-

December 4 was International Day of Banks – seriously – so it’s a good time to review the health of the industry.

Historically, economic crises tend to be caused by the banking system blowing itself up. In 2008 it was poor pricing for risk and a failure to understand where that risk was held that led to the American sub-prime mortgage collapse which crashed financial markets globally.

“The financial sector survived the pandemic in pretty good shape, in part because of the rules put in place after the global financial crisis.” - Steven Leslie, Principal Finance Analyst at the Economist Intelligence UnitBad debts and failed banks followed.

In the Asian crisis of the late 90s countries became over-indebted in US dollars and again the banking system had failed to price in or appreciate the risk of widespread defaults and capital flight. More bad debts, more dead banks.

Australia’s last major recession in the early 90s came down to banks over-lending to commercial property and the business sector – both of which were kneecapped when the official cash rate neared 20 per cent. Bad debts swamped the sector for years after.

Coming out of the pandemic however – and of course this recovery will be volatile – the banking system is actually in decent shape.

That’s because banks didn’t cause this crisis. And they were well capitalised – thanks to the response to the global financial crisis. They were able to support corporate and consumer customers which ultimately meant less bad debt[JW1] . There was plenty of liquidity around to fund banks – and banks tend to fail due to a lack of liquidity rather than insolvency because they borrow for short periods and lend for long.

Pretty good shape

In this crisis though, because there hasn’t been a lot to spend money on and governments globally have provided financial relief, there haven’t been runs on banks. In Australia, for example, households amassed additional savings worth more than $A220 billion, around 10 per cent of gross domestic product (GDP), during the COVID-19 crisis.

As Steven Leslie, Principal Finance Analyst at the Economist Intelligence Unit, says “the financial sector survived the pandemic in pretty good shape, in part because of the rules put in place after the global financial crisis. Bad loan ratios actually fell in 2020”.

That’s certainly a better outlook than 18 months ago. And the rising interest rates we are starting to see globally are usually, up to a point, good for banks because they allow margins to increase.

Yet an ostensibly better outlook for financial services elides some underlying, existential threats to the sector – or at least those banks unprepared for the disruption. Not all banks are in the same place.

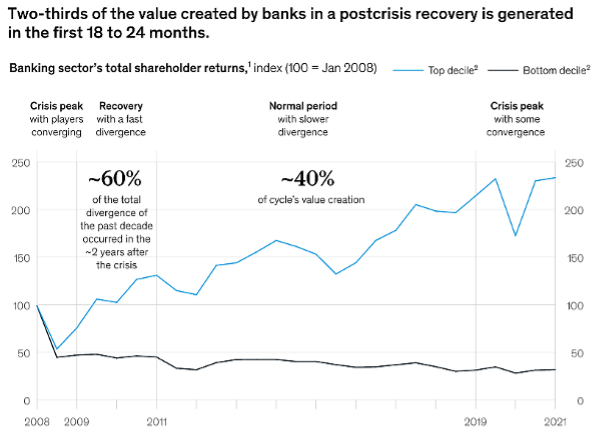

McKinsey & Co’s latest Global Banking Survey notes “the valuation gap between leading banking institutions and those trailing behind is once again widening. Decisions made in the next 18 to 24 months will determine which firms emerge on the right side of this divergence”.

{CF_IMAGE}

Whimper, not a bang

The central issue for global banking this time around is not that a bunch of banks are going to immolate but that they won’t make enough money to attract investors. That would be going out with a whimper not a bang.

“Cause for concern is evident in banks’ performance on two yardsticks: return on equity (ROE), a measure of current profitability, and market-to-book value, a leading indicator of how capital markets value banking,” McKinsey argues.

“Fifty-one per cent of banks operate with an ROE below cost of equity (COE), and 17 per cent are below COE by more than 4 percentage points. In an industry that has high capital requirements and is operating amid low interest rates, creating value for shareholders is structurally challenging.”

Since the financial crisis banks have not been great stewards of shareholder funds in McKinsey’s view: “In fact, the almost $US2.8 trillion of capital that was injected by shareholders and governments into banking over the past 13 years eroded 3 to 4 percentage points of ROE.”

That translates into valuations: “Banks are trading at about 1.0 times book value, versus 3.0 times for all other industries and 1.3 times for financial institutions excluding banks, with 47 per cent of banks trading for less than the equity on their books.”

Yet this is not true for all banks – during the pandemic the financial system as a whole gained about $US1.9 trillion (more than 20 per cent) in market capitalisation, McKinsey says.

The next phase

So the issue comes back to the growing disparity between high and low performers. What are the forces then that will push this disparity?

Competition is intense not just between incumbent financial institutions but from emerging competitors, be they fintech, bigtechs, neo-banks and non-bank financial institutions. This next phase will swing on which organisations can most quickly move to the kind of digitalisation customers want and harness the power of the data they have access to – without damaging the necessary trust their customers demand.

Yet at least these are comprehensible and largely measurable threats.

Climate change, as an existential threat to the planet, is also a clear and present danger to the financial system, on two fronts.

The Reserve Bank of Australia’s (RBA) deputy governor Guy Debelle summed it up in a speech titled “Climate Risks and the Australian Financial System”.

“Climate change is a first-order risk for the financial system. It has a broad-ranging impact on Australia, both in terms of geography and in terms of Australian businesses and households. Most Australian financial institutions now recognise climate as a risk. The assessment of climate risks has evolved considerably over the past five years, but there remains considerable scope for further improvement.”

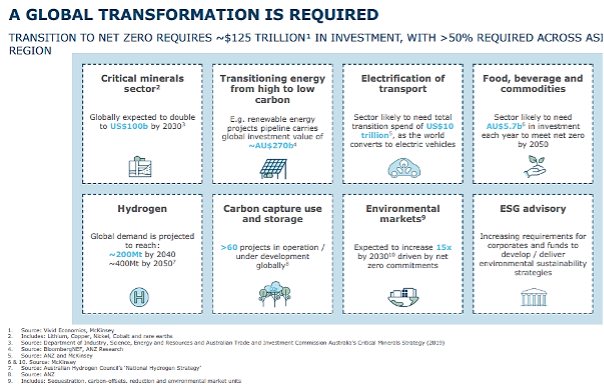

That’s one front. But the other is the opportunity cost: there is value in investing in those industries and technologies that will address climate change and the financial assets that will support investment in the transition to lower carbon intensity.

According to the International Energy Agency’s World Energy Outlook 2021, investment related to the transition to zero emissions will need to reach $US4 trillion annually by 2030 from around $US1 trillion now. That makes this one of the great financial opportunities in history.

This bank, ANZ, recently held an investor day on its Environmental Sustainability Strategy and the focus was on that opportunity. Chief Executive Shayne Elliott described the transition as “super cycle” that “will drive immense opportunities … in decades to come for both us and our customers”.

ANZ’s position is that it accepts climate change is a financial risk, and a shared challenge for customers, governments and the financial sector. But also an opportunity.

According to Elliott, “the biggest role we can play is through our financing, services and advice – backing customers who have the right plans and commitments in place”.

{CF_IMAGE}

ANZ is hardly alone. According to Oliver Wyman in a note prepared after COP26 “more than 450 firms in the financial services sector across 45 countries that represent more than $US130 trillion of financial assets have committed to align their activities to transitioning to net zero and to work to deliver the $US100 trillion investment needed to achieve net zero over the next three decades”.

“The scale and significance of the announcement should not be underestimated,” according to Oliver Wyman. ‘Firms representing 40 per cent of the financial system have committed to set concrete, science-based, net zero-aligned interim targets for portfolio emissions, back them up with credible transition plans and actions, and report progress regularly.”

The good news is the financial sector has weathered the immediate crisis of the pandemic and is actually in good shape. The bad news is things are not going back to normal with digitalisation, artificial intelligence and myriad other tech challenges. And then there’s global warming…

It is these challenges which will determine the next generation of winners.

Andrew Cornell is Managing Editor of bluenotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

Share

anzcomau:Bluenotes/Banking,anzcomau:Bluenotes/social-and-economic-sustainability

2022 looms as watershed for financial sector

2021-12-08

/content/dam/anzcomau/bluenotes/images/articles/2021/December/ACColumn2021wrap.png

EDITOR'S PICKS

-

It’s not capitalism that is driving global warming and growing inequality, it’s the humans making the rules behind it. And they can change them.

24 November 2021 -

Financial services companies have a clearer framework for sustainability investments in the wake of the COP26 conference in Glasgow.

18 November 2021