-

Just as any debate on the internet inevitably ends up with someone accused of being a character from Triumph of the Will, so any discussion of artificial intelligence (AI) ends up with Skynet from the Terminator movies.

" The right movie to serve as a model for how the interaction of technology and finance might evolve with AI is probably more like Andy Warhol’s Empire than Blade Runner."

Andrew Cornell, Managing Editor BlueNotesBut before the computers form a neural network and take over the world, as the Armegeddonists predict, AI might be capable of lesser but still meaningful corrosion. For example, the European Union’s anti-trust head Margrethe Vesteger recently flagged tougher sanctions on organisations which used AI or clever algorithms to subvert competition, perhaps by setting up web-mediated cartels.

Of course, there are also optimists: Bank of Japan governor Haruhiko Kuroda in a speech AI and the Frontiers of Finance noted “financial services, through efficiently processing large volumes of information, continuously allocate limited economic resources to promising projects, thereby supporting economic development.

“In this respect, AI and big data analytics are considered to have great potential for making the information processing function - which is the fundamental function of finance -even more efficient and advanced, as they enable the generation of more value through processing large volumes of information.”

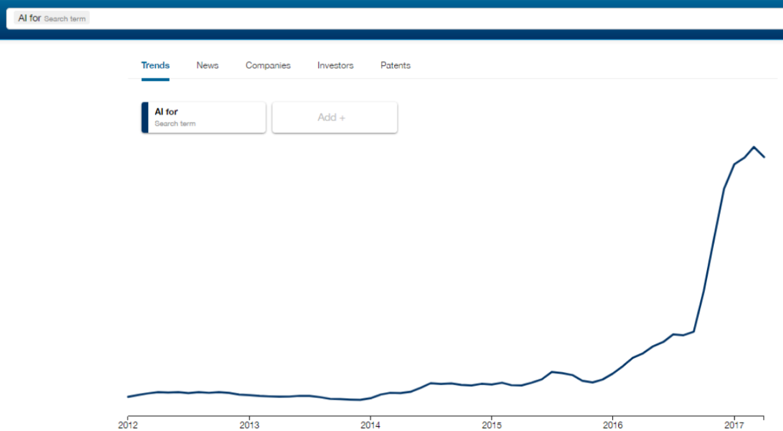

Then there is hype. Venture capital analysts CB Insights recently produced an entertaining list of start-ups professing AI would transform everything from boutique brewing to roti bread making to marijuana growing. Some of these products undoubtedly produce the illusion at least of artificial intelligence…

“Our Trends tool, which analyzes millions of media articles to quantify tech trends, shows how the hype has built around AI for X,” CB Insights said.

{CF_IMAGE}

Reality though is usually more mundane. Even for AI.

In his speech Kuroda implicitly argues the challenge with these new technologies is not always the big questions, it is often the myriad small ones. With AI he draws attention to market distortion, information security, data privacy - those essential process and governance considerations with which any transformative technology has to grapple if it is to obtain and hold a social licence to operate.

So the right movie to serve as a model for how the interaction of technology and finance might evolve is probably more like Andy Warhol’s Empire than Blade Runner.

Take digital wallets like Apple Pay or Android Pay and others. This idea is more than two decades old, back when they were known as “electronic purses”. They didn’t reside on phones as the only things which resided on phones were rotary dials and handsets.

Yet the idea was there: something portable which not only replaced cash but provided other value, whether it was loyalty programs or multiple functions such as train tickets. Australian pilots of these programs by Visa and MasterCard were very successful and went nowhere. So too in Japan, Singapore and many countries in Europe.

The reasons for the slow acceptance were many, varied and relatively minor: some people didn’t see the need to replace cash, many merchants were waiting for the technology to gain wider acceptance, terminal providers struggled with contactless capacity, stakeholders raised privacy and security objections.

Now, more than 20 years later, in Australia at least, mobile wallets are gaining genuine traction. This bank, ANZ, has just passed a year since launching Apple Pay and also offers Android Pay and a proprietary ANZ Mobile Pay wallet.

ANZ says it has about 600,000 cards available in digital wallets (the lion’s share being Apple Pay) with nearly 18 million mobile payment transactions made over the past year. The bank says Apple Pay users are highly engaged and transact 2.5 times more than before they added Apple Pay to their phones.

There’s a generational attraction: Apple Pay appeals most to 18 – 36 year olds while grocery, fast food and fuel are the most popular categories. Meanwhile chief executive Shayne Elliott has said the technology has also attracted tens of thousands of new customers to the bank.

But for all the success of mobile wallets in Australia and some regional markets, whether the technology takes off on a global scale depends primarily on global markets – and that means the United States, China and the European Union.

That’s why it is so difficult to predict how even technologies with proven utility will fare.

Payment analysts note determining markets actually fall into development not geographic categories - developed economies or emerging markets. They are totally different due to the percentage of the population unbanked, the penetration of smart phones and the size of the banking sector compared with substitute payment entities like telcos.

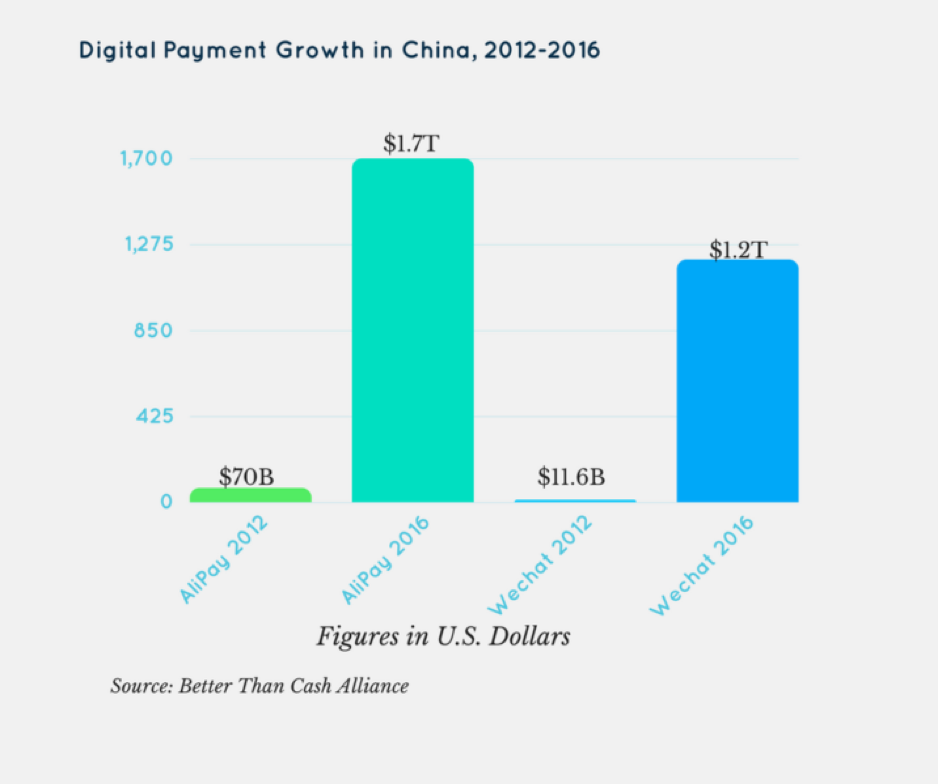

Take China. According iResearch, China is the largest mobile payments market in the world with transactions tripling to 38 trillion yuan. But the two companies battling for control are not banks, device manufacturers or telcos, they are the internet conglomerates Alibaba and Tencent.

Alibaba’s Alipay is the market leader via its e-commerce sites Taobao and T-Mall with Tencent's WeChat Pay growing due to the near 800 million daily active users on its messaging and social media app.

While originally online, these technologies are migrating to the physical world. The Chinese are already huge mobile wallet users – but the technology most commonly is a phone app scanning a QR code linking the merchant with the internet company.

Using low cost point-of-sale technologies and phone-based systems such as QR codes is lower cost and easier to roll out. These strategies are being used not just in China but also the Philippines, Kenya, Mexico and South Africa.

According to a report in The Australian Financial Review, WeChat Pay accounted for 24 per cent of all transactions by value during the week ending March 31, having been added as a payments options just six months earlier. Alipay accounted for 72 per cent of transactions with the state-backed UnionPay, which holds a monopoly on credit card payments in China, making up the remainder over the same period.

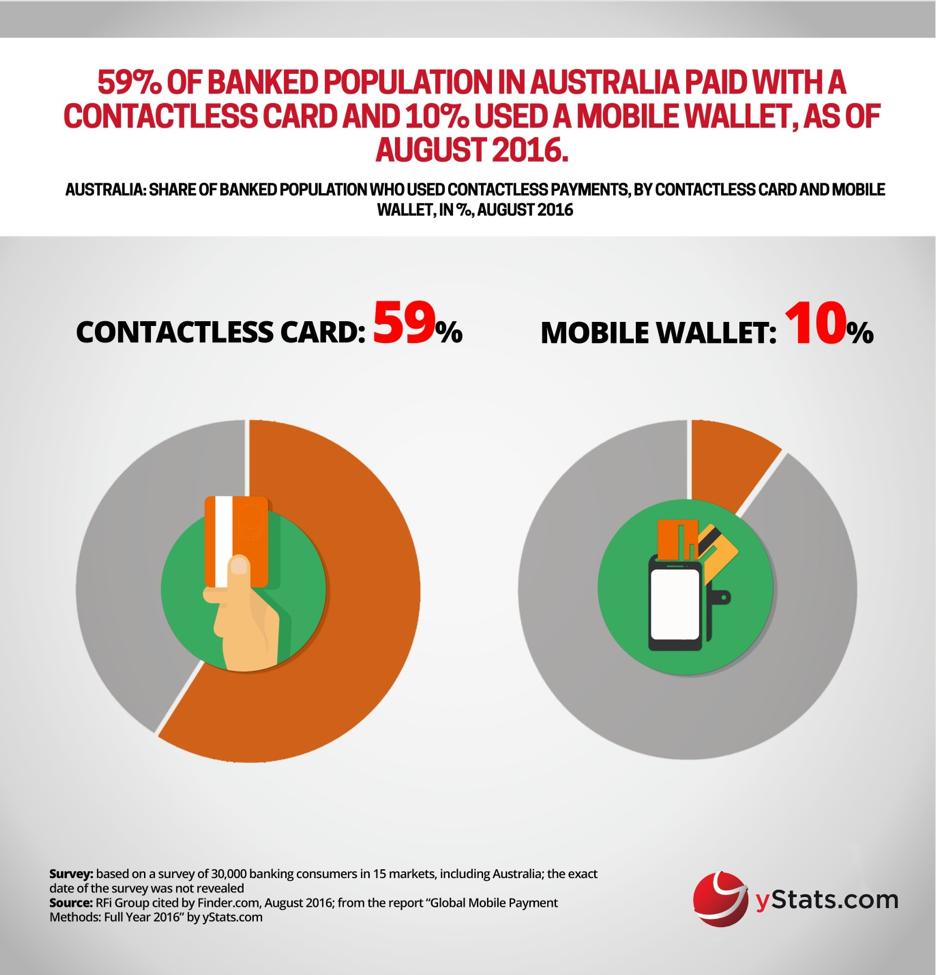

Meanwhile, in Australia the runaway success of contactless payments via so-called “tap’n’go” is a double edged sword: mobile wallets utilise the same contactless technology but the success of cards in this realm means it is harder to have consumers switch.

Some recent research by an industry consultant found 11 per cent of Australian consumers were familiar with Apple Pay and Samsung Pay but 40 per cent were still not aware of mobile payments at all. However 85 per cent had used a contactless card.

Obviously mobile wallets are still relatively new so greater awareness would be expected to aid take-up but the question is to what extent.

{CF_IMAGE}

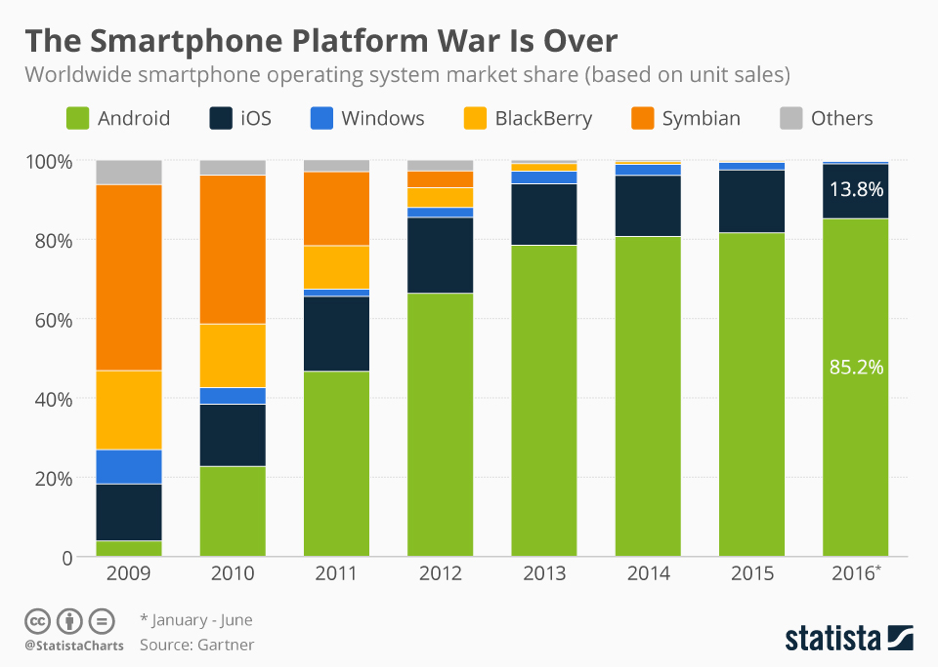

The battle between wallets is also a proxy battle between device manufacturers. Android is currently the world’s dominant mobile platform but the competition varies from market to market. For example, in the US and Australia, Apple has close to 40 per cent share but in China its share is around 15 per cent and elsewhere in Asia it is put at just 4 per cent.

{CF_IMAGE}

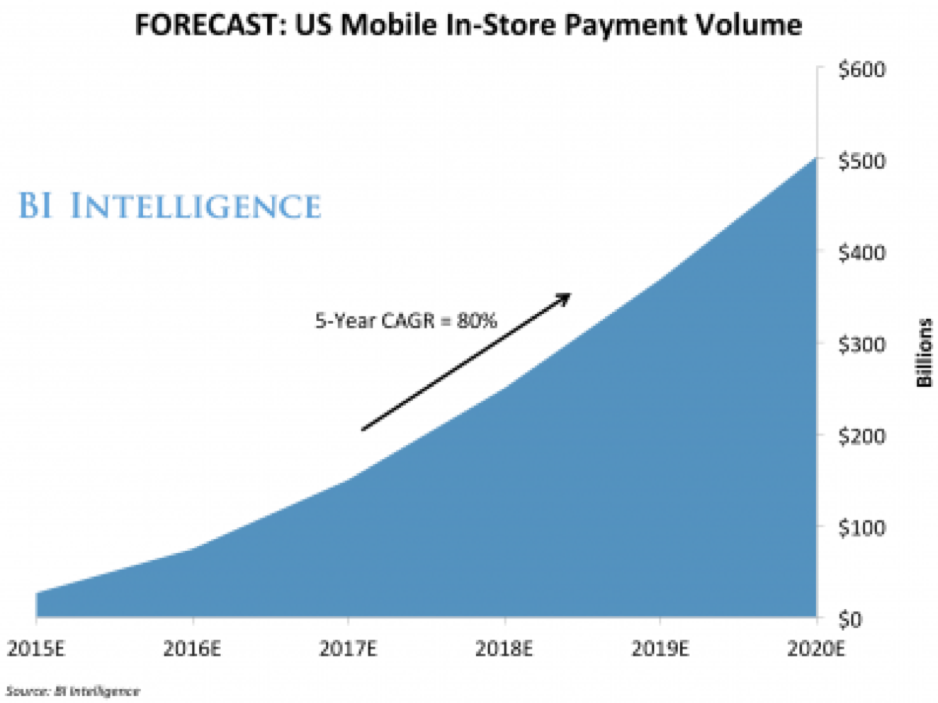

Then there is the practical challenge of infrastructure. The US has deep mobile phone penetration and the world’s largest number of credit cards at around 700 million – and hence there’s a prima facie case for a huge mobile wallet market storing those cards on smart phones.

The reality is though the US payments market is relative primitive – many terminals are not even smart card compatible so can’t even do a contactless transaction. Transactions are often still signature based, not even PIN-based.

Mobile sales in the US are forecast to reach $US600 billion by 2020 – pretty impressive until you look at total US cards sales (Credit/Debit and other cards) which were $US6.7 Trillion in 2014 – and projected to grow to $US9.4 Trillion in 2018. So by 2018 in-store mobile payments in the US will only reach 2.6 per cent of total card spend at current the rate.

{CF_IMAGE}

{CF_IMAGE}

This doesn’t mean mobile wallets will not become a significant part of the payments landscape. They are more secure, convenient, offer a range of added value - but history shows technology and opportunity are not the whole story.

So too with AI. The potential – and the risks – are real. The potential opportunities, even if they don’t include micro brewing and flat breads, defy the imagination. But we are still some way off the singularity of Sci-fi movies.

Andrew Cornell is Managing Editor of BlueNotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

-

-

Share

anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/technology-innovation/digital,anzcomau:Bluenotes/technology-innovation/disruption,anzcomau:Bluenotes/technology-innovation/tech

Beyond Good and Evil: AI and market forces

2017-05-10

/content/dam/anzcomau/bluenotes/images/articles/2017/May/cyberforce_thumb.jpg

EDITOR'S PICKS

-

Work Club founder and CEO Soren Trampedach discusses the future of work – and it is essentially evolve or die.

9 May 2017 -

Fresh from San Fran, here are six key take-outs from a region known for incubating innovation.

8 May 2017 -

Since the financial crisis in 2008 the speed of regulatory change has accelerated rapidly, consuming an increasing amount of time and resources. In 2014, the top six banks in the US spent over $US70 billion on emerging regulation.

5 May 2017