-

The saying, better late than never, is typically a positive one. However, in the case of the likely impending recession, it might not be so for markets.

Rather, the further this late cycle phase extends and the higher central banks need to raise interest rates, the deeper any market fallout might become.

"We would caution against becoming too aggressive and chasing a market that has rallied more than 20 per cent since its October low, and almost 100 per cent from its COVID-nadir.”

{CF_VIDEO}

It is just three months from our last quarter-end update, and yield curves are again looking ugly. In Germany, the 2 year/10 year yield curve is deeply negative. In Australia, the yield curve for bonds of a similar tenor turned negative last month — for the first time since the global financial crisis.

And in the US, after beginning to steepen following the banking crisis, the 2 year/10 year yield curve is again hovering at a 100-basis point inversion. Moreover, it’s entering its thirteenth straight month of inversion — the third longest on record.

So, if this ends up as the most well telegraphed global recession in recent memory, why then have equity markets continued to climb steadily over the past quarter? And could this mean the much-vaunted downturn will fail to materialise?

The simple answer is - unlikely.

In our view, it appears a few key factors have simply delayed, rather than stopped any eventual downturn —one we still expect before year-end. Rather, our recent message to investors remains — don’t confuse late with not coming.

With respect to equity market returns, while solid in recent months, they’ve come with rather idiosyncratic features. Over the first half of the year the S&P 500 rallied more than 16 per cent. However, remove the performance of the top seven contributing stocks and this performance looks drastically different — somewhere closer to 5 per cent. And although the recent earnings season came and went — without deeply negative revisions — it was the second successive quarter of negative earnings growth, with a third expected to follow.

To financial conditions more broadly and the banking crises. Many initially feared this would bring widespread capitulation across markets, however it seemingly had the opposite effect. Outside of a few downtrodden sectors, it may have supported equity markets in recent months as the US Federal Reserve provided a backstop and the financial system was suddenly awash with liquidity.

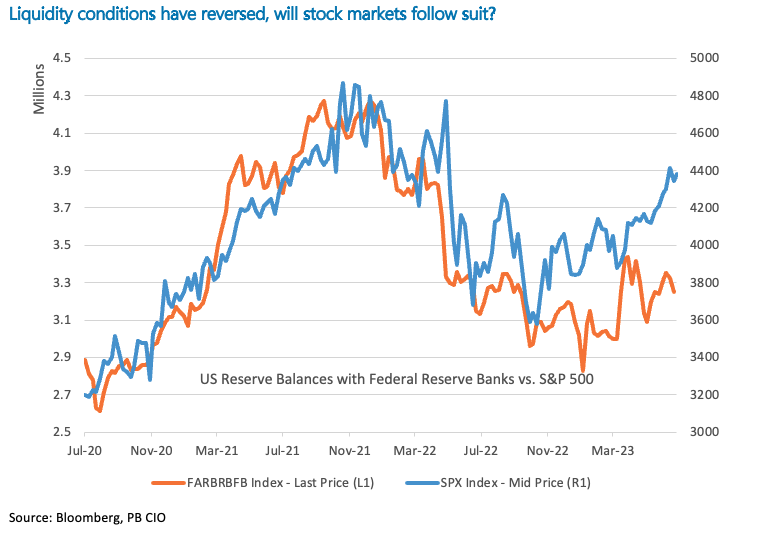

Abundant liquidity

Alongside the debt ceiling impasse and the US Treasury’s inability to issue new debt, it’s reasonable to suggest liquidity has been abundant and a prevailing force for equities over the first half of the year.

Indeed, this may help explain why — even with the Fed’s ongoing balance sheet reduction — equity markets have remained buoyant. And while there’s been some divergence of late, there is a clear correlation between equity market performance and market liquidity.

However, with the US Treasury now refilling its general account — and the Federal Reserve set to continue its balance sheet run-off over coming months — we expect liquidity to evaporate and this divergence to converge once more as liquidity becomes a drag on asset prices.

This comes against a macro-backdrop and outlook that is looking no less clouded and increasingly difficult for central banks to navigate.

It’s here, that we are now seeing what most — including ourselves — expected to arrive much earlier this year. Growth has continued to deteriorate with a steep decline in Purchase Managers’ Index last month. The eurozone has officially entered recession and Gross Domestic Product forecasts for China have been revised sharply lower.

Perhaps most concerning are the persistent price pressures, particularly across core and services inflation. Combined with still strong labour markets, central banks are being forced to talk (and in some cases act) hawkish once more. In fact, after initially pricing out further rate hikes following the banking crisis, market pricing is now suggesting more increases before year-end and little prospect of rate cuts in the US until next year.

Tighter financial conditions, negative earnings growth, and restrictive monetary policy settings — against a prolonged late cycle backdrop — are unlikely to bode well for risk assets. This is why we have continued to transition portfolios to a more defensive posture over the second quarter of the year — something we highlighted as probable in our base case at the start of 2023.

While the slower pace of the economic downturn has taken us by surprise, the overall direction has not. We expect this downward trend to continue over the back half of the year. Rather, the performance of some equity markets has left us pleasantly surprised.

Sound investment

However, we would caution against becoming too aggressive and chasing a market that has rallied more than 20 per cent since its October low and almost 100 per cent from its COVID-nadir, particularly when financial conditions remain so vulnerable.

While the outlook for equities appears more troublesome, sound investment opportunities remain, and bonds in particular are providing important diversification benefits to portfolios and compelling yields once more.

Of course, markets rarely behave as expected. As seen repeatedly over the COVID-period, significant downturns are typically followed by sharp upswings. Attempts to time investing to maximise returns during these periods is typically a fool’s errand, often leaving investors disappointed.

Being invested in a well-diversified portfolio that is ready to take advantage of opportunities on the other side of any downturn is often the best course of action. Remaining invested through the full market cycle is the most critical factor for compounding returns and long-term wealth creation.

{CF_IMAGE}

What this means for our diversified portfolios

During periods like these, we position portfolios to broadly participate in upside surprises, while maintaining the right defensive characteristics and liquidity profile to protect capital should risks become increasingly skewed to the downside.

And while overall portfolio allocations to growth and defensive assets aren’t markedly different to three months ago, the mix of asset classes should provide for better diversification and increased defensive characteristics across portfolios as we enter the second half of the year.

Changes this month have included a reduction in Global Real Estate Investment Trusts and emerging market equities. In the case of emerging market equities, we remain mildly overweight the segment and on a relative basis, it remains our preferred equity exposure across portfolios.

Indeed, we remain constructive towards it on a strategic basis also. However, given the late-cycle risks we have made the decision to reduce exposure to volatility in portfolios and adopt a more neutral stance across the equity bucket.

In fixed income, we’ve recently trimmed exposure to high-yield credit, again preferring to adopt a quality bias into late cycle. We’ve also changed our holding of global fixed income, taking the position to just below benchmark with purchases of both global sovereign and investment grade bonds. Alongside our continued mild overweight to Aussie fixed income and cash, this sees us positioned with an overweight to defensive assets overall.

Click here to read ANZ Private's latest investment update in full.

Lakshman Anantakrishnan is Head of Investment Strategy in Private Banking & Advice at ANZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

Share

anzcomau:Bluenotes/Economics,anzcomau:Bluenotes/global-economy

Don’t confuse late with not coming

2023-07-10

/content/dam/anzcomau/bluenotes/images/articles/2023/July/levi-meir-clancy-jdIT3puximI-unsplash.jpg

EDITOR'S PICKS

-

Banking crises and financial stability are dominating headlines, following the sharpest rate tightening cycle in decades. Despite the calamity, inflation remains the key issue for policy makers.

14 April 2023 -

There’s likely to be no shortage of challenges for the global economy and markets in 2023. But those challenges should bring opportunities for patient investors who know where to look.

20 January 2023