-

I’ve written before this year on how this is as good as it gets for global growth.

The worldwide economy has reached peak growth due to - among many factors - low household saving rates, the combined effects of monetary tightening out of both the US Federal Reserve and The People's Bank of China, along with the unwinding of quantitative easing around the world.

"[The] global economic cocktail makes many countries and asset markets unusually sensitive to downside surprises.”

Volatility in asset prices amid tightening liquidity, an enormous US debt issuance program, trade tensions, geopolitical realignment, chronic political instability and constrained credit growth in some economies have also played a role. In addition, much of the world is dependent on exports to drive activity.

This global economic cocktail makes many countries and asset markets unusually sensitive to downside surprises, either in their own economies or elsewhere.

In the absence of an easing in Chinese liquidity, ANZ Research struggles to see how the outlook for the next year or so is substantively different from a rinse-and-repeat of the first half of 2018 – including volatility, sentiment showing heightened sensitivity to geopolitical and trade risks and economic growth which is reasonable but never seems to quite reach lift off.

Easy company

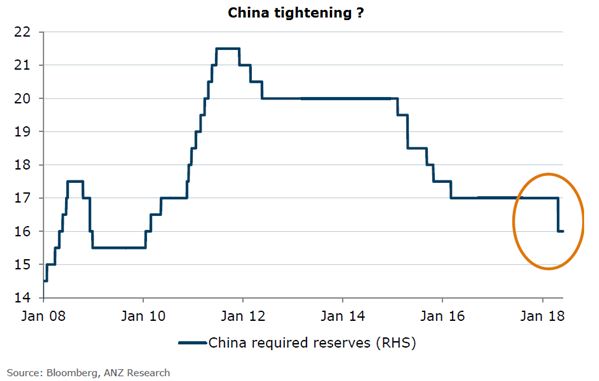

With China accounting for a third of global growth the focus is likely to increasingly turn to the stance of Chinese liquidity policy.

The year 2017 was the first since the global financial crisis where Chinese and the US bond yields tightened concurrently.

But since then China has begun to manage liquidity more deftly. China’s large April reserve requirement ratio cut was seen as a surprise – could it be the first hint of a more permissive liquidity stance?

{CF_IMAGE}

If this is indeed the first tentative shift towards easier liquidity, this would support inflation and commodity prices.

An easing in China would help boost the most-cyclical sectors of the Chinese economy (including housing from the second half of the year), contribute to stronger money supply growth and strengthen inflation and commodity prices.

{CF_IMAGE}

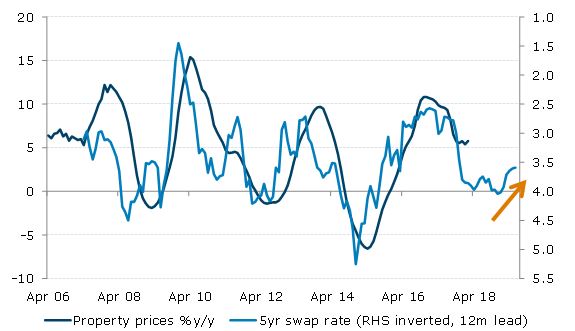

Easing would likely also have global implications by helping global growth, adding some reflationary impulse to markets via stronger demand and higher commodity prices and benefitting risk appetite and - potentially risk-sensitive assets such as the Australian dollar and currencies in Asia.

Richard Yetsenga is Chief Economist at ANZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

Share

anzcomau:Bluenotes/Economics,anzcomau:Bluenotes/asia-pacific-region

Is China the only light at the end of the tunnel?

2018-06-12

/content/dam/anzcomau/bluenotes/images/articles/2018/June/YetsengaChina_banner.jpg

EDITOR'S PICKS

-

The China-US armistice is good news but the crux of the matter has yet to be addressed.

22 May 2018 -

Let’s welcome the global recovery and take advantage of it - but the chances of further improvement are minor.

18 January 2018