-

What does 'digital' in banking mean in practice? Robots with Artificial Intelligence replacing humans? Bank vaults moving to the Cloud? Branches replaced by mobile phones? Biometric ID assuming the role of photos, PINs and signatures?

There is, of course, no one answer – but digital certainly doesn’t mean no humans, no branches or just shifting processes online.

ANZ’s chief executive Shayne Elliott makes the point it’s wrong to just see digital as a way of streamlining an existing process – in effect just maintaining the same paper trail of hand-offs but doing it virtually.

" Customers are interested in solving financial problems, not being either physical or digital." Andrew Cornell, bluenotes Managing Editor.

{CF_IMAGE}

Rather, it is the hand-off process itself which needs to be fundamentally rethought. If the ambition is provide a foreign exchange transaction for a company in another country, the challenge is to reshape the bank to solve the question “how does the company want to use FX funds?” more efficiently. Not just let’s try and have digital Letters of Credit and faster settlement.

{CF_IMAGE}

Financial services needs are many and varied and so the digital alternatives will be equally diverse. There’s no shortage of surveys interrogating whether consumers and businesses want more automation but the findings all boil down to an essential purpose: they want something done, not a digital experience for its own sake.

For example, communications application developer Avaya commissioned YouGov to survey more than 5,000 banking customers in four countries – Australia, India, the UK and the UAE.

Avaya found given the choice of only one channel, 28 per cent of the 1,153 Australians surveyed would prefer access to a complete list of services via their bank’s web site, speaking to a real person only if they really have to.

More than half, 54 per cent, regularly use online banking, behind only the UK’s with 60 per cent, while only 36 per cent usually visit their branch - the joint-lowest with the UK.

Younger customers were not surprisingly more likely to use mobile services – 58 per cent of 18 to 24-year-olds compared with just 13 per cent in the 55+ category – yet 22 per cent of Australians still prefer to visit branches.

The Indian data however were particularly insightful: while more than half, 51 per cent, of Indian respondents said they regularly visit their branch, the highest of the four countries surveyed, only 13 per cent said they prefer to do so – by far the lowest of the four.

I’d argue what that illustrates perfectly is customers are interested in solving financial problems, not being either physical or digital. Obviously, Indian customers have particular financial needs but they would prefer them to be fulfilled outside a branch. I’m guessing on a mobile phone or at least online.

Efficient experience

As Peter Chidiac, Avaya’s managing director for Australia and New Zealand noted, what customers value is an efficient experience.

For example, regardless of how they choose to contact their bank, Australian customers want their problem resolved at the first point of contact. The most common customer complaint is being kept waiting for a long time on the phone, cited by 21 per cent.

So making a call centre more digital, perhaps employing AI, is meaningless if a problem can’t be solved in one call.

For a different perspective, Suvo Sarkar, head of Retail Banking & Wealth Management at Emirates NBD, wrote in Gulf News an opinion piece called “Technology is making banking human again”.

{CF_IMAGE}

While his perspective may not resonate so much in Australia, he outlined a vision where your bank is your “friend” on social media.

“In its latest avatar, an online banking channel is personalised to your profile, so you get spending analysis, saving and investing widgets and relevant insights,” he wrote.

“You can buy a banking product just as you shop for everything else, with a click. On a personal wall, you can post to customer care, chat with your adviser or schedule an appointment with your relationship manager while you pay a utility bill.”

Sarkar explained Emirates NBD’s 'FaceBanking' feature, calling it high-tech and high touch. Essentially the channel exploits video calls.

“Instead of interacting with a machine, a human banker is online, face to face, for your every need," he wrote. "Banks like Emirates NBD now use instant video and live chat in a secure environment to share documents, explain product details and even deliver personal loans.”

Sarkar’s is far from the only bank exploring this but essentially the challenge is the same: for some interactions, humans are happy to deal with technology; for others they want humans. But in all cases, they don’t want to 'bank' they want something done.

And that brings us back to digital. All these new 'old' ways of improving banking, preserving the human element and delivering a less frustrating customer experience do essentially rely on being more digital.

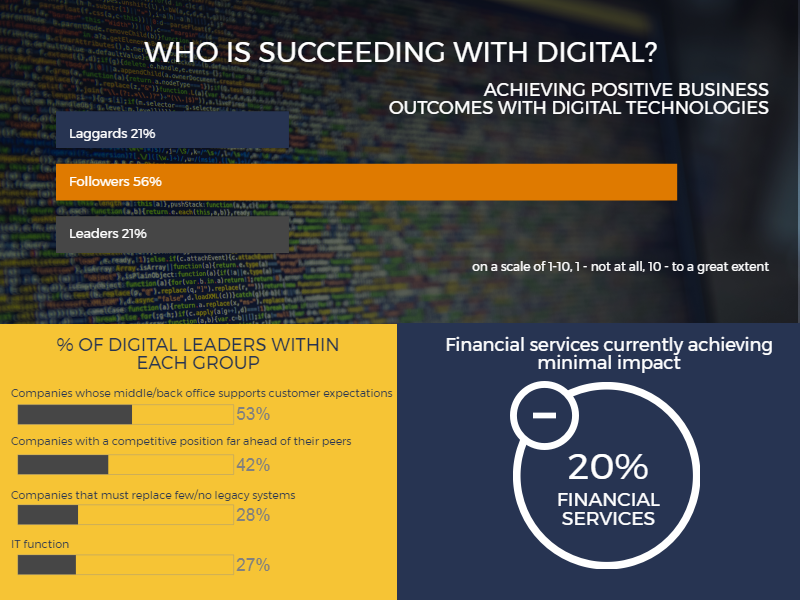

But the financial services sector remains a laggard in this regard.

Digital agenda

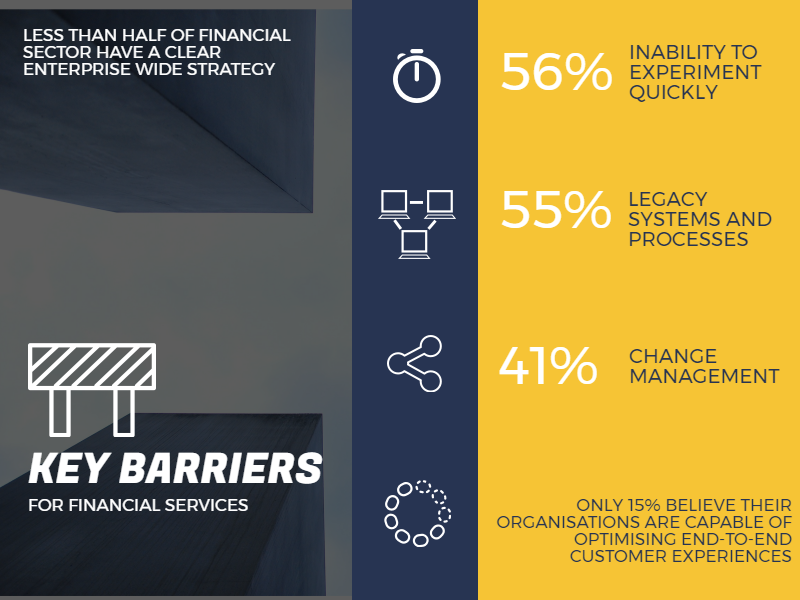

Research from the Harvard Business Review and Genpact Research Institute called “Accelerating the pace and impact of digital transformation: How financial services views the digital agenda” highlighted ongoing challenges in the sector, notably an inability to experiment or the burden of legacy systems and processes, preventing the effective use of digital technologies.

Less than half of financial services sector respondents said their companies have a clear, enterprise-wide digital strategy. Leadership was a critical issue with too much fragmentation and reluctance to abandon existing structures.

Financial companies aren’t delivering digital-driven value to customers as they don’t link end-to-end user experiences beyond the web-enabled front end, especially with intractable legacy systems and processes. Only 15 per cent of financial services firms say they do this well.

This is something commonly cited anecdotally when customers compare their financial institution with Amazon or Spotify or Apple: parts of the experience may be very satisfying but rarely is the end-to-end.

{CF_IMAGE}

In the survey, financial firms cited key barriers as an inability to experiment quickly (56 per cent), legacy systems and processes (55 per cent) and change management (41 per cent).

Many financial services firms believe they are on their way to embracing digital but only a minority, 20 per cent, believe they are harnessing these technologies successfully. And only 15 per cent believe their organisations are capable of optimising end-to-end customer experiences.

Meanwhile, for those succeeding in their digital initiatives, a vast majority say digital technology has had significant impact on their companies’ cost to serve (90 per cent), customer loyalty (75 per cent), and revenue growth (75 per cent).

There’s certainly no shortage of technology start-ups and established firms looking to help financial institutions – or help others compete with them – with the digital shift.

CB Insights' latest fintech report notes a “massive market opportunity, coupled with shifts in technology, demographics and consumer expectations, has made the idea of disrupting financial services more feasible in the minds of investors and start-ups”.

CB Insights makes the point start-ups are “essentially outsourced R&D” but the stats are pretty outstanding: in the last five years, there have been 38,135 early-stage start-up financings to pursue these experiments.

Standing aside from digital is not a choice. Banks may not be Uber-ed or Airbnb-ed but they can suffer piecemeal erosion of their revenue pools.

CB Insights ask the question “is Goldman Sachs a tech company?” Interestingly, an answer came from another bank in an interview with McKinsey & Co.

Discussing ING’s “agile transformation”, ING’s chief information officer Peter Jacobs said “we came to the realisation that, ultimately, we are a technology company operating in the financial-services business."

"So we asked ourselves where we could learn about being a best-in-class technology company. The answer was not other banks, but real tech firms.”

Andrew Cornell is bluenotes Managing Editor

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

-

Share

anzcomau:Bluenotes/Digital,anzcomau:Bluenotes/Banking,anzcomau:Bluenotes/Innovation,anzcomau:Bluenotes/technology-innovation

Why should banks be digital?

2017-08-16

/content/dam/anzcomau/bluenotes/images/articles/2017/August/humanoid.png

EDITOR'S PICKS

-

For some, the fintech boom never subsided - but it’s clear its momentum and nature have shifted.

2 August 2017 -

ANZ tech GE says on video businesses must align with modern customer expectations.

14 August 2017 -

Hordes of fake identities are being created for the purpose of illegally obtaining credit.

19 July 2017