-

Ten years ago the New Zealand Government launched KiwiSaver, the world’s first auto-enrolment, opt-out, national retirement savings scheme. Now, on the precipice of its second decade, changes to the scheme must be considered if it is to best serve New Zealanders into the future.

KiwiSaver was introduced with the aim of lifting New Zealand’s low savings rate and encouraging more people to save for their retirement. As we look back at the past decade, KiwiSaver has come a long way, transforming the superannuation landscape in New Zealand.

{CF_IMAGE}

To ensure it continues to support New Zealanders’ retirement outcomes, ANZ Investments (ANZ New Zealand’s investment management business) has released Dollars and Sense: A Decade of KiwiSaver, a comprehensive report which suggests improvements to the savings initiative.

" New Zealanders are starting to think about how much they will need to fund a comfortable retirement."

The report was released in tandem with a survey of 1,000 people where we asked the public what they thought of KiwiSaver and what they would like to see changed.

ANZ Investments’ recommendations

• KiwiSaver should be compulsory

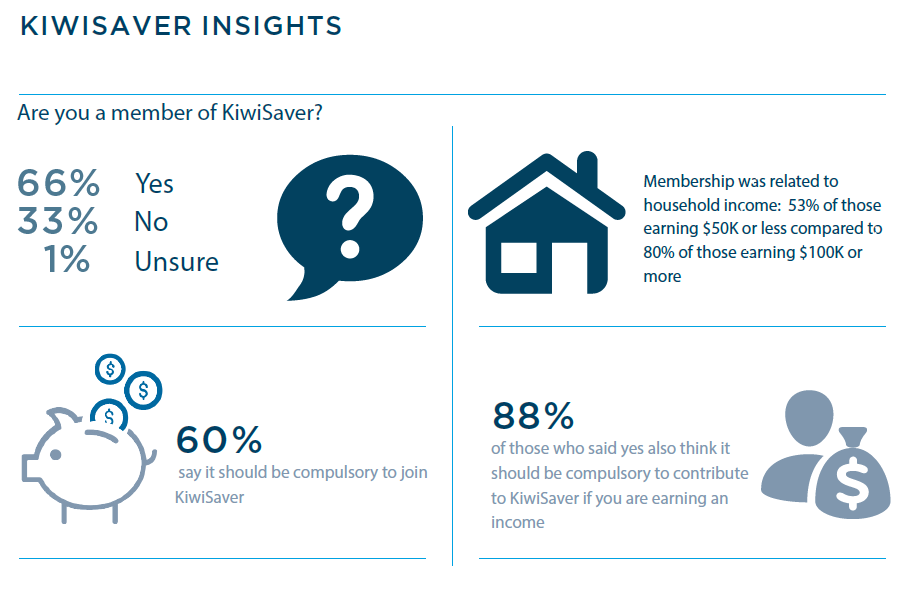

That is an idea which was supported by our research. Sixty per cent of respondents supported compulsory KiwiSaver while only 33 per cent said no and 7 per cent were not sure.

Among those who supported making KiwiSaver compulsory, 88 per cent said contributions should be compulsory if you are earning an income.

Interestingly, the percentage of people who supported making KiwiSaver compulsory was similar to the proportion of respondents who told us they were KiwiSaver members.

Sixty six per cent said they had enrolled in KiwiSaver. A third told us they had not joined, while 1 per cent of people were not sure if they were members or not.

The results suggest people who are KiwiSaver members now view it as integral to their savings plan.

The research also found 80 per cent of people from households with an annual income of $NZ100,000 or more were KiwiSaver members.

That compared to 53 per cent of people from a household with an annual income of $NZ50,000 or below.

This raises questions about whether KiwiSaver is reaching many of the people who need it the most and illustrates why ANZ Investments believes making the initiative compulsory is a good idea.

But we also recognise much more needs to be done than just making KiwiSaver compulsory.

• Members should have more flexible employee contribution options

At the moment, employees who are KiwiSaver members can opt to contribute 3%, 4% or 8% of their salary, with a contribution from their employer which will generally be 3% of the employee’s before-tax pay. But we know saving can be tough for many people, especially with modest wage growth and rising living costs.

To provide more flexibility, ANZ believes an option should be introduced for members’ employee contributions to be automatically increased by small increments (e.g. by 0.25 per cent, 0.5 per cent or 1 per cent) up to a capped rate.

Equally, some people might prefer to reduce their contributions when money is tight, rather than stopping saving altogether. There should be options for reducing employee contributions by small increments (e.g. by 0.25 per cent, 0.5 per cent or 1 per cent) for a set period.

{CF_IMAGE}

Milestones and challenges

There is an important difference between the superannuation models in New Zealand and Australia.

Launched fifteen years earlier in 1992, Australia implemented a compulsory superannuation initiative. On the other hand, in New Zealand, it was decided KiwiSaver would not be compulsory.

Instead, people would be automatically enrolled when they started a new job and they could decide to opt out within 56 days from the day they started their new job.

In 10 years, nationwide uptake has grown substantially as employers and members alike commended KiwiSaver for providing an easy way to save.

Today, over 2.7 million New Zealanders are enrolled in KiwiSaver – far exceeding the government’s initial expectations – and collectively, members have saved over $NZ40 billion. KiwiSaver has also helped members buy their first home and learn more about investment markets.

But there are also plenty of challenges. While over half the population are KiwiSaver members, around 375,000 working age New Zealanders still have not signed up and some who have enrolled are not making any contributions.

Others are saving some money, but not enough to receive the full annual Government contribution (eligible KiwiSaver members who contribute up to $NZ1042.86 annually will receive 50 cents for every dollar up to $NZ521.43 from the Government). We are also seeing a rise in the number of members looking to access their savings for hardship reasons.

• Changes should be made to the current ‘contributions holiday’ facility

Many employees who are KiwiSaver members are opting to suspend their contributions, taking what is called a ‘contributions holiday’.

Any employee who has been in KiwiSaver for a year can then opt to suspend their contributions for between three months and five years. There is also no limit to the number of times they can do this.

ANZ Investments favours changing the name of the ‘contributions holiday’ to the less alluring ‘savings suspension’ and reducing the maximum length to one year, thus requiring members to reapply annually if they want to suspend their contributions again.

• Members should select more-balanced risk profiles or follow a life-stage model

All new employees are automatically enrolled in KiwiSaver. But if they don’t actively choose which KiwiSaver scheme they want to be with and if their employer doesn’t have a preferred scheme, Inland Revenue will allocate them to one of nine default providers where their contributions will be placed into a default conservative investment fund.

These funds are generally low-risk and low-return, with a much higher exposure to income assets such as bank deposits and fixed interest investments and a lower exposure to growth assets such as shares and listed property.

While this may suit some people’s risk tolerance and investment timeframes, it may not help everyone reach their retirement goals.

People need to ensure they’re making active choices about their KiwiSaver accounts. ANZ Investments believes all default funds’ risk profiles should be more balanced or follow a life stage model rather than a conservative risk profile.

This will provide better long-term outcomes to those default members who may be hard to reach or choose not to make an active choice.

• KiwiSaver scheme providers should work with the government to increase transparency around fees and improve member education about returns after fees

In recent months, New Zealanders and the financial services industry have been engaging in a debate around KiwiSaver fees.

Our research shows younger people in particular are placing a lot of emphasis on finding a provider which offers fees as low as possible.

To address this, the government has mandated KiwiSaver scheme providers disclose the fees they charge in dollar amounts in their annual member account statements.

That way members can see how much they’re paying for the services and benefits they receive in return – ANZ Investments strongly supports this. But we also believe it is essential people consider the most important measure – returns after fees.

• Financial ‘health checks’ should be provided to members at various stages to ensure they continue to meet their retirement goals and know how to use those funds when they reach retirement

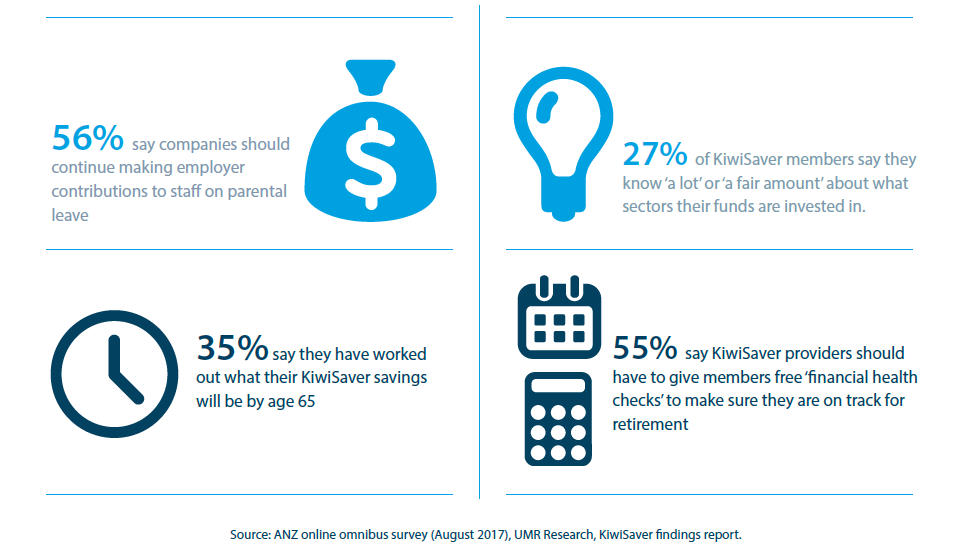

It can be hard to work out how much you will have saved for retirement. This was reflected in our research when only 35 per cent of respondents under 65 said they had worked out what their KiwiSaver balance and other savings might be by the time they retire.

When the remaining 65 per cent were asked why they hadn’t done this, 35 per cent said there was too much uncertainty, 27 per cent said they did not feel they needed to, 24 per cent did not care and 22 per cent said it is too hard or they don’t know how.

To tackle this, ANZ Investments believes providers should grant a free service to investors at specific life stages to help them identify their savings and retirement goals.

Health checks, tools and resources should also be provided to groups most in need of support, such as non-contributing members, women and those nearing the retirement age.

Just over half of poll respondents agreed it should be compulsory for KiwiSaver providers to give members ‘free financial health checks’ to see if they are on track for their future retirement (e.g. at 40, 50 or 60 years of age).

It’s also essential to ensure members can decide the best way to ensure their KiwiSaver savings last them through their retirement.

ANZ Investments believes providers should encourage members approaching retirement to set a plan or seek advice for how they will draw upon their savings. Sixty two per cent of respondents said they would like their provider to give them access to free professional advice on the options for withdrawing funds.

Continuing the conversation

At ANZ, we created Dollars and Sense and commissioned this research to spark a conversation about retirement savings. We believe this is something important to all New Zealanders.

As the country’s largest KiwiSaver scheme provider we have always spoken up for our members, raising issues and advocating for changes which will help deliver them better retirement outcomes.

Through our report we hope to keep the conversation going and encourage change nationwide.

Craig Mulholland is Managing Director of Wealth at ANZ New Zealand

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

Share

anzcomau:Bluenotes/your-money,anzcomau:Bluenotes/business-finance

The next steps for Kiwisaver

2017-10-02

/content/dam/anzcomau/bluenotes/images/articles/2017/October/kiwisaver.jpg

EDITOR'S PICKS

-

Does the ATM – once considered the ultimate banking innovation – even have a future?

27 September 2017 -

New Zealand – not unexpectedly – has a hung parliament after the weekend election. What can the parties’ own words tells about how a coalition may form?

25 September 2017 -

High European prices due to falling product and low inventories are affecting the domestic market.

19 September 2017