-

Judging by the headlines of McKinsey & Co’s latest Asia-Pacific Banking Review, it’s becoming less attractive to bank in the region as an era when this part of the world was the most fertile for growth loses vigour.

" If Asia’s first transformational catch up story was industrial, its next will be financial - even if the precise path is unpredictable and rocky."

Andrew Cornell, Managing Editor BlueNotes“Our annual report, Weathering the storm: Asia–Pacific Banking Review 2016, finds that the momentum from this golden decade is already fading,” the consultancy says.

“Margins and returns on equity are shrinking - for instance, the Asia-Pacific banking industry’s return on equity (ROE) slipped to 14 per cent in 2014, from 15 per cent a year earlier. The region and its financial industry seem to be settling into a new era of slower growth and greater challenges in generating economic profit.”

Yet McKinsey properly and promptly adds such is the diversity of the region, in culture, economic cycles and stages of development, the macro picture doesn’t always capture the micro stories.

Nevertheless, it posits three headline challenges – slowing macroeconomic growth; disruptive attackers from outside the financial services sector; and weakening balance sheets – which mean Asia won’t repeat the last decade when it delivered 46 per cent of global banking’s $US1.1 trillion profits in 201 compared with just 28 per cent in 2005 (thanks mainly to Chinese growth).

There’s obviously evidence to support this aggregate view. (Even China’s most recent higher than expected growth numbers - driven as they were by credit growth and a reversion to infrastructure spending - may not be sustainable according to ANZ Research.)

Meanwhile, there is little dispute debt is rising in China and elsewhere in the region with consequent risk implications.

So what might be some of the offsetting attractions in the region?

DEEPENING MARKETS

McKinsey itself, in a separate report, points to the positive impact of deepening capital markets in Asia.

“Deeper capital markets in emerging Asia could free up an additional $US800 billion every year in funding, mostly for midsized to large corporations and infrastructure, accelerating economic growth and potentially lifting millions out of poverty,” the consultancy said.

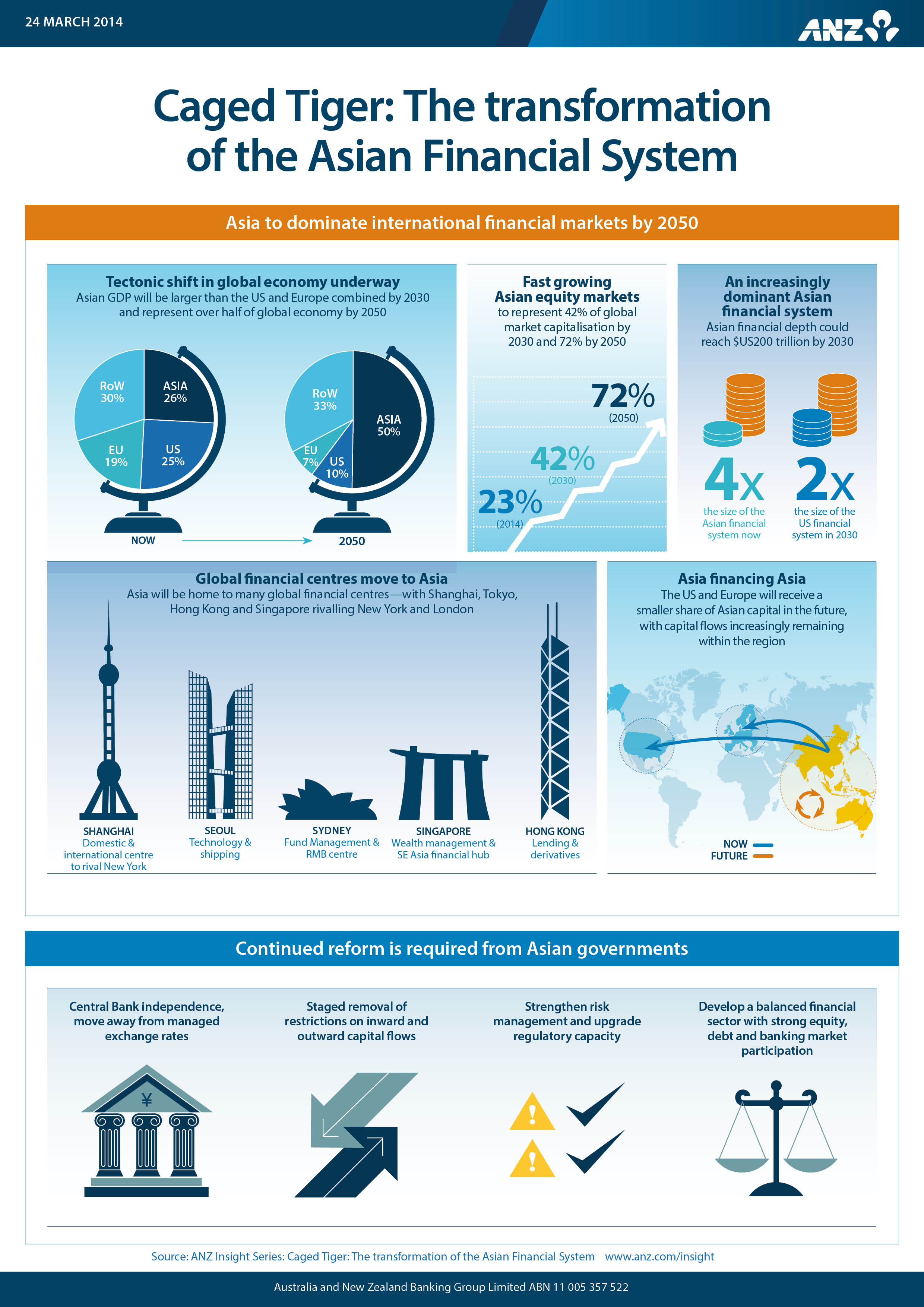

This is precisely the point made in ANZ’s far reaching analysis of the transformation of the Asian financial system, Caged Tiger.

In that report, ANZ estimates the region’s financial system could be as large as $US200 trillion by 2030. This would make it about four times the current size of the Asian financial system and more than twice as big as we project the US financial system to be in 2030.

The secular momentum of this transformation is profound and over the longer term will support not just banks but a huge variety of participants in financial services.

“The area with the most significant growth potential is the debt markets,” Caged Tiger forecasts.

“Asia currently has a relatively small bond market but a viable alternative to bank finance needs to be developed. ANZ projects that the Asian domestic debt (excluding Japan) could be worth around $US80 trillion by 2030 (with China accounting for over half). Asian equity markets could represent over 40 per cent of global market capitalisation by 2030.”

{CF_IMAGE}

If Asia’s first transformational catch up story was industrial, its next will be financial - even if the precise path is unpredictable and rocky.

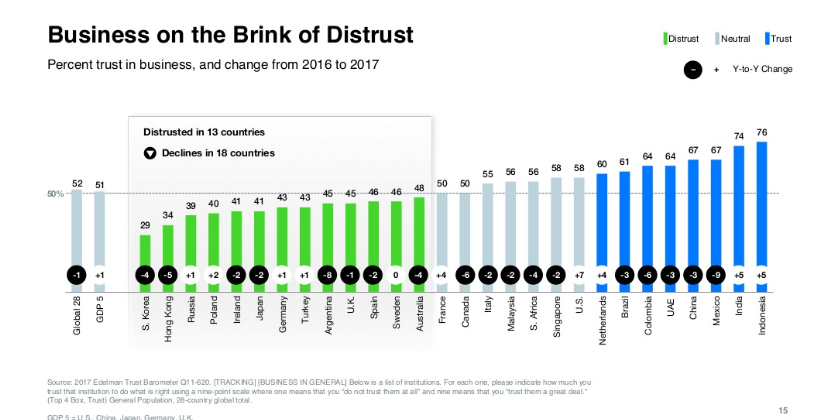

Asia has another, less-tangible but equally profound advantage over western markets: the trust essential to financial services remains relatively more robust in Asia than the west.

That means the pressures of extra regulation, policy intervention and customer rejection are less intense.

According to the most widely quoted survey of popular attitudes to business, the Edelman Trust Barometer, the – again relatively – more positive mood was in large Asian countries. For example, of the eight countries were business was still ‘trusted’, Indonesia showed the highest level of trust followed by India with China fourth.

{CF_IMAGE}

There is a clear consensus falling trust raises operating costs – companies have to do more to convince customers to deal with them, they have to spend more time defending their actions to politicians, they incur more regulatory intrusion. To that extent, higher levels of trust translates to a competitive advantage.

LEVERAGED PLAYS

It is true financial services and banking in particular are leveraged plays on economic growth so any economic slowdown in Asia is likely to impede profits.

Trade, in particular, is an issue because so many Asian economies are trade dependent. Hence the current anti-globalisation and even mercantilist agendas gaining ground in the US, the UK and Europe in particular are a concern.

However to date the evidence does not show a sharp retraction in trade. According to the Institute of International Finance’s monthly growth and financing data, the IIF Emerging Market Growth Tracker advanced for the fifth consecutive month in March, marginally adding to a five-year high.

The major driver was emerging Asia. The IIF also noted ongoing portfolio inflows: such inflows to EMs rose to $US29.8 billion in March.

“All four EM regions saw positive inflows for the second consecutive month,” the IIF said. “China saw net capital inflows in February for the first time since 2014, while net capital inflows to EM ex-China reached a four month high.”

The trade story though is mixed. On a recent run through Asia, ANZ head of institutional banking Mark Whelan told the South China Morning Post “there has been a slowdown in trade already (post-President Trump) and you’ve got to take into your thinking that there might be further disruption.”

The challenge – as always with Asia – is the variety and disparity in the region and the time frames involved.

McKinsey was quite negative: “An increasing volume of nonperforming loans is putting added stress on banks, as interest-coverage ratios decline at large companies throughout the region, especially those in China and India,” the report said.

“Our analysis indicates that by 2020, banks in Asia need to raise $US400 billion to $US600 billion in additional capital to cover losses from non-performing loans while maintaining capital-adequacy ratios.”

“Our analysis of 328 banks in the region showed that while 39 per cent posted an economic profit in the period from 2003 to 2006, only 28 per cent did so from 2011 to 2014.”

OPPORTUNITY & THREAT

McKinsey though was clear: this is as much an opportunity for disciplined banks able to innovate as it is a threat to passive incumbents.

The firm noted the keys to success would be focused growth; digital transformation; strong balance sheets; adaptability and a willingness to partner – for example with financial technology start-ups.

On that front, Asia does have promise. Outside of Silicon Valley, Singapore is considered a hot bed of fintechs but it is not alone.

China too is aggressively sponsoring such businesses and its major online firms such as Alibaba and Tencent are highly innovative in core banking sectors like e-commerce and payments with Alipay and WeChat Pay – to the extent the cashless economy in China has penetrated deeper than the US.

Then there is India: in a recent report, venture capital analysts CB Insights noted foreign investors have rushed to capitalise as the country’s GDP continues to grow at a steady clip.

“Looking at Indian fintech specifically, funding to private companies in the sector boomed from about $US175 million in 2014 to a high of $US2 billion in 2015 (buoyed by mega-rounds to Paytm) and then slid to $US530 million in 2016.”

“Still, 2016′s total funding was more than 200 per cent higher than total funding in 2014,” the firm said.

“A host of global corporations and their venture arms have entered the fray, eager to reach India’s mostly unbanked population and profit from the country’s tech-friendly regulatory environment.”

It’s an exciting time to be in Asian financial services – if your heart can take it.

Andrew Cornell is managing editor at BlueNotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

Share

anzcomau:Bluenotes/business-finance,anzcomau:Bluenotes/business-finance/banking

Pressures and promise for banking in APAC

2017-04-20

/content/dam/anzcomau/bluenotes/images/articles/2017/April/inisght5_infographic_preview.png

EDITOR'S PICKS

-

A demand for increased duration, diversification and the rise of Asian liquidity are the biggest factors facing Australia’s capital markets sector as we head into the middle of 2017, according to the co-heads of capital markets at ANZ.

30 March 2017 -

In the Australia-India trading partnership much that glitters is fool’s gold.

20 April 2017 -

ANZ chief executive Shayne Elliott says the bank is seeking a partner and exploring models for its wealth business but insists the industry remains critical to the bank’s customer proposition.

4 April 2017