-

The novel Utopia has just been republished in a quincentenary edition, having been written in 1516 by Sir Thomas More, then a counsellor to Henry XIII, King of England.

More envisaged an ideal utopian society which possessed highly desirable qualities for its citizens. Utopians have no personal property and the houses they live in are kept unlocked at all times. Money does not exist but wealth is accumulated by the government through trade.

"The utopia of a cashless society is merely a mirage.” - Steve Worthington

More’s vision was attractive to early socialists who saw this imaginary society as a blueprint for a socialist nation. These became known as the ‘utopian socialists’, who favored an egalitarian distribution of goods, alongside the total abolition of money in order to achieve perfect social and financial equality.

{CF_IMAGE}

Four centuries later, Animal Farm by George Orwell brilliantly exposed the flaws in the communist view of society. The novel offers a view of human behaviour at odds with the philosophies and principles of a ‘perfect society’ as described in Utopia.

Many advocates of the ‘cashless society’ suggest it could offer a better and more-efficient world, but do they also fail to see how the behaviour of humans means the utopia of a cashless society is merely a mirage?

Mirage

Cash, in effect, has its own Triple-A credit rating. It is broadly speaking acceptable everywhere; it is anonymous (in an increasingly monitored world) and it is authentic: in you can see it, touch it and hence continue to validate its value.

According to a recent survey of over 1,500 Australians conducted in November 2016 by Ipsos for the Reserve Bank of Australia (RBA), cash still accounted for 37 per cent of all consumer payments in 2016 and the median value of cash held in consumers purses and wallets was $A40

Thus, although the share of payments made in cash continues to fall, cash was still used for over one-third of consumer payments and the reasons given by the respondents for holding cash were both for precautionary purposes to fund emergency transactions and for day-to-day transactions, particularly of lower value.

Some 70 per cent of respondents to the 2016 survey also held cash in places other than their purses or wallets. Whilst the majority of participants held $A100 or less, around 3 per cent reported they held over $A1,000, primarily as a store of value.

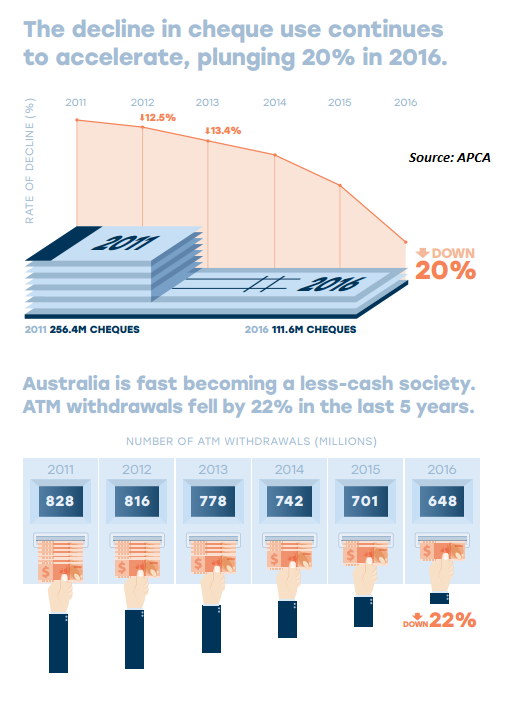

The use of cheques has also continued to decline although 12 per cent of respondents to the RBA survey said they had made at least one personal cheque payment in the year prior. These were mainly for larger expenditures such as household services and utility bills.

Reasons given for using cheques varied. Some merchants preferred to be paid by cheque; there was no alternative other than paying by cheque; and cheques provide a useful record of the payment.

Data from the Australian Payments Clearing Association (APCA) in shows cheque use dropped by 20 per cent in 2016 alone - the largest drop ever recorded. Over the last five years, cheque use has dropped by 56 per cent.

Just over 1 per cent of all payments made in Australia are now made with a cheque. The APCA data reveals other non-cash payments are increasingly popular; transfers (direct credit, direct debit and BPay) have 32.2 per cent and payment cards (credit and debit) have 66.7 per cent, of all digital payments.

Their popularity is underpinned by the use of contactless payments on credit and debit cards; the rise of the subscription economy, where goods and services are paid for by direct debit and in-app payments, such as GoGet and Uber, for services such as car hire and taxis.

Digital wallets

The RBA’s recent 2016 survey also reported the use of digital wallets or mobile phones, accounted for only around 1 per cent of the number of point-of-sale transactions over the week of the survey.

Bearing in mind, mobile wallets in their current incarnation have only been rolled out over the last year or so. Anecdotaly, Apple Pay in particular has shown positve trends for the institutions - including ANZ - which have issued it.

Previous experiments with electronic purses such as Mondex and Visa Cash failed to take off and obviously convincing consumers to adopt new electronic cash alternatives, is a hard road to tread.

The status of gold as a universal commodity and store of wealth; the resilience of the paper cheque and the relatively slow uptake and usage of digital wallets are all examples of behavioural economics at play in the payments world.

Gold may well be the ideal metal for toilets and the ‘gold standard’ no longer underpins the issue of notes and coins, yet the gold price is featured on the daily news programs and it is seen as a safehaven in times of economic uncertainty.

According to the APCA, 77 per cent of Australians own a smartphone and yet mobile payments at the point-of-sale remain relatively rare.

The very success of contactless cards in Australia demonstrates the rapid adoption of their functionality by both consumers and merchants.

The RBA estimates in 2016 around one-third of all point-of-sale transactions were conducted using contactless cards. What then is the additional functionality digital wallets can offer both consumers and merchants to speed up their adoption?

What the utopian view of society and money reminds us is although bank notes and coins may well be inherently insecure and relatively inefficient, it will take more than the introduction of new, more efficient methods of payment, to wean society away from the use of cash. Particularly in its role as an easily accessible and anonymous store of wealth.

An RBA Bulletin paper from the December quarter 2016 issue, considers "cash is expected to remain an important part of the payment system for the foreseeable future". So, it looks like the utopian cashless society will remain just a vision.

Steve Worthington is a Professor at Swinburne Business School

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/technology-innovation/payments

A cashless utopia? Dream on!

2017-06-02

/content/dam/anzcomau/bluenotes/images/articles/2017/June/WorthingtonCash_IMG.jpg

EDITOR'S PICKS

-

The pace of change in the rapidly evolving payments space is news to no one. As the world moves closer to becoming cashless and disruptors offer an increasingly wide number of payment options, the old ways of buying are losing relevance.

18 October 2016 -

In the decades since payment cards entered commerce alongside cash their promoters have struggled to convince a significant minority of merchants the benefits of non-cash payments outweigh the costs.

30 November 2016