-

Much ink has been spilled and airtime filled with discussion of the wild ride the Australian property market has had in the last few years, notably the impact of COVID-19, record low interest rates and generous government support.

Through the pandemic one particular market – Queensland – saw one of the strongest price upswings across the states and territories and also some of the highest increases in rents.

Queensland has several factors in its favour – a highly diverse economy, strong internal migration trends and international tourism attractions, including the 2032 Brisbane Olympic Games. These factors are also likely to see ongoing investment and competition for housing across the state.

The latest ANZ-CoreLogic Housing Affordability report highlights the increased demand pressures on Queensland housing markets and the challenge that creates for housing affordability.

Analysis of income, rent and housing value data show the cost of servicing a new mortgage or new rental lease continued to increase as a portion of income through the three months to September 30, despite some aspects of housing affordability improving.

Higher demand has been a key driver of prices and rents. A surge in interstate migration to Queensland meant the state had the highest annual rate of population growth of the states and territories over the year to March 2022, at 1.8 per cent. In the year to March about 54,000 more Australians moved to Queensland than left.

WHAT ARE THE MOST POPULAR INTERNAL MIGRATION DESTINATIONS OF QUEENSLAND?

Portion of Queensland net internal migration (2017-2020){CF_IMAGE}

Lifestyle markets like the Gold Coast attract the most internal migration from other parts of Australia, accounting for 28.1 per cent of net internal migration in the four years to June 2020.

High migration areas saw the biggest upswing in dwelling values since the onset of COVID-19 through to October 2022. The Gold Coast had the strongest dwelling value gains since March 2020 at 43.7 per cent.

HOW DOES THE DWELLING VALUE TO INCOME RATIO COMPARE ACROSS OUR LARGEST CAPITAL CITIES?

{CF_IMAGE}

Meanwhile, the lift in Queensland housing values suggests a greater deterioration of housing affordability in a relatively short period of time than in other parts of the country.

The relative affordability of housing in Brisbane and the rest of Queensland though compared with New South Wales worked as a ‘pull factor’ that drove higher migration to the state through to early 2022, lifting property prices.

Through that period, 48 per cent of interstate migration to Queensland was from NSW while a further 28 per cent came from Victoria. As prices rose across Australia through the pandemic, increased housing values in the southern states may have prompted more migration to Queensland.

Interstate migration also rose with economic activity and heightened job opportunities amid the low interest rate environment to May 2022. The emergency interest rate setting during the pandemic contributed to the lowest levels of unemployment in decades. Annual jobs growth in Queensland was 4 per cent in September 2022, above a 20-year average of 2.4 per cent.

Furthermore, the pandemic prompted a significant shift in remote work trends.

INDEXED CHANGE IN MEDIAN RENT VALUE

(GREATER BRISBANE)

INDEXED CHANGE IN MEDIAN RENT VALUE

(REST OF QUEENSLAND)

The productivity commission estimates around 38 per cent of full-time workers have the capability to do aspects of their job remotely. This allowed more Australians – particularly knowledge workers on higher incomes – to move to lifestyle markets. In some of these markets affordability has become extremely stretched for long-term residents.

The Gold Coast saw the portion of income required to service a new rental lease rise to 42.7 per cent as of September, from 33.3 per cent at the onset of the COVID-19 pandemic.

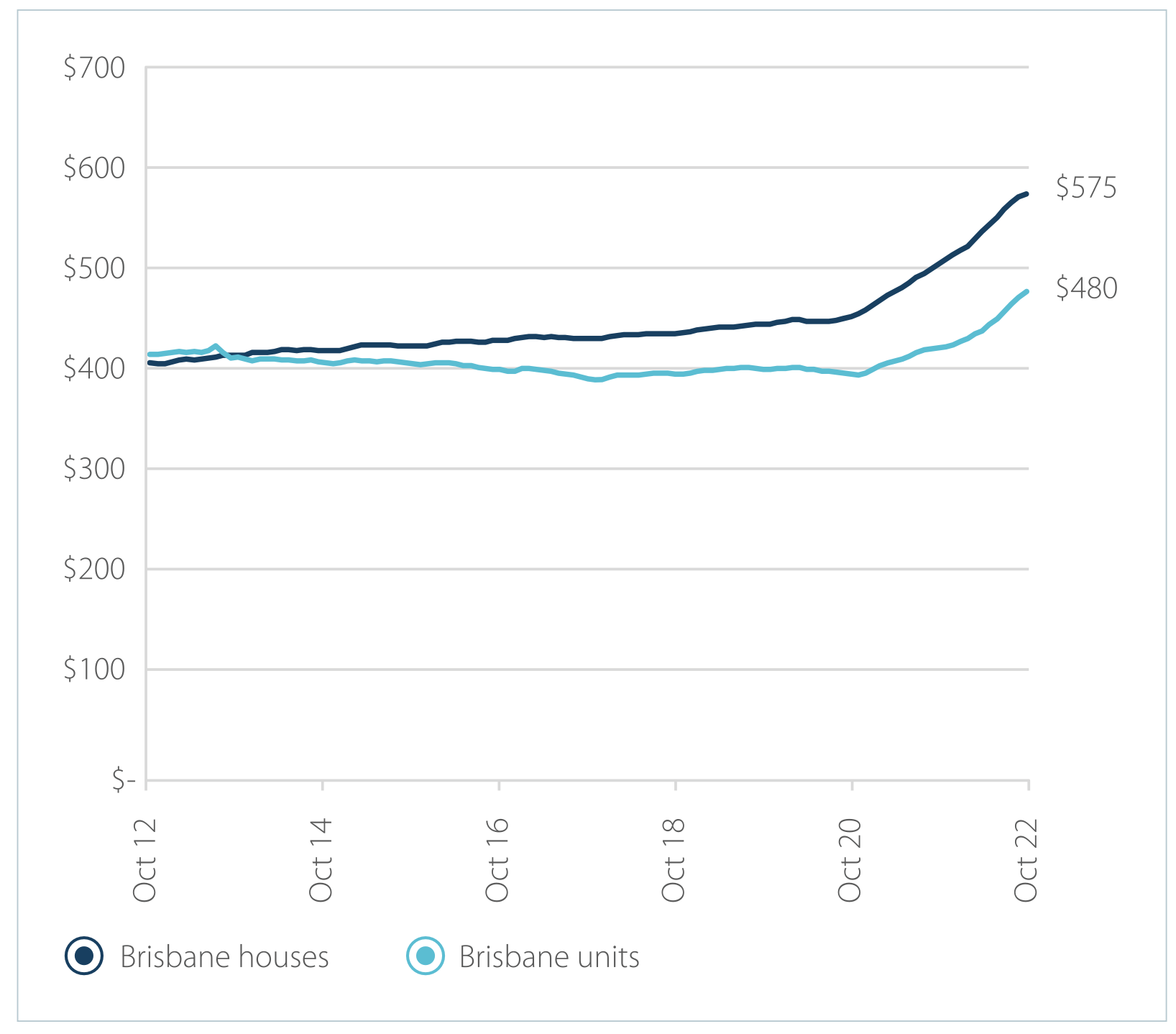

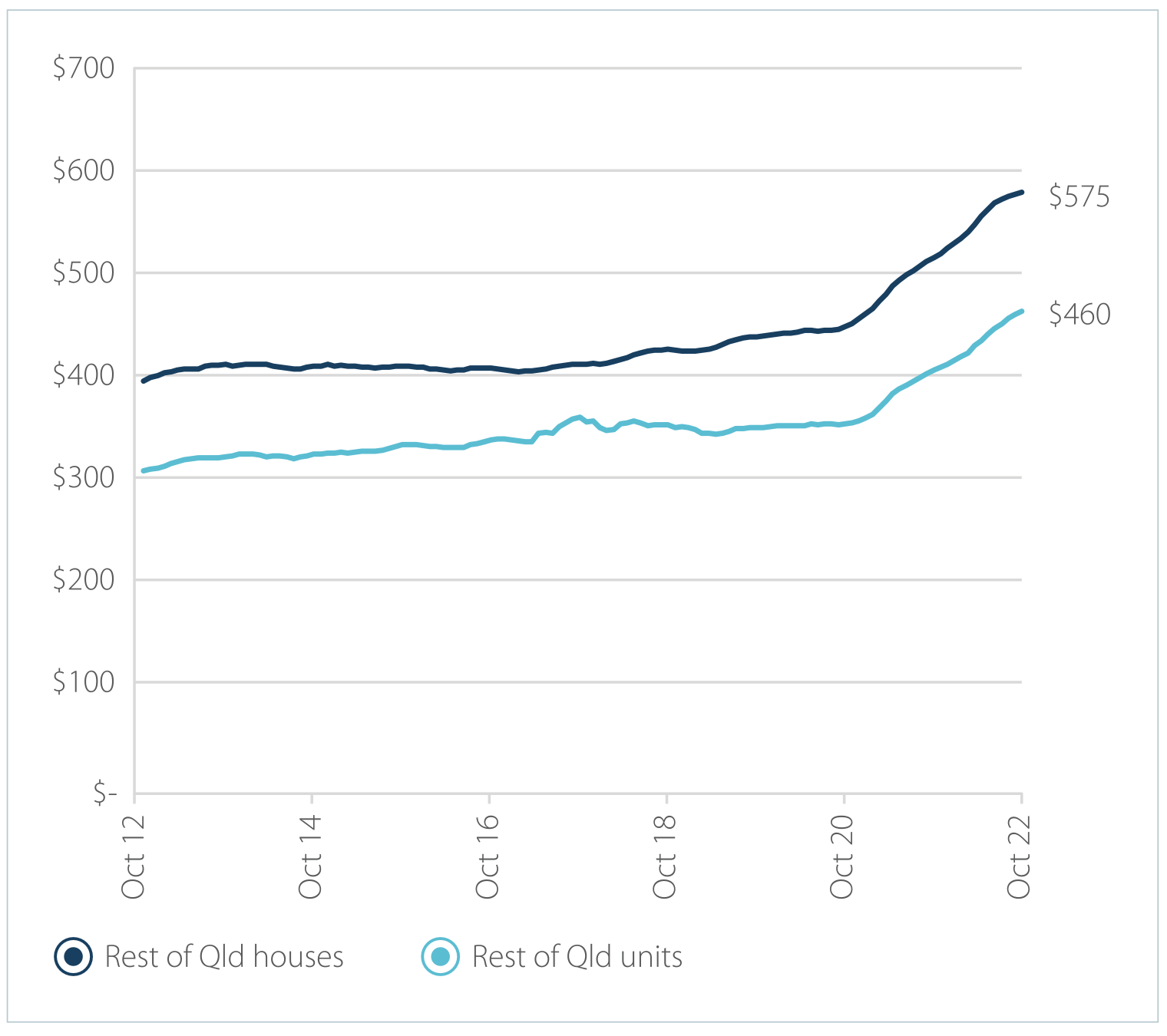

The portion of income required to service a mortgage has also continued to rise. For the median household income household in Brisbane, CoreLogic estimates it would take 40.3 per cent of income to service a new mortgage on the median dwelling value. This is up from 29.1 per cent a year ago and 25.8 per cent in September 2020.

Across the rest of state region, the portion of income required to service a new mortgage on the median dwelling value at September was 36.9 per cent. Mortgage serviceability is most strained in markets like the Sunshine Coast where it would take almost 60 per cent of median income to service a mortgage on the median dwelling value.

More recently, rapidly rising interest rates have started to impact dwelling values. Brisbane values have declined 5.5 per cent since a peak in June 2022 through to the end of October. This fall in prices has reduced the so-called deposit hurdle – or the time it takes to save a 20 per cent deposit on a median value dwelling.

Across Brisbane the time taken to save a deposit was estimated to be 10.1 years in September 2022, down from 10.8 years in June 2022. However, it is still a long time to accumulate a deposit especially compared with the 7.5 years needed in September 2012. Moreover, prospective first home buyers will find saving for a deposit more challenging in an environment of rising living costs and sharply rising rents.

The highest amount of time required to save a 20 per cent deposit is in the Sunshine Coast with an estimated 14.7 years required for the median income household at September 2022.

CORELOGIC ADJUSTED MEDIAN VALUE

(Queensland dwellings){CF_IMAGE}

Some other market conditions have become more favourable for home buyers in Queensland this year. Since the start of the year properties have taken longer to sell, with median days on market across Brisbane lifting to 31 days in the three months to October from 13 days in the three months to January.

Across the rest of Queensland, median selling times have increased to 38 days from 19 over the same period. Vendors have also been discounting from initial listing price to the contract price.

The median vendor discount has deepened across Brisbane to 4.4 per cent in the three months to October from 2.9 per cent in the three months to January. In the rest of the state, vendor discounting reached 4.5 per cent in the past three months, up from 3.4 per cent at the start of the year.

These factors mean first home buyers may have more bargaining power in negotiations, and have more time to carry out due diligence, and compare properties. However, first homebuyer demand has been dropping in Queensland since February 2021, coinciding with the end of the HomeBuilder scheme.

On the supply side, the construction pipeline is down relative to historic averages while high interest rates and sharply higher construction costs will be headwinds to a recovery.

This suggests the demand-supply imbalance in Queensland will take some time to address. Given the outlook, the state is likely to continue to attract new residents but ongoing strong housing demand will remain a challenge to housing affordability.

Felicity Emmett is a Senior Economist at ANZ and Eliza Owen is Head of Residential Research Australia at CoreLogic.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

Share

anzcomau:Bluenotes/Housing,anzcomau:Bluenotes/Research

Queensland’s Catch 22: strong demand exacerbates the housing affordability challenge

2022-11-23

/content/dam/anzcomau/news/articles/2022/November/CoreLogic_Queensland_appartments.png

EDITOR'S PICKS

-

A guide to the trends and main drivers of housing affordability across Queensland.

2022-11-23 08:05 -

The latest ANZ CoreLogic Housing Affordability Report shows record low rental affordability in regional Australia where rents can be greater than the cost of servicing a mortgage.

2022-05-12 10:00