-

China’s decision to force the breakup of the financial arm of Jack Ma’s Ant Group, hiving the hugely successful Alipay off into a separate joint venture, reflects the new focus on distribution of wealth under the Chinese government.

But it’s not the only sign the seemingly inevitable breaching of the wall of traditional finance by Big Tech companies may itself be facing enormous disruption.

"The Chinese Communist Party emphasised the priority of greater financial equality through the economy by making sure huge companies… don’t garner too much power.”

Along with these measures in China, Google has abandoned long held plans to launch its own banking service, Plex, and the threats from Apple and Amazon seem, for the moment, to have moderated. Even on the startup front, the fintech assault has dispersed: most recently Monzo, one of the UK’s highest profile “neobanks”, was refused a banking licence in the US while the developing trend of fintech startups being acquired or networked into incumbents continues.

However, new threats to banks do continue to emerge. The US postal service has become the latest in a long history of post offices to see banking as a potential way to enhance revenues in the franchise. The Financial Revolutionist reported “the US Postal Service is launching a pilot program in four cities in an effort to deliver financial services to underserved Americans”.

Idiosyncrasies

In its decision, the Chinese Communist Party emphasised the priority of greater financial equality through the economy by making sure huge companies such as Ant don’t garner too much power and become too central in the social economy.

“(it is) necessary," President Xi Jinping said, to "reasonably regulate excessively high incomes, and encourage high-income people and enterprises to return more to society”.

These developments all have their own idiosyncrasies, whether that be governmental, corporate or regulatory. But taken together they complicate the narrative that Big Tech’s scale, financial resources, customer experience expertise, data, and network power would render traditional financial institutions nothing more than service providers.

Ant and Chinese rivals including Tencent, which owns WeChat Pay, are actually the most advanced tech companies in the world when it comes to integrating financial services into a much broader social media ecosystem.

They bring together ecommerce, instant messaging, mobile payments and financial services, deep networks and an extraordinary body of customer knowledge into an ecosystem far more complex and valuable than any bank.

It’s not just a Chinese phenomenon, of course. That’s why Amazon, Google and Apple have all deeply embedded at least some financial services offerings into their own ecosystems whether they originated in ecommerce, search or devices.

{CF_INFOGRAM}

Innovation and stability

Globally, regulators have recognised Big Tech poses new challenges for financial stability and monetary and fiscal policy if these non-traditional – that is, less regulated - players become more powerful. (Although there is always a tension between innovation and stability.)

In the words of François Villeroy de Galhau, governor of the Bank of France, “our role is obviously not to stop innovation. it’s to build trust in innovation. [But] if left unregulated, innovation can decrease financial stability, and there also is the issue of market concentration and of customer protection”.

The global regulator, the Bank for International Settlements (BIS), has just released a review of the growing body of rules and guidelines looking to tame Big Tech called Big Tech Regulation: What is going on?

“Several regulatory initiatives have emerged in China, the European Union and the United States to address new challenges presented by Big Techs,” the report says.

“The initiatives generally seek to achieve a balance between addressing the different risks posed by Big Techs and preserving the benefits they bring in terms of market efficiency and financial inclusion. While recent initiatives constitute important steps in addressing risks posed by Big Techs, additional regulatory responses might be needed.”

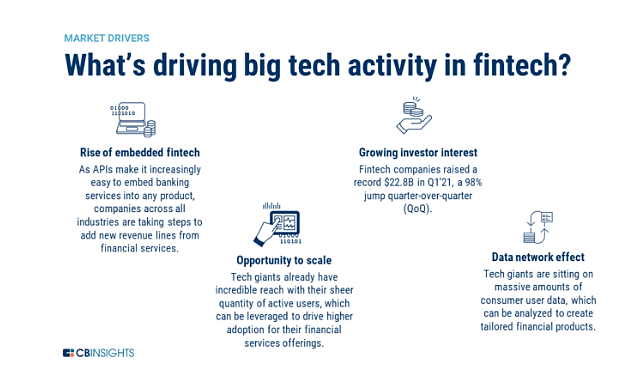

The potential threat of an invasion by Big Tech is increasing and nicely summarised by tech intelligence service CB Insights.

“Eager to turn the ongoing fintech boom into an advantage, Big Tech companies (Facebook, Apple, Google, Amazon) have been taking a number of strategic steps to grow their market share in financial services,” CB Insights found.

“From digital banking and lending to budgeting and payments, tech giants are revamping their financial services offerings through partnerships with legacy institutions and in-house solutions that fit into their wider product ecosystems.”

{CF_IMAGE}

“Tech giants already have the capacity to not only offer improved banking services but also scale quickly within their large user bases. In Big Tech’s race to become the go-to app for banking, shopping and connecting, legacy banks face the continued threat of being further pushed out of the financial system.”

Partnering to embed

But while they are even more active, CB Insights discerned a trend towards a less adversarial approach: “Apple and Google are already partnering with banks to embed banking into their services, while Amazon is seeking out institutional lenders to expand its loan offerings. These partnerships present a win-win situation for tech giants and legacy names alike and help boost customer attraction and retention.”

Nevertheless the threat is real – and implicit in the shifting regulatory approach by the Chinese government. In that case, the state is imposing explicit limits on the market power of Big Tech companies to entwine themselves in the deep working of the economy and the lives of its citizens.

As reported in the Financial Times, Chinese regulators, having ordered Ant to separate from its main business, now want the company’s lending units — Huabei, which is similar to a traditional credit card, and Jiebei, which makes small unsecured loans — to become a new entity with outside shareholders.

Critically, the FT says Ant must turn over the user data “that underpins its lending decisions to a new and separate credit scoring joint-venture that would be partly state-owned”.

The CCP perceives Big Tech as a challenge to the state while CB Insights sees the growing threat to Big Tech poses to “legacy banks”.

{CF_INFOGRAM}

But regulatory and state interventions aside, why might Big Tech be hesitating at the gates of the banking citadel? In Google Plex’s case, part of the reason is age old internal corporate jostling around strategy and resources – two champions of the project have gone.

What’s in it for me?

But the more fundamental reason comes back to the old SWAT analysis: what’s in it for me? What are the costs and benefits? It seems many in Big Tech see greater opportunity and lower costs in working with banks rather than against them.

Aser Blanco, who runs Google Cloud’s US financial services business, told the global bank tech conference Sibos this week the company wants to focus on supplying banks with cloud-based services to help drive profits out of the customer data banks generate.

“Google has stated many times it has no interest in becoming a bank,” said. “But we think we can help with the transformation of [banks]”.

There’s more to be gained from partnering with banks rather than competing directly with them – difficult enough with regulation and launch, trust and marketing costs. But also running the risk of alienating some of the major customers of its Cloud services.

Andrew Cornell is Managing Editor of bluenotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

Share

anzcomau:Bluenotes/Banking,anzcomau:Bluenotes/technology-innovation

Big Tech bank invasion halted at the moat

2021-10-13

/content/dam/anzcomau/bluenotes/images/articles/2021/October/read-ACColumn.jpeg

EDITOR'S PICKS

-

Decentralised finance – or DeFi – isn’t just for online crypto traders. Large financial institutions must take note.

8 October 2021 -

Australia’s payments system is large, diverse and very complex. And globally interlinked. So has regulation kept up with the pace of innovation?

1 September 2021