-

The future of farming is bigger. Much bigger.

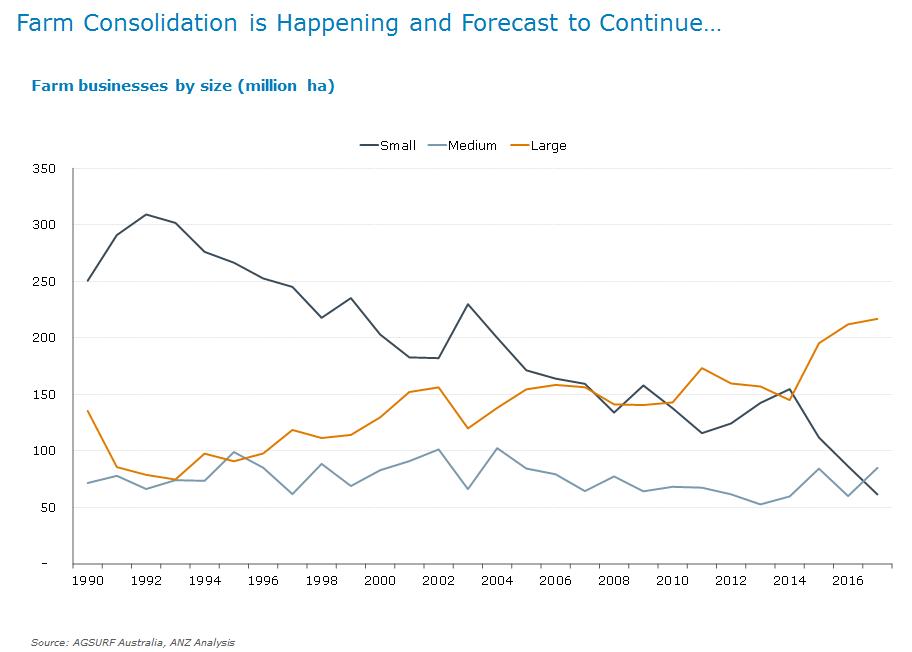

New ANZ analysis shows trends in Australian farming are towards consolidation amid a reallocation of resources across the country from smaller, less-efficient farms to larger-scale operations.

" Over the past 20 years farm consolidation has occurred alongside a correlated increase in productivity.”

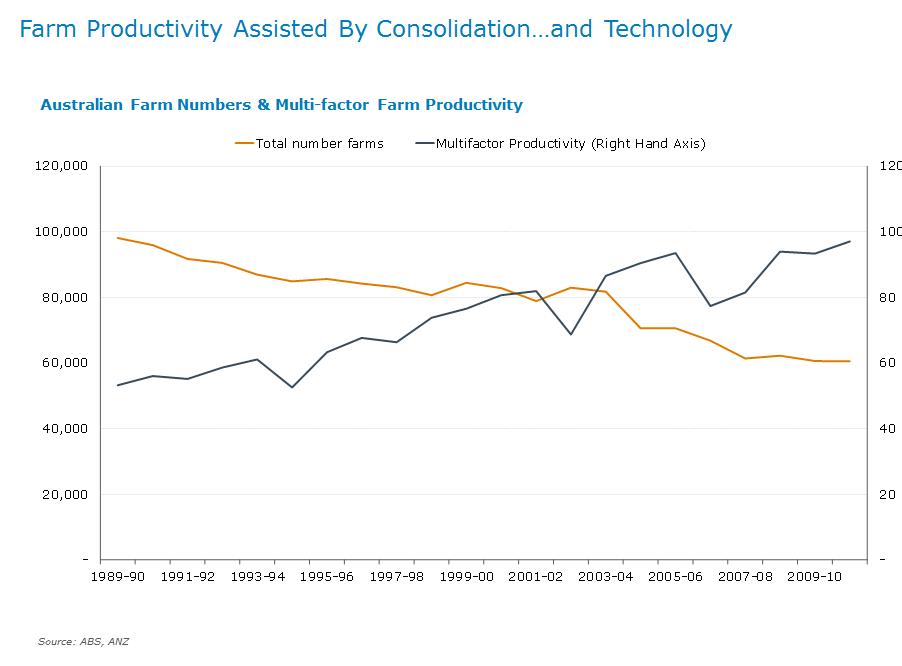

Over the past 20 years farm consolidation has occurred alongside a correlated increase in productivity, ANZ’s latest agriculture report The Track Ahead suggests.

While scale is often attributed as the key driver of increases in farm productivity, ANZ research shows since 1995–96, 62 per cent of the increase in agricultural output can be attributed to farm consolidation leading to greater access to technology - with tech arguably the key driver of the productivity gain as opposed to scale itself.

{CF_IMAGE}

On current trend, the number of farms in Australia will shrink from today's 123,000 to 110,000 in 2025 and just over 85,000 in 2050.

Meanwhile, The Track Ahead finds Australian agriculture’s five-largest commodities face strengthening global competition which may impact the National Farmers Federation’s $A100 billion 2030 target, according to the report.

{CF_VIDEO}

That target is certainly achievable but growing global competition means heightened levels of collaboration and innovation are required from all stakeholders.

While our farmers remain world-leading, our international competitors have improved their quality, volume and reliability, strengthening their overall market position.

{CF_IMAGE}

The Track Ahead suggests this trend is evident across a range of commodities including cattle, horticulture, wheat, sheep and wool, and dairy which together represent about 68 per cent of Australia’s agricultural production value.

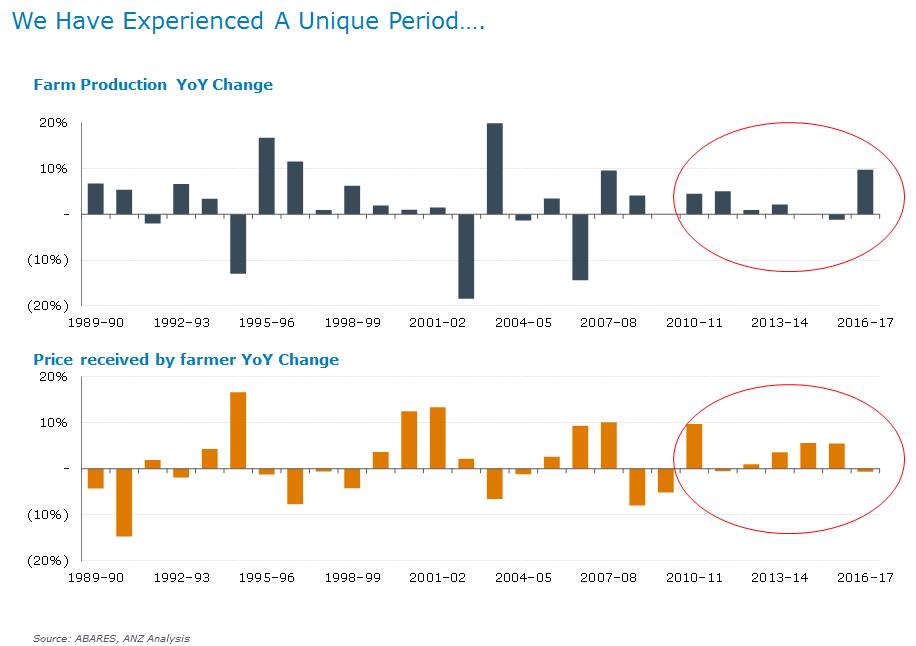

Since 1989, Australian agriculture’s gross value production has grown at an average of 3.6 per cent annually – a rate which would see it reaching about $A89 billion by 2030.

Ongoing capital injections are critical to this growth. ANZ modelling shows 1.5 per cent annual growth in capital investment, combined with a 3 per cent rise in productivity, would grow the sector to $A97 billion in production by 2030.

{CF_VIDEO}

{CF_IMAGE}

Best steps

It’s never the wrong time ask fundamental questions about the direction of the industry to optimise planning for the future. Here are three of the biggest:

- How do Australia’s major agri stakeholders best work collaboratively in a free market and unsubsidised environment? This includes producers, processors, industry bodies, external stakeholders, regulators and, importantly, banks.

- What is the optimal policy for maintaining a competitive, efficient and innovative industry, while ensuring major disruptions such as drought or trade bans do not set the sector back for many years?

- With detailed analysis of Australia’s agri export competitors, including their forecast volume growth and breadth and quality of their output, how should Australia be positioning itself for 2030? For example, in which categories will Australia be a bulk soft-commodity supplier versus a niche provider?

Chapters

The recent history of Australian agriculture can be seen in a series of chapters; from the introduction of grain to the development of merinos and other sheep breeds; the transition from horses to machinery; the development of irrigation and advanced water infrastructure.

The sector has also undergone a series of major regulatory and structural changes. At a regulatory level the creation and ultimate dissolution of single-desk marketing or buying bodies has arguably had a greater impact on the sector than any other.

These ranged from the reserve price scheme for wool, to the single desks for wheat, barley and sugar, plus the state-based dairy desks.

At the farm-gate level, fewer but larger farms undeniably bring enhanced levels of efficiency and profitability, due not just to scale but to the passion of innovative and successful farmers.

There will always be a place for the smaller family farm that targets this scale and appreciates the need to be profitable and sustainable, or who have other interests.

The impact of new technology and capital will open up farming to a whole suite of new operators. While the visions of many new agtech developments are grander than the reality at this point in time, the developments will gradually provide less-skilled farmers with the capacity to run an operation.

At a high level, Australia continues to adjust the balance of different agri sectors, driven by varying factors including demand, investment and climate.

Wheat

Record wheat harvests across the world have kept downward pressure on Australian prices outside of local drought years.

Despite increasing export tonnage to major markets like Indonesia and Vietnam, Australia’s share of value of these markets is under increasing competitive pressure.

Black Sea-region producers are serious competitors on world wheat markets, and while economic and structural issues are present, their scope for yield and cost of production improvements will assist to place their produce competitively in the international market.

Beef

Global beef consumption is increasingly reliant on imports and is driven by strong consumption growth in emerging markets.

South American beef is forecast to dominate global production as improvements in supply chain, quality and quantity of product continue.

Strong Australian production and stable consumption growth implies a large exportable surplus from the US, meaning continued competition for Australian beef. Around 70 per cent of domestic produce is destined to export markets – primarily to four countries (Jap an, South Korea, US and China) which account for over 75 percent of exports (both volume and value).

Sheep

The global sheepmeat market is particularly unique in that Australia has only one major export competitor, New Zealand. Together, throughout 2017, Australia and NZ accounted for 71 per cent of global sheepmeat trade despite accounting for only 8 per cent of global production.

The NZ sheep flock, like Australia’s, has experienced a significant decline since the 1990s. Where Australian sheep farms gave way to wheat and cropping operations, NZ sheep farms were largely converted to dairy operations and, to a lesser extent, beef operations. In total size, the NZ flock is some one-third the size of the Australian flock, at around 27 million head.

In terms of competition, NZ sheepmeat is present in all of Australia’s top 10 export markets for both lamb and mutton, however New Zealand exports are heavily focused on two key markets, being China and the EU.

A shortening of supply of NZ sheepmeat and a redirection of product towards China has presented opportunities but Australia has been unable to fill the gap.

The EU market is a high-value premium-cut sheepmeat market for Australia, and the recent announcement of initial negotiations toward an Australia-European Union Free Trade Agreement that began in mid-2018 is welcome news for the industry.

Mark Bennett is Head of Aus Agribusiness at ANZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

-

-

Share

anzcomau:Bluenotes/Agriculture,anzcomau:Bluenotes/business-finance

The future of farming is big - literally

2019-01-23

/content/dam/anzcomau/bluenotes/images/articles/2019/January/BennettTrackAhead_banner.jpg

EDITOR'S PICKS

-

Industry collaboration is starting to improve the bottom-line profitability of farmers in the Sunraysia region.

15 November 2018 -

Drought is not new and neither is the strength of Australia’s farmers.

22 October 2018