-

Home ownership, the digital divide and fears around inheritance are three of the biggest factors driving concerns around financial wellbeing among older people, new research has found.

The Financial Wellbeing: Older Australians report isolates the factors associated with financial wellbeing in older Australians including financial capability and stable income streams.

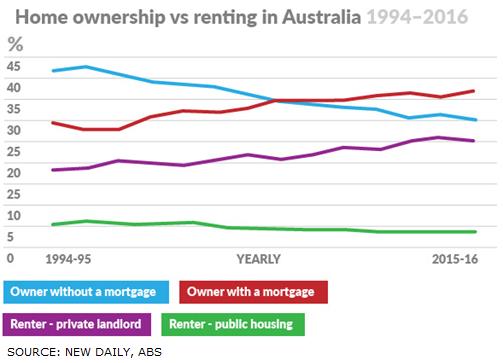

" Owning a home is one of the most-important indicators of financial wellbeing for older people - which does raise concerns as the rate of home ownership is declining.”

It finds the overall higher financial wellbeing score of elderly Australians may mask the hardship faced by a significant number of older people – especially women.

The report, together with a companion report outlining the impact of ANZ’s MoneyMinded program, the 2018 MoneyMinded Impact Report, analyses in depth the financial wellbeing of older Australians through a series of surveys, interviews and focus groups. You can click HERE to read the report.

The works bring together researchers from RMIT University, the University of South Australia, leading advocates for the elderly and ANZ’s partner organisations including AnglicareSA, Berry Street, Brotherhood of St Laurence, The Benevolent Society, The Smith Family and Uniting Vic/Tas.

Home

Research into older participants in MoneyMinded found the number-one priority for wellbeing was ‘coping financially now or in the future’ and there is increasing evidence home ownership is of paramount importance for the financial wellbeing of older Australians.

“The [ANZ] report confirms categorically owning a home is one of the most-important indicators of financial wellbeing for older people which does raise concerns as the rate of home ownership is declining,” RMIT University Professor Roslyn Russell says.

Research shows 75 per cent of pensioners own their own home but consideration should be given to the 25 per cent who do not.

“Older Australians who are renting are in trouble,” National Seniors Australia Chief Advocate Ian Henschke says. “Especially older women renting alone.”

About 40 per cent of renters aged 65 and over are below the poverty line. And, among those renters living alone, the poverty rate rises to 60 per cent.

{CF_IMAGE}

The issue of rent is one of the key tenets of the Fix Pension Poverty Campaign, an advocacy initiative led by The Benevolent Society in partnership with National Seniors that seeks to ensure the 1.5 million older Australians who receive the full age pension can live their lives with dignity and wellbeing.

“If there are financial products that help people live better in retirement, we have to look at them,” Henschke says.

Digital divide

In his role at National Seniors Australia Henschke spends a lot of his time in the media and at large discussing all manner of financial issues for older Australians – including superannuation, reverse mortgages, worries over dwindling retirement savings and what he calls “pension poverty”,.

A big issue is the digital divide many older Australians face as banking products and services increasingly move to digital models.

“One in eight Australians is not connected to the Internet,” he says. “The majority of them are older Australians.”

The Financial Wellbeing: Older Australians report concurs with University of South Australia focus-group research about this fear of technology, particularly of smart phones and apps for banking.

One of four research project leads at UniSA Dr Braam Lowies warns financial services organisations not to brush off this disconnect with older Australians.

“We cannot afford to say ‘oh this problem will be gone in 15 to 20 years’,” he says. “This is a massive cohort of clientele that holds a lot of wealth.”

The research found on average 82 per cent of older Australians do their banking using a desktop computer, comparable with younger cohorts. Far fewer (32 per cent aged 65 or over) use mobile banking or apps on a phone or tablet device.

“Mobile banking is physically problematic,” Professor Russell says. “(People) are worried about doing something without meaning to.”

The over 65s still want face-to-face customer service or to talk on the telephone “especially around financial matters”, Henschke says.

Citing the Australian Government’s new Pension Loans Scheme - a voluntary reverse-equity mortgage that offers older Australians an income stream to supplement their retirement income - Russell says if digital literacy is low and trust in internet banking is low “it is difficult for older people to find out about products that maybe useful for them”.

Inheritance Impatience

The research also highlighted fears around financial abuse (or, as it is euphemistically being referred to, ‘inheritance impatience’) by family and other parties and decreasing freedom to make their own decisions. Thirty one per cent of MoneyMinded facilitators interviewed identified financial abuse as an issue faced by older clients.

The 2019 National Elder Abuse Conference will take place in July, following the much-anticipated release of the National Elder Action Plan by the Council of Attorneys-General (comprising the Commonwealth and all State and Territory Attorneys-General).

National Seniors Australia is also working with the Australian Banking Authority (ABA) around the issue of elder abuse.

“It is very difficult to detail the level of financial abuse but we do know the rate is much higher than the reported rate and we suspect it is around 5 per cent,” Henschke says. “It can be subtle or it can be clear cut abuse … the majority of it is coming from sons or daughters.”

Tracking the financial wellbeing of older people will continue, Professor Russell says.

“We believe this is the first time data using the Elaine Kempson scale or any of the other financial wellbeing scales have been used to focus on an older cohort. The most-important indicators for financial wellbeing could change as the next generation ages,” she says.

Emily Ross is an author, journalist and editor

Click here to read the Financial Wellbeing: Older Australians report and 2018 MoneyMinded Impact Report.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/social-and-economic-sustainability,anzcomau:Bluenotes/financial-literacy

Three massive factors for senior financial wellbeing

2018-11-29

/content/dam/anzcomau/bluenotes/images/articles/2018/November/RossMM2_banner.jpg

EDITOR'S PICKS

-

Many factors contribute to a person’s financial wellbeing – including some surprising ones.

19 April 2018 -

We speak with Elaine Kempson, professor and global pioneer about the state of financial wellbeing in Australia and NZ.

19 April 2018