-

When interest rates go up it’s usually because of inflation. This time is no different. But what rising rates also do is make risk more expensive. And so risky things lose value.

And that, even though the boosters argue otherwise, is the proximate cause of the carnage in DeFi – decentralised finance – markets and crypto classes in recent days and weeks. Risk is now ultimately more expensive relative to safer assets.

"This latest spate of major market malfunctions, coin collapses, DeFi destruction and NFT DNFs demonstrates graphically the correlation across markets.”

It might seem counter-intuitive, given rising rates have the most immediate impact on bond markets which are supposed to be low risk and crypto assets are suddenly cheaper.

But that’s because a bond is valued on its total value – its principal price plus the accrued interest it will pay over its tenor, whether that be three months or 10 years. So if the amount paid in interest is rising, it’s price is falling. Yield up, price down.

However, bonds, particularly those backed by governments and highly rated corporates, are considered lower risk because they are predictable, an earnings stream is locked in and the principal – unless there’s a default – is paid back at the end of its tenor.

When interest rates are low, bonds have high prices but low interest payments so investors looking for interest payments – yield – are more likely to look further out the risk curve, to property, equities or other assets in the search for returns. Even to crypto assets.

Destruction

When you’re comparing almost no income stream with some income stream, markets tend to take more risk to get the return. But now the returns from interest rates are rising, the cost of the risk in other markets is priced higher. Why risk losing a lot for a little extra income when you can be safer on not much less?

A crypto currency may now be massively cheaper to buy but that’s because the long term return on it is vastly more uncertain.

But, scream crypto investors, the whole point of crypto is it’s not supposed to be correlated with the real world. It is supposed to be orbiting far out in the galaxy away from the gravitational pull of central banks, regulation, interest rates, TradFi – traditional finance – or boring old market pricing.

It seems that’s wrong. In a massive shock.

This latest spate of major market malfunctions, coin collapses, DeFi destruction and NFT DNFs demonstrate graphically the correlation across markets even where causation is hard to discern.

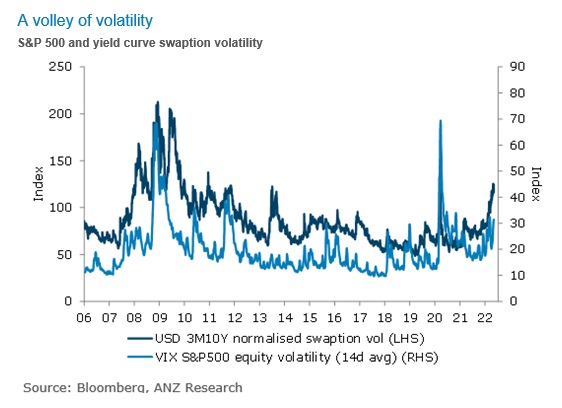

ANZ New Zealand Chief Economist Sharon Zollner published a series of charts showing the shocks taking place.

Volatility is up:

{CF_IMAGE}

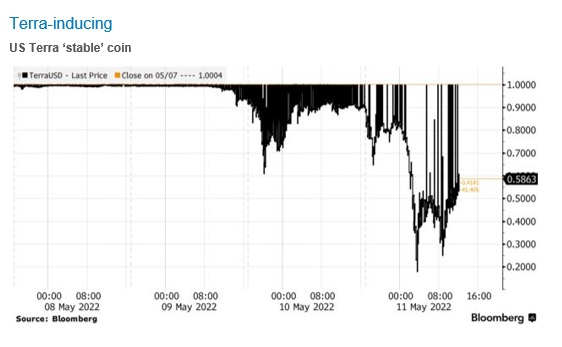

Meanwhile, a range of cryptocurrencies, other crypto assets and the exchanges on which they trade have cratered.

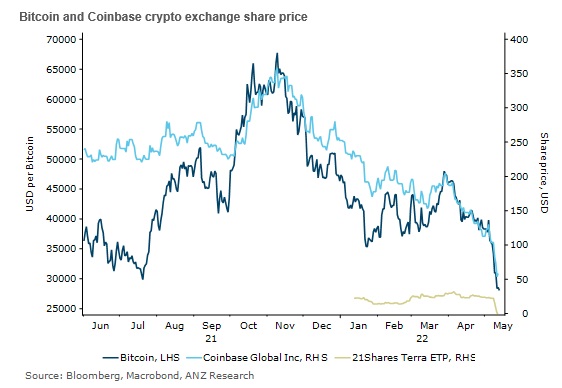

{CF_IMAGE}

Coinbase is the highest profile exchange for crypto and is suffering from plunging activity in the assets. The correlation cuts two ways – not only is the real world impinging on the crypto world, the more conventional tech-heavy Nasdaq index has collapsed by nearly a third this year with the theory being those investors keen on crypto are also in other tech investments which they may be liquidating.

{CF_IMAGE}

Not-so stable?

However, while the purist crypto evangelists have long – even if misguidedly – spruiked their independence from the official finance world, one category of cryptocurrencies, so-called stablecoins, have attempted to straddle both.

Stablecoins are cryptocurrencies but they are “tethered” to use the popular term to real currencies, whether the US dollar or a basket of currencies. Theoretically, that should fix their value to the pegged currency.

Spoiler alert: it didn’t for the latest high-profile collapse, TerraUSD.

But this is why it’s important to be discerning in this new DeFi world. Not all crypto assets are the same and, critically, not all stablecoins are the same. Indeed, in a time of stress like we are experiencing, with risk aversion surging, it’s important to understand there are very important differences.

It comes down to how stablecoins are structured. TerraUSD is not actually backed by cash or cash-like assets. It is backed by an algorithm, the nature of which is the special sauce. It is supposed to constantly manage assets so each TerraUSD can be redeemed at any time for a dollar. Which it did.

Until it didn’t.

Exactly the same lesson in reality – that a tether or “cash-like” are not actually cash when the acid bites – happened to American money market funds during the 2008 global financial crisis. These funds managed their investments for higher yields but on the premise each unit would never be worth less than a dollar.

However, at the peak of the crisis, as financial markets froze, cash-like was suddenly oh so close but not enough. In the search for that extra yield, these funds introduced an element of risk which before the crisis had never been recognised. Then, in the vernacular, they “broke the buck”.

So too with stablecoins. A tether, however clever, is not tangible asset backing.

A$DC

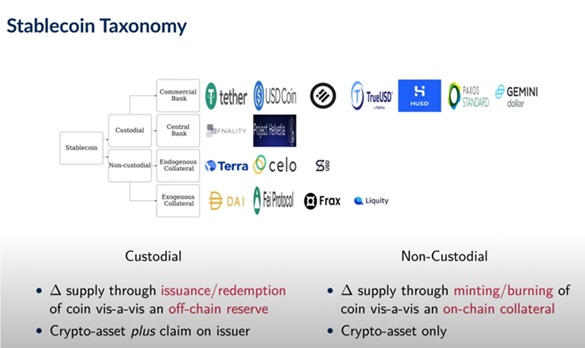

Technically, TerraUSD is an unbacked, “algorithmically stabilised”, USD coin which is used in unregulated DeFi venues. It is known as a Non-Custodial coin.

However, other stablecoins, including the A$DC recently minted by this bank, ANZ, are backed by hard “fiat” currency. And, equally critically, the institution doing the backing, in this case ANZ, is a fully regulated and prudentially licenced financial institution. In Australia this category of organisation is called an “approved deposit taking institution”, an ADI. A$DC is a Custodial Coin.

This structure, and its location within a highly regulated ring fence, makes for a stablecoin which is different in kind, not just degree, although that distinction has only become visible as risk aversion has peaked.

This point was made clear by ANZ Banking Services lead Nigel Dobson at the bank’s half year result.

“Because this stablecoin is backed by ANZ – with our AA credit rating and government deposit insurance – it does not face the same risks of a ‘run’ on redemptions which have caused some concerns with more volatile versions of stablecoins,” he explained.

“We have also been clear in discussions with the Australian Prudential Regulatory Authority (APRA), the Australian Securities and Investments Commission (ASIC) and the Australian Transaction Reports and Analysis Centre (AUSTRAC) that we are only exploring custodial stablecoins that are 100 per cent backed by cash and we have no intention of pursuing algorithmic stabilisation mechanisms.”

{CF_IMAGE}

Radically different

Not just in cryptocurrencies but across crypto assets there is a clear distinction between innovations designed to use distributed ledger platforms such as blockchain to augment the existing financial system and those which are attempting something radically different.

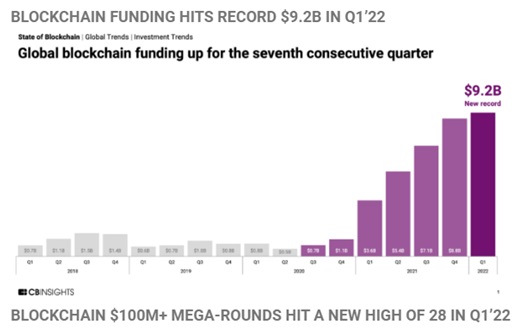

Although there is always a lag before longer term investors react to market situations, blockchain investment continues to grow at record levels because it is supporting innovations with inherent value and utility as well as those shooting for the stars.

According to CB Insights’ latest report on the sector, blockchain and crypto startups had a record-breaking funding quarter as venture capital firms doubled down on “Web3” – a blockchain enabled world.

{CF_IMAGE}

Separating assets with robust value and utility from speculative ventures and outright Ponzi schemes will be one of the challenges of this new era.

The former have an inherent value – such as a cash backing – and utility – such as providing certainty in contracts and supply chains with much greater efficiency – which gives them a role in the financial system.

Those whose only underlying value is an idea and an attraction to speculators may indeed prove to revolutionise the financial system in the future. But as we are seeing in this current shakeout, the majority will crash and burn. Particularly as interest rates rise and investors place more value on security.

That’s creative destruction at work.

Andrew Cornell is Managing Editor of bluenotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

-

-

Share

anzcomau:Bluenotes/Banking,anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/Innovation

Ah, you want a stable stablecoin…

2022-05-18

/content/dam/anzcomau/bluenotes/images/articles/2022/May/May18_AC_Thumb.jpg

EDITOR'S PICKS

-

Fintech was once touted as the great challenger to traditional finance, will DeFi – decentralised finance – be the next threat? Or will it create opportunity?

4 May 2022 -

The global financial system is facing the next phase of the digital revolution – decentralised finance.

29 September 2021