-

The flattening yield curve in the US is beginning to turn heads. The good news is - so far - we are someway short of the yield curve flagging an imminent hard landing in the economy and sharemarket.

It’s a pretty simple story - the market expects better returns from long-term bonds than short ones. When the difference disappears, people start worrying. There’s a pretty good reason for that – a flattening curve is a fairly reliable indicator of an approaching recession.

"The market expects better returns from long-term bonds than short ones. When the difference disappears, people start worrying.”

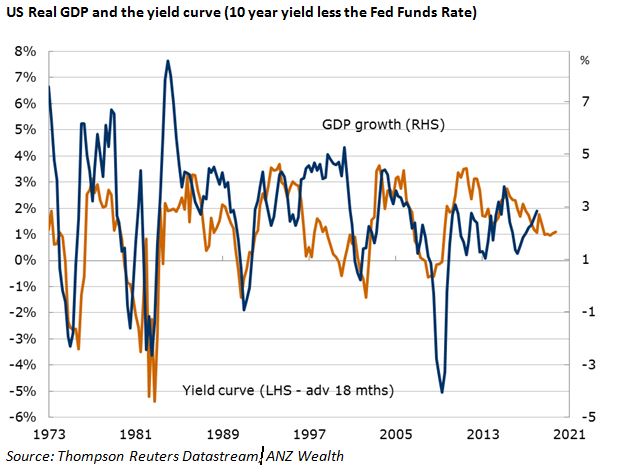

History suggests making a fuss about a flattening yield curve is time well spent. When we look at US economic downturns over the past 40 years, every time the yield curve has inverted the economy has ultimately gone into extended negative territory.

{CF_IMAGE}

ANZ Wealth’s analysis suggests a moderation in economic and earnings growth is in train in the US given economic tightening measures put in place to date from the US Federal Reserve.

The Fed will be the key to how this story ends.

Inverted

The “yield curve” shows the difference in the compensation investors are getting for choosing to buy shorter or longer-term debt. Investors generally want more for locking away their money for a longer time period due to the greater uncertainty that comes with a longer time frame. So yield curves usually slope upwards.

A yield curve goes flat when the premium - or spread - for longer-term bonds drops to zero. This happens when we see the rate on a 10-year bond as no different as the rate on shorter term securities, typically a cash rate or a two-year bond. If the spread turns negative, the curve is ‘inverted’.

The yield curve is seen by many to be the most reliable predictor of the economic outlook. However, the lead time is long (typically around 18 months) and can be variable, sometimes raising doubts whether its forecasting track record will continue to hold.

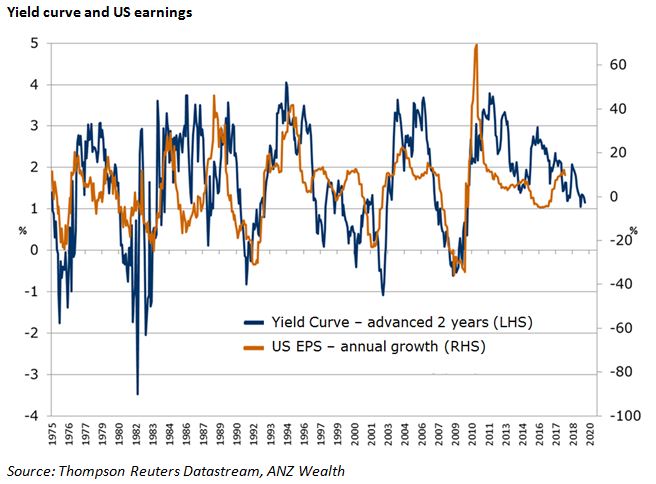

In many cases it’s more than just whether the yield curve is inverted. The yield curve’s accuracy is quite amazing: the degree of steepness of the curve correlates with the pace of growth, so a flatter curve indicates slower growth and a steeper curve means a faster pace. Not surprisingly it also closely correlates with earnings on the US market.

{CF_IMAGE}

As you can see from the first two charts, while there can be shorter spells of inconsistency, during the 1990s there was a longer phase when the yield curve’s downbeat economic forecast of slower growth didn’t eventuate - the yield curve flattened but the economy and earnings remained stronger than expected.

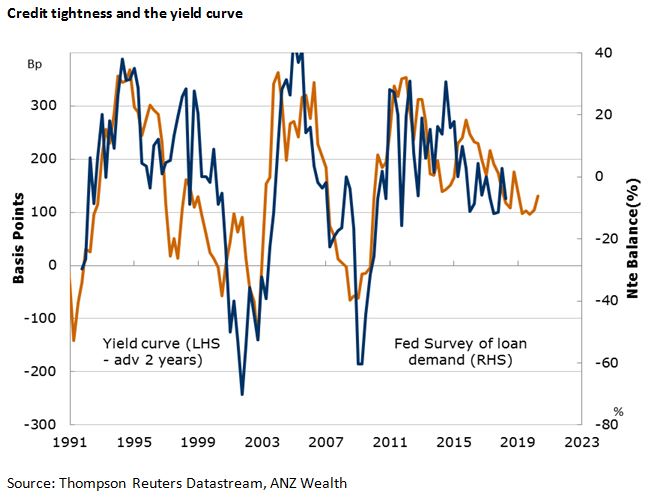

So what was different? Credit demand was unusually strong in the 1990s and this in turn supported the economy and share market.

Even so, the yield curve did eventually invert with economic growth and earnings slipping into recession. So far this cycle looks closer to normal and so we expect the economy to slow after the usual lags.

{CF_IMAGE}

Inflation matters

After the 2007 financial crisis the Fed cut the federal funds rate - the short-term rate at which banks can borrow from each another - to near zero levels. This expansionary policy supported businesses and consumers to borrow and get the US economy back into growth.

The Fed first moved off this in late 2015 and since then has slowly lifted the rate six times, signifying more-normalised policy designed to keep inflation in check. With the US unemployment rate at its equal-lowest point in almost five decades, wage growth is expected to rise in the period ahead.

The yield curve is already suggesting the US economy will slow by mid next year and, along with it, earnings growth will stall.

It’s worth asking the question: does the Fed really have to raise short term rates much more? This should be expected only if inflation looks likely to be well clear of 2 per cent, the Fed’s target, and therefore sees a need to slow the economy significantly. There’s no need to do it otherwise.

As for markets? What’s happening now is consistent with our ‘good-times fade’ analysis. ANZ Wealth’s expectation remains for the market to not wholly take on board the 15 per cent growth in current US earnings.

Mark Rider is Chief Investment Officer at ANZ Wealth

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/Economics

Listen up: what the yield curve has to say

2018-06-29

/content/dam/anzcomau/bluenotes/images/articles/2018/June/RiderYield_banner.jpg

EDITOR'S PICKS

-

As the spotlight falls on the US yield curve, ANZ Research looks at what this means for credit risk.

28 June 2018 -

ANZ Wealth’s CIO looks at predictions for a volatile market this quarter.

12 June 2018