-

Momentum in the New Zealand economy is picking up from a lull over late-2016 to early-2017. This pickup will be modest, with the economy facing capacity constraints and late-cycle economic challenges, two of which are finding skilled labour and keeping excesses in check.

However, business and consumer confidence are elevated, the terms of trade buoyant, fiscal policy is set to turn more expansionary, financial conditions supportive, tourism booming and migration strong.

ANZ Research’s forecasts depict an economy growing at a pace strong enough to continue to gradually absorb spare capacity. But it’s a solid, rather than stellar story. Core inflation will slowly rise, and interest rates too.

"We are expecting the NZ economy to keep on a relatively steady beat.” - Cameron Bagrie

Steady beat

We are expecting the NZ economy to keep on a relatively steady beat. GDP growth is forecast to run at an annual pace of around 3 per cent over the next 18 months (in fact quarterly annualised growth is expected to be stronger in the near-term).

After growth of 3.1 per cent over 2016 as a whole, 2017 growth is forecast to average 2.8 per cent in 2017 and 3.0 per cent over 2018. It is a pace of activity momentum which should:

• continue to see the unemployment rate gradually trend lower (which we see falling to 4.4 per cent by the end of 2018 even though labour supply growth should also remain strong); and

• result in spare capacity continuing to gradually be absorbed (we place trend growth at around 2.75 per cent).

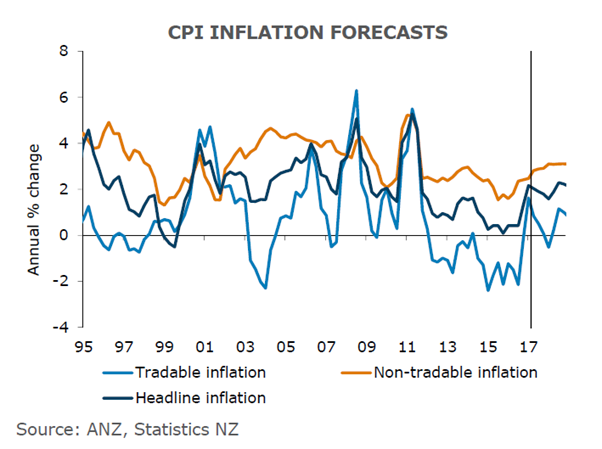

We see inflation pressures slowly broadening. Some measures of core inflation are already at the target mid-point of 2 per cent. However, it is not a broad-based story, and still largely contained to housing. But we do see that gradually changing.

With wage growth forecast to lift off lows, non-tradable inflation should rise too. After averaging 2.0 per cent over 2016, non-tradable inflation is forecast to average 2.8 per cent and 3.1 per cent over 2017 and 2018 respectively.

But there will be plenty of factors that throw headline inflation around. Although non-tradable inflation is forecast to lift, headline inflation looks set to fall back into the lower half of the RBNZ’s 1 per cent to 3 per cent target band over the coming 12 months.

{CF_IMAGE}

This is largely due to the recent plunge in oil prices. While recent lifts in food prices are consistent with the broader soft commodity picture, they also reflect disruptive summer/autumn weather conditions, and some of that should at least partially unwind.

There also remain plenty of questions over the global inflationary impulse. That said, headline inflation is forecast to average 2.0 per cent in both 2017 and 2018.

Cameron Bagrie is Chief Economist at ANZ NZ.

Contributors to this article include Philip Borkin, Senior Economist, David Croy, Senior Rates Strategist, Kyle Uerata, Economist, Con Williams, Rural Economist and Sharon Zöllner, Senior Economist at ANZ NZ.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/Economics

NZ to stay on song

2017-07-19

/content/dam/anzcomau/bluenotes/images/articles/2017/July/NZeco_IMG1.png

EDITOR'S PICKS

-

New Zealand’s forestry sector is experiencing a period of strong returns fuelled by a combination of steady Chinese demand, restrictions in export markets on native-forest harvesting, low shipping costs, a local building boom and a supportive NZ dollar.

21 March 2017 -

New Zealand has reached a mature stage in the economic cycle. Historically, sharp slowdowns have followed such periods - but ANZ research does not believe the cycle is about to roll over and expire.

31 March 2017 -

New Zealand tourism is on a tear with no sign of slowing, driven by ever-higher numbers of Chinese tourists, right? Actually, not quite.

3 April 2017