectives such as immigration, while seeking to implement tariffs on countries with large trade surpluses with the US. We expect decisions surrounding China to be more structural in nature as the approach has bipartisan support, and is part of the fight for global hegemony, but a watered-down approach to trade policy seems more likely and less problematic for global as well as US growth.

As a result, over the second half of 2025, and more likely into 2026, we see scope for yields to lift again as central banks grapple with reinflation risks from Trump policy and global growth faces potential headwinds.

While this could present problems for equities, in the near-term, should the global easing cycle remain intact, we see room for rates to fall as markets separate rumour from fact and surplus liquidity from the US Treasury helps ease pressure.

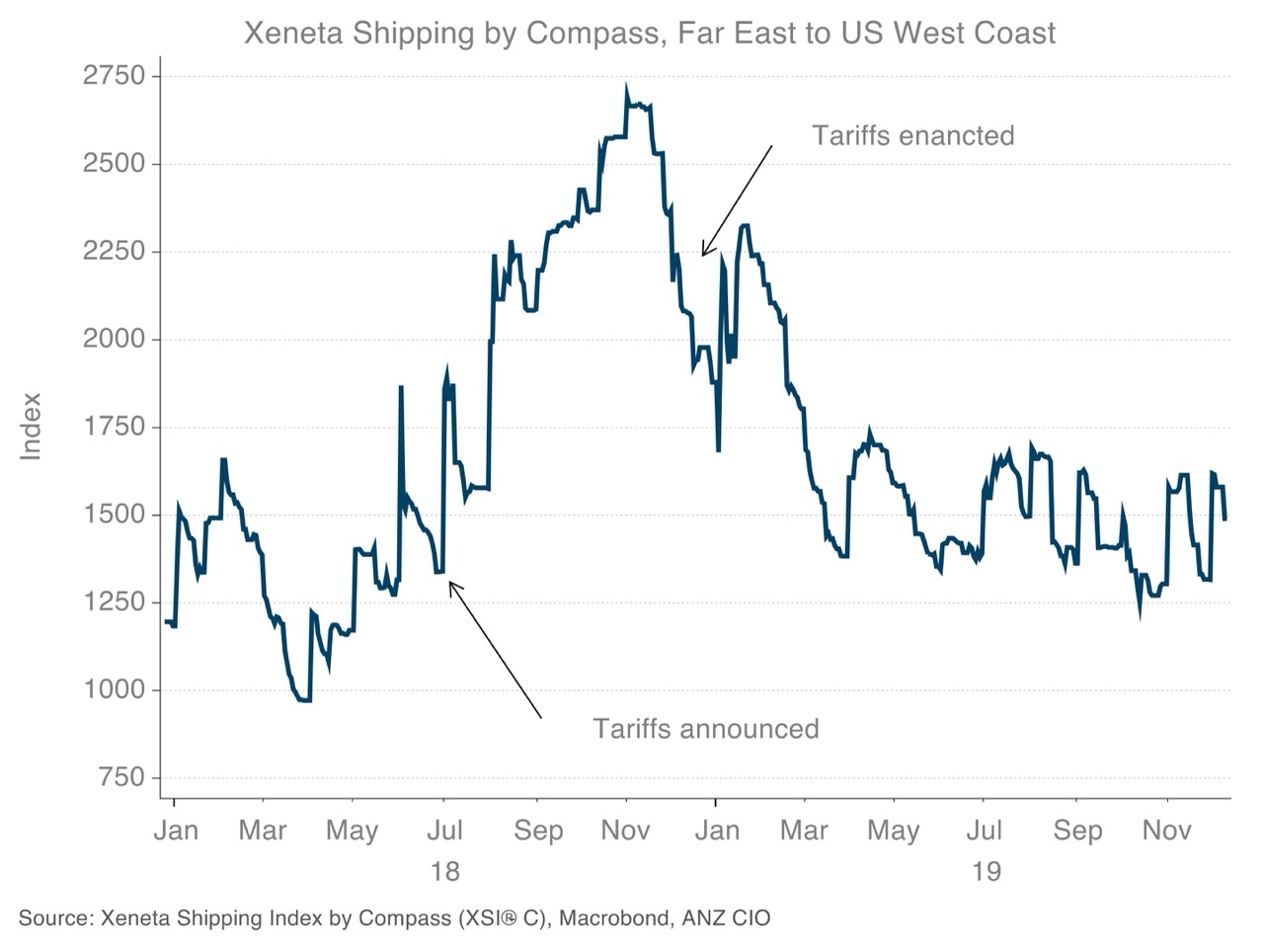

Moreover, in the immediate term there may be a boost to corporate earnings, if, as seen during 2018, corporates seek to stay one step ahead of tariffs and bring forward trade.

Tariffs could be a positive for earnings – at least initially

[image3]

This belief helps inform our positioning within portfolios where we start the year with a bias toward US equities (that we believe are better positioned to withstand Trump headwinds) and mild overweight to gold.

Conversely, we hold a mild dislike for broader emerging markets and China that look particularly susceptible to weakness over the first half. Nonetheless, we expect strong earnings growth across emerging markets over 2025, and coupled with already cheap valuations, maintain a strong focus on fundamentals and look to identify periods of dislocation as a possible means to increasing our position over the latter part of the year.

The fundamentals

While we expect US Treasury spending and its impact on liquidity to play an important role for markets this year, it would be ill-considered to completely ignore fundamentals at this point in the cycle.

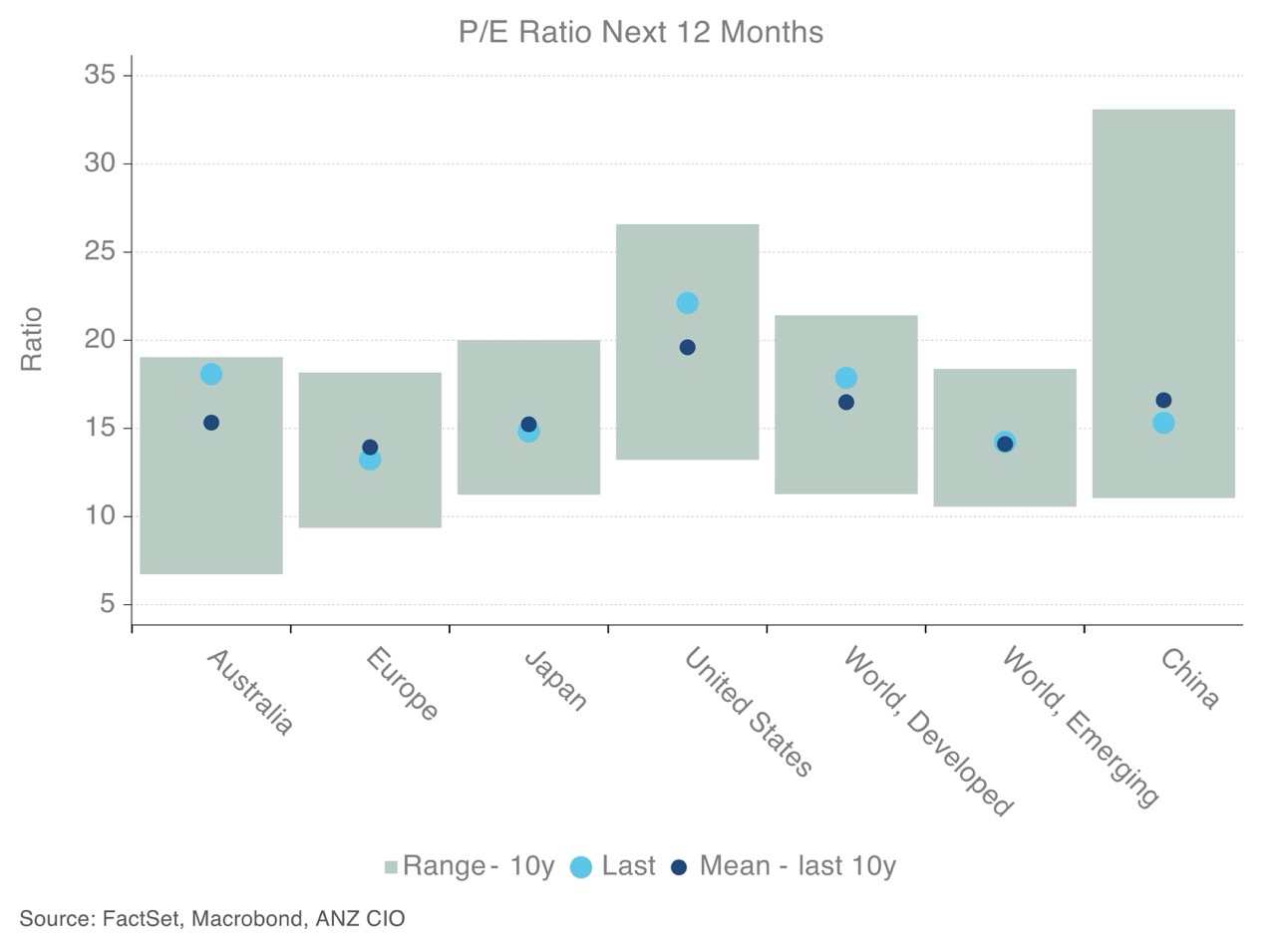

In 2025, concentration risks — including Australia and the US — alongside rich equity valuations are expected to again be a major factor for investors to navigate. While we remain cognisant of these risks, we don’t believe they are insurmountable.

Rather, they speak to a continued need for portfolio diversification — including alternative assets — and tactical positioning over the year ahead, ensuring adjustments are made should market pricing move too far ahead of fundamentals.

Indeed, we start the year with our largest overweight in US shares, where we hold a modest preference for tech-related mega caps.

While the US market is among the most expensive - we expect the AI theme has further to run and that US tech companies will continue to produce strong earnings growth.

In Australian shares we commence the year with a mild underweight. The ASX, like the S&P 500 is another heavily concentrated and currently overvalued market when compared to history.

However, unlike the US where we expect strong earnings growth from the largest constituents, here the earnings outlook appears more constrained, leaving room for disappointment. While we see modest earnings growth potential for the banks over 2025, we expect soft iron ore prices and continued risks to the outlook for China as a possible drag on the Materials sector.

Regional valuations remain mixed

[image4]

As the year commences, we expect favourable liquidity conditions to persist, but with the added benefit of a more supportive monetary environment. While this could lead to rising inflationary pressures and a resurgence in upward pressure on central bank rates, the near-term outlook presents a more constructive environment for risk assets.

As always though, and perhaps more so than usual under Trump 2.0, investors should expect the unexpected and be prepared to adjust portfolios as necessary.

In 2025, a diversified portfolio and long-term investment strategy should again be the best way to navigate unforeseen risks and participate in opportunities as they arise.

Click here to read ANZ Private's latest investment update in full.

Lakshman Anantakrishnan is Head of Investment Strategy in Private Banking & Advice at ANZ

-

-

-

-

Share

anzcomau:Bluenotes/global-economy

A fertile time for markets?

2025-01-29

/content/dam/anzcomau/bluenotes/images/articles/2025/lakshman-anatakrishnan-thumbnail-2.jpeg

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

EDITOR'S PICKS

-

The chief financial officer role is changing; two of the nation’s top CFOs explain its evolution.

6 December 2024 -

Some traditional drivers of asset prices are being overwhelmed by alternative policy measures and structural change including disruptive tech and the green transition. This presents opportunity.

10 July 2024