-

At the start of 2020, looking ahead at the year in banking, EY anticipated a range of significant headwinds with margins under continuing pressure, ongoing geo-political uncertainty and increasing competition from new, non-traditional players.

We didn’t anticipate a global pandemic, one that would present the banks – and economic markets more broadly – with even more volatility and uncertainty.

"In this environment, banks need to strike the right balance between managing risk and transforming for future growth.”

Yet in the face of substantial new challenges thrown up by COVID-19, the banking industry demonstrated its ability to manage change in the face of unprecedented crisis and market upheaval. Locally and globally, banks stepped up to play a leading role in helping sustain economies by facilitating income support programs and assisting vulnerable customers.

In Oceania, the banks rapidly responded to requests for loan deferrals from individuals and small businesses. Had that not occurred, many people could have lost their homes and their livelihoods. This, in turn, provided the chance to help rebuild some much-needed consumer trust in the sector.

As banks look ahead into the new year, the trajectory of the world’s recovery remains critical to their profitability and growth. Subsequent waves of the virus and accompanying lockdowns could require more provisioning and put a further squeeze on lending books – scenarios banks should be preparing for now. On the other hand, the pandemic is also highlighting new opportunities for banks to accelerate digital innovation programs, connect more deeply with their customers and drive greater sustainability.

In this environment, banks need to strike the right balance between managing risk and transforming for future growth.

Oceania outlook

Profitability across Oceania banks dropped sharply in 2020 but the good news is the local sector’s overall financial position remains sound, supported by strong capital and liquidity levels, as well as the early policy measures put in place to address COVID-19 stresses.

Asset quality has so far proven particularly resilient, with Oceania delivering the lowest non-performing loans ratio globally, at just 0.3 per cent. However, this is an area the banks will need to watch closely over the coming months.

The full effects of the economic downturn are yet to play out and the true scale of distressed loans is unlikely to be revealed until forbearance programs and income support measures draw to a close. In addition – despite signs of an unexpectedly strong Australian recovery and significantly improved gross domestic product (GDP) forecast – the ultra-low interest environment could still undermine banks’ performance in the months ahead. Indeed, the potential for negative rates in New Zealand is still on the table and credit growth is likely to remain relatively subdued for some time. In this ‘lower for longer’ environment, managing costs and credit risk will remain among the top priorities for local banks over the coming year.

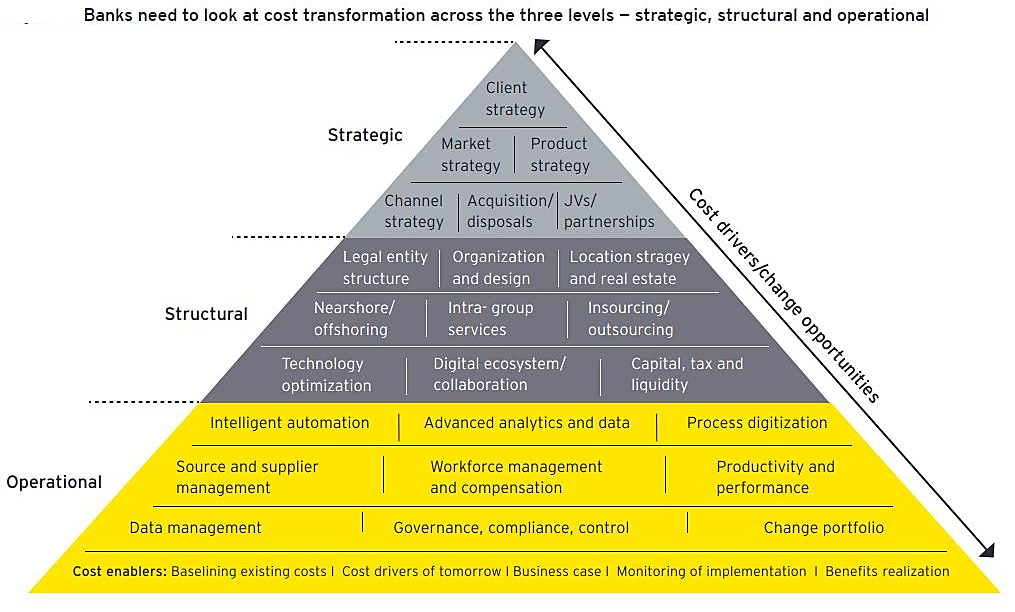

Tackling costs has been a key challenge for the local banking sector for some time, however the weakened economic environment brings extra pressure to accelerate productivity initiatives and expedite process simplification and digitisation as a mechanism for controlling costs.

Banks that consider the crisis as an opportunity for holistic cost reduction across three main areas — operational, structural, and strategic — can find strategic ways to align resources and maximise potential. To that end, banks will be looking for initiatives that deliver measurable cost-out benefits and lower risks; no easy task given complex legacy systems and traditional silos of operation.

{CF_IMAGE}

Expect to see Australian and New Zealand banks continuing to invest in areas such as technology, process automation, digitisation and process simplification, to help reduce costs and enhance the customer experience into 2021 and beyond.

When it comes to managing credit risk, banks will need to make greater use of management judgement, stress testing and new modelling approaches. Banks can build greater strength across the enterprise by expanding testing for scenarios around cyber, third parties, technology, operations and regulations, while developing new performance metrics. The pandemic has shown you cannot predict all risks but building resilience means building an organisation that can respond with agility and flexibility when they occur.

By investing in advanced data analytics, banks will be better able to measure and monitor credit risk and identify at risk customer segments. Banks should also be focusing on overhauling their collections models with a large number of customers likely to need customised payment strategies and solutions over the coming months.

Opportunity from uncertainty

However the wide-scale disruption, globally, has also led to new possibilities. In 2021, as we move further into the recovery phase of the pandemic, banks can take steps to position themselves for future growth by seizing this once-in-a-generation opportunity to transform, accelerating their investment in technology and embedding more agile and scalable business models.

Banks must build new revenue streams and, to do this, they need to find ways to give customers the products and services they want in a post-pandemic world and deliver these in the ways they demand. The rapid acceleration in digital adoption by both retail and small-to-medium enterprise customers, bought on by the pandemic, is an opportunity for banks to rethink their models and reimagine the customer experience.

The last few years have seen new entrants and non-traditional players lead the race to banking innovation, showing outstanding customer experience and agility can be achieved at a low cost. But the COVID-19 crisis has exposed some weaknesses in parts of the challenger sector where, despite rapid customer growth, many have yet to achieve the scale and profitability that help build resilience in tough market cycles.

Traditional banks, which already have the scale to help insulate against the current tough conditions, should be using this opportunity to take the lead on the innovation front. To do this, they will need to take a customer-centric approach and proactively engage with consumers to design and offer alternative digital products and services that are more customised and better suit their personal and business finance requirements. Platforms and ecosystem models that allow for seamless interaction between customers, banks and third parties should also be considered as part of the broader business strategy.

While the past year has shown us that no one has a crystal ball view of the future, those banks that take the opportunity now to accelerate their digital and customer transformation will be better positioned to weather whatever new challenges lie ahead in 2021 and beyond.

Tim Dring is Banking and Capital Markets Leader for EY Oceania

The views expressed in this article are the views of the author, not Ernst & Young. This article provides general information, does not constitute advice and should not be relied on as such. Professional advice should be sought prior to any action being taken in reliance on any of the information. Liability limited by a scheme approved under Professional Standards Legislation.The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/Banking,anzcomau:Bluenotes/Innovation,anzcomau:Bluenotes/Digital,anzcomau:Bluenotes/COVID-19

Transformation opportunities exist amid disruption

2021-02-16

/content/dam/anzcomau/bluenotes/images/articles/2021/February/DringOutlook_banner.jpg

EDITOR'S PICKS

-

Australia’s banks must accelerate digital transformations to help the economy recover from the COVID-19 pandemic.

19 January 2021 -

Corporate, commercial and small-medium enterprise banking services are ripe for innovation and need to start planning now to stay ahead of the curve.

15 January 2021