-

Although the world of contactless payments has exploded in Australia, for some cash remains the payment method of choice.

The COVID-19 pandemic has clearly accelerated the transformation of banking and payments in this digital age.

"In 2020, there was a 22 per cent reduction in volume and 12 per cent reduction in value of cash withdrawals from ATMs.”

According to eminent economics professor Jeffery Sachs, in six months we achieved what would have normally taken 10 years in terms of adopting technology and working remotely. The more people work and buy remotely, the more comfortable they become with using digital platforms.

The payment ecosystem is evolving. Contactless payments continue to rise and cash payments diminish; debit cards are accelerating and credit cards declining. Even newer technologies like mobile wallets and buy now, pay later (BNPL) schemes are all rising rapidly. People are increasingly doing away with physical cards and relying on mobile phones for payments.

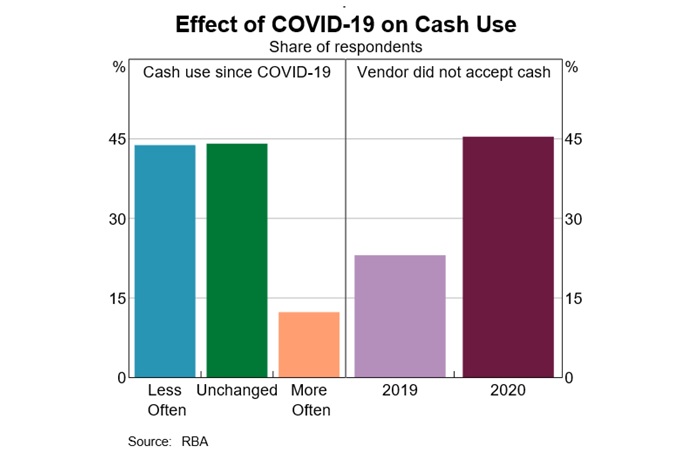

According to the Reserve Bank of Australia (RBA), 23 per cent of Australians surveyed in October 2020 said they had used cash for their most recent face-to-face purchase - down from more than 30 per cent previously.

{CF_IMAGE}

Of those who said they avoided using cash, 45 per cent had come across a business that wouldn't take it. The RBA estimates only 4 per cent of businesses refuse to accept cash outright although many more did what they could to discourage it.

2007 research by the RBA into household payment patterns showed cash was used in the majority of transactions up to $A41. By 2016, this had fallen to $A12 and by the 2019 cash was reported as being the major payment tendered for transactions up to just $A4.

Banking on digital

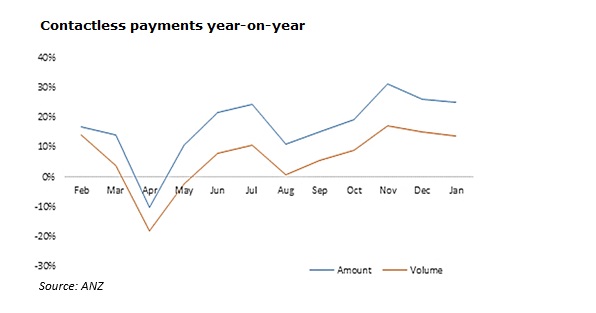

At ANZ, we also found these trends playing out in a similar pattern. In 2020, there was a 22 per cent reduction in cash volume and 12 per cent reduction in value of cash withdrawals from ATMs.

At the same time, there was significant growth in contactless and digital wallet spend. Between January 2020 and January 2021, contactless payments increased 14 per cent in transaction volume and 25 per cent in transaction value.

{CF_IMAGE}

Over the same period, digital wallet payments increased by 68 per cent in transaction volume and 92 per cent in transaction amount. This was mainly driven by increases in spending on groceries, retail and recreation (including restaurants, fast food and liquor).

Customers also turned to banking remotely with ANZ app data between May 2020-2021 showing a 24 per cent increase in total transaction volumes. Almost 440,000 customers registered for the app for the first time and at the end of May the bank reached 3.62 million registered users.

Logins to the app also exceeded 1.2 billion, averaging 92 million logins per month. In March 2021, the bank recorded the highest number of logins in a single month at 100.5 million.

Customers are also using internet banking to check balances, view transaction history, pay bills, transfer money, view statements and more. In a typical day for ANZ’s internet banking platform, we would see 2.14 million active customers (up nearly 10 per cent year-on-year), 840,000 logins and nearly $A975,000 in total transaction value.

Holding onto cash

So, it would seem at many levels the previously slow death of cash accelerated with COVID-19, right? In some ways yes but in other ways no. Here in Australia a puzzling paradox has emerged.

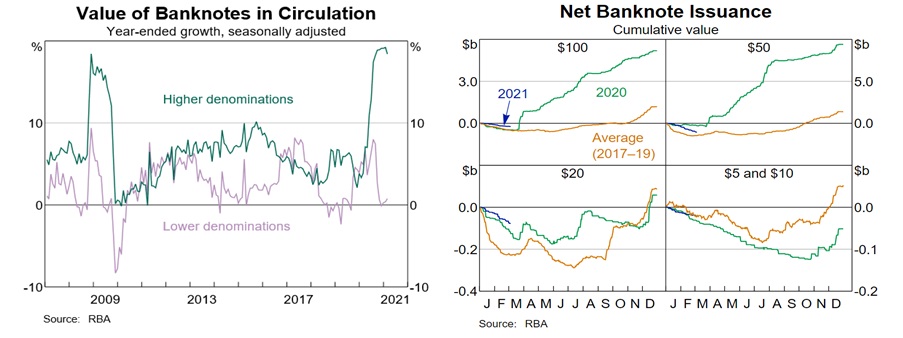

Despite the trends mentioned above, the levels of cash in circulation grew in 2020 and there is now more cash in the system than ever before.

{CF_IMAGE}

The amount of cash currently in circulation has reached $A94 billion, growing by $A11 billion during the pandemic.

RBA Governor Philip Lowe told a parliamentary committee some people seem to be wanting to keep extra physical money at home. Meanwhile, Deloitte noted low interest rate environments added to the desire to hold onto physical money, fuelled by fear of recession.

So big was demand for cash during the pandemic, the RBA opened its "contingency" distribution site twice – once in March and once in July - to send $A50 and $A100 notes to banks who requested them. At the same time, banks held back on returning poor-quality notes to the RBA in case they were needed. The value of cash in circulation – calculated as the value of notes issued in excess of those returned - soared 13 per cent per cent during 2020 according to the RBA.

The value of cash

All this begs the question: if data show use of cash in transactions is declining rapidly then why do some people still hold onto it?

In early 2020, ANZ commissioned a review of cash logistic programs globally which highlighted the unique and valued attributes of cash.

Some of these attributes included 100 per cent availability and reliability, anonymity and direct settlement without the need for a technical infrastructure. This might go some way in explaining the continued use of cash even when provided an alternative.

The report also noted some people prefer cash for reasons of privacy, security and convenience. Others live in areas where inadequate mobile phone coverage and frequent electricity outages make cash the most reliable way to pay. This is certainly true in Australia where geographic isolation is a real concern in our regional and rural areas. Research by the RBA similarly found 5 per cent of respondents noted no other way to pay and 5 per cent noted poor internet access.

ANZ and RBA data would suggest cash, to some degree, is still king for older Australians, those living remotely and the vulnerable.

The RBA study also highlighted regional and remote residents were higher users of cash than metropolitan residents. Those who live in regional areas also tended to be older and have inferior internet access relative to capital city dwellers. These factors too are associated with higher cash use.

Similarly, lower socio-economic households had significantly higher use of cash and if cash were removed the vast majority of heavy/intermediate cash users will experience major inconvenience or genuine hardship.

Beyond that, in regional and remote Australia cash is also used heavily in agriculture – particularly through wholesale produce and livestock markets.

Cash in hand

As a society and major bank, it is incumbent on ANZ to continue providing cash services to these customers and the businesses who serve them.

Major industry sectors including retail, gambling and hospitality are still relatively heavy recipients of cash. By virtue of time, they often have well established cash management routines with their financial institution, usually involving tellers and couriers who could be staff or professional security services.

However, although most business customers are happy with the efficiency of cash, the true cost of this management remains largely hidden.

It remains difficult to accurately measure the cost of cash management but there are some obvious costs such as time management, reconciliation and servicing cash. Most businesses are cognisant of the security risks that arise when dealing with cash, with most having well managed mitigation strategies in place.

Emerging payments

Beyond the ongoing challenges and implications of the pandemic, it’s clear cash must remain accessible as a public good and made efficient to use to ensure the older and vulnerable members of community have access to payments. At the same time, as a sector it’s important to collectively help all people have better access and capability with all emerging payment options.

The Bank for International Settlements sees long term trends in a similar way.

“Looking ahead, developments could speed up the shift toward digital payments,” the BIS explains. “This could open a divide in access to payments instruments, which could negatively impact unbanked and older consumers. The pandemic may amplify calls to defend the role of cash - but also calls for central bank digital currencies.”

Globally there have been a number of attempts for collective solutions to servicing business and customer needs with limited success. Perhaps learning from other sectors like Uber and enhancing the way businesses of all sizes manage cash to their place of business is the key.

Despite technology and digital payment ecosystems contributing to the reduced need for cash, there will always be a need for physical money from individuals who prefer it and businesses looking to meet these customer’s needs – banks included.

Jodie LeeTet is Value Stream Lead, Cash Strategy at ANZ

This article was produced with support from Michael Daddo at The Shannon Company

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

Share

anzcomau:Bluenotes/Payments,anzcomau:Bluenotes/Banking,anzcomau:Bluenotes/COVID-19

Banking on the future of cash

2021-07-07

/content/dam/anzcomau/bluenotes/images/articles/2021/July/LeeTetCash_banner.jpg

EDITOR'S PICKS

-

The move away from cash emerged as one of the biggest digital shifts from the pandemic as consumers seemed to fully embrace mobile wallets.

20 October 2020 -

Consumers and businesses have turned to contactless payments in the wake of the COVID-19 pandemic and a greater focus on hygiene.

30 July 2020