-

The Reserve Bank of Australia has just released its fourth consumer payments survey, How Australians Pay, and Michele Bullock, the bank’s Assistant Governor (Financial System) sat down with bluenotes managing editor Andrew Cornell to talk about its implications and the future of payments.

{CF_AUDIO}

Screen reader users press tab 3 times to reach the play button.

She covered a wide variety of topics:

"We don’t really understand [the reasons for people’s use of cash] in enough detail and that’s the nature of cash.” - Michele Bullock

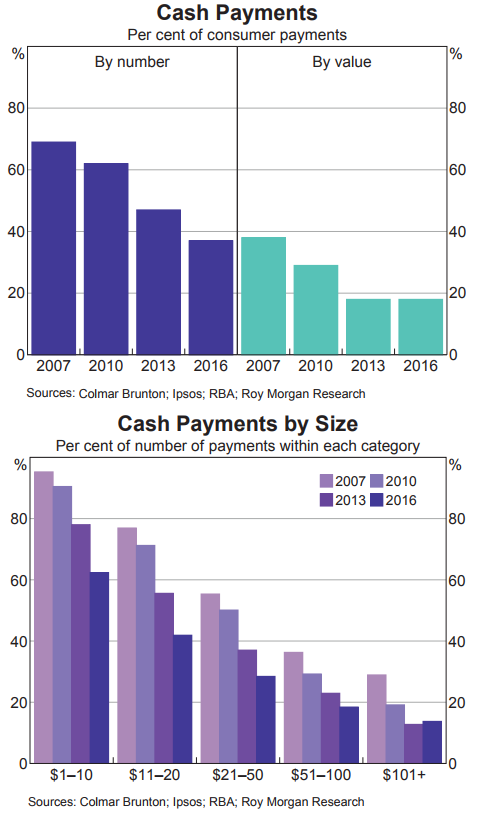

On cash: That’s still the very broad trend and one of the interesting conundrums about this is that, although these sorts of surveys show use of cash as a percentage of transactions as declining, the actual number of bank notes outstanding is still going up. So, there’re two issues here. One is how are people transacting with cash? And then then there’s also cash as a store of value.

We don’t really understand (the reasons for people’s use of cash) in enough detail and that’s the nature of cash. What we find, what we know from this survey, is there are a lot of people who hold cash as a store of value, they hold it in places other than their wallet.

And when you ask them why they hold it they say for emergency reasons or they say for budgeting purposes. So, the sorts of reasons some people like to hold a bit of cash and feel uncomfortable they don’t have some in their wallet.

The rapid spread of tap’n’go: It’s very quick, you can make a very quick low value transaction. Whereas in the past if you had to stick your credit card in and put in your PIN it was a bit slow.

You thought, well I’m not going to bother doing that for a cup of coffee. Now you can, you can do that for a tap and go. So, what we’re observing in the new survey is a movement towards lower value transactions being done by credit and debit cards.

It’s really a demonstration of what I call the network effective payments. So, I think the difference back in the 90s – and I remember this myself – was that you were being issued with cards but there weren’t many merchants that took them.

So, you didn’t tap very often because it just wasn’t obvious who took them. I think the big change was when the big supermarkets started taking tap, and once that happened and people had the tap and go in their hand, then the network effect kicked in and people became familiar with it and they started to use it.

Even as recently as the 2013 survey, tap and go was sort of happening but not near as much as it is now. In fact, around two-thirds of all card payments now are contactless. So, I think it’s a really powerful demonstration of the network effect, that you need both sides, merchants and consumers, involved in order for something to take off.

Payments policy: For the Payments System Board and the bank, really what we’re looking at is issues of competition and efficiency. But also safety.

And the way we would typically operate is by talking to systems in the market, talking to stakeholders, determining where there might be material efficiency and competition gained, and seeing if the market can address that by itself or whether there might be some sort of market failure that requires the bank to step in.

Our preference is not to regulate, our preference really is to let the market work and where there are issues for the industry to self-regulate. But having said that, there are occasions where we have stepped in in the past and a couple of those are interchange and surcharging.

Asian payment trends: There are some countries in Asa who are still very heavy cash users. Some of them are sort of countries that are still middle income, sort of developing countries. (But) surprisingly one of them is Japan.

Japan is a very heavy cash-using society. It has a high currency to GDP ratio relative to quite a few countries. Having said that there are many which are also well on the way to electronic payments.

Hong Kong has long had a transport card that also acts as a prepaid sort of card around shops. Singapore’s reasonably well advanced in electronic payments, as is Korea. And China of course is moving along with some very innovative payment systems, so they’ve got Alipay and WeChat which have worked into developing payment systems surrounding their social networks.

Everyone’s sort of heading in similar directions but it depends very much on where you start from. We started from a base where we had relatively high penetration of terminals in Australia.

So that’s made it easier for us, electronic terminals, it’s made it easier for us to rollout the contactless. The contactless actually I think in Australia is reasonably high penetration.

I’s possible (QR codes, widely used in China) will come to Australia. Again, I think it depends very much on where you’ve come from.

QR codes in Australia I don’t think took off as they did in other places overseas and I think the other point is that the QR code solution, if you don’t have a very heavy penetration of electronic terminals, allows merchants to take payments using these QR codes.

But as I said, we’ve actually got historically a very heavy penetration of electronic terminals, which goes back to the EFTPOS system in the 1990s. And so, we’ve sort of built on that rather than building a completely new payment system based on another sort of system, the QR codes.

The New Payments Platform: Let me just make a couple of points about cash. There was two areas in which cash I think was sort of superior if you like or had benefit to it that certain other payment methods didn’t have. One, it was quick for small value transactions.

As we’ve already talked about actually, contactless has sort of solved that problem now. But the other way that cash had advantages over many other payment mechanisms was you could make person to person payments very easily on the spot in real time.

I can give someone cash and they’ve automatically got the money. At the moment that’s not so easy using electronic payment methods because it often has to go through the bank systems overnight and you might take a day or two before the money can be transferred.

So, I think potentially what the new payments platform is delivering is almost one of the last bastions of cash, which is very quick person to person payments that you can’t do using other methods at the moment, except for cash.

I think you’ll see services develop that offer all sorts of possible real time services to people. I think we’ll still continue to see the use of cash in day to day transactions decline. I still think it will be a relatively important payment mechanism. I think there’s a lot of people who still use it.

The survey tells us that there’re a lot of people who like to use it for budgeting purposes. So, I think there’s still a demand for it. I think we’ll possibly start to see some of the new payment mechanisms coming from overseas.

I wouldn’t be surprised if we see a little bit of Alipay and WeChat. So, it’s gradual I think. I don’t think we’re accelerating but I expect to see similar trends moving forward for the next few years.

Andrew Cornell is managing editor at bluenotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/Economics,anzcomau:Bluenotes/Payments,anzcomau:Bluenotes/Podcast

PODCAST: RBA’s Bullock on cash, payments & policy

2017-08-09

/content/dam/anzcomau/bluenotes/images/articles/2017/August/CornellBullock_Thumb.jpg

EDITOR'S PICKS

-

A cross-industry initiative shows blockchain can cut costs and improve security in bank guarantees in commercial property leasing and beyond.

11 July 2017 -

For currencies, there’s a steamroller coming – in the shape of liquidity.

4 July 2017 -

A decade after the financial crisis, have we learned anything? It’s a crisis which keeps on taking.

5 July 2017