-

Australians love talking about property – how expensive it is but also how desirable. At the same time as affordability is at cyclical lows and household debt at highs, both major Australian media organisations have launched huge, glossy inserted marketing magazines wallowing in the allure of luxury property.

" Housing is not just a roof over a head, it’s a roof over the economy."

Andrew Cornell, BlueNotes managing editorThey conjure images of one of Marge Simpson’s favourite magazines “Better Homes than Yours”, but if the public is obsessed, politicians too are obsessed by housing.

As are all Australia’s financial regulators, the Reserve Bank, the Australian Prudential Supervision Authority and the Australian Securities and Investments Commission.

Those three, together with the Federal Treasury, form the Council of Financial Regulators, a joint body strengthened during the financial crisis and instrumental in the response. And COFR too has recently concentrated its attention on housing.

Twenty five years ago, Australia’s gross domestic was $A757 billion. Housing lending was $A93 billion – around 12 per cent of GDP. Today, GDP is $A1.67 trillion and housing lending $A1.65 trillion – 98 per cent of GDP.

Meanwhile, the percentage of housing lending attributable to investors has risen from 20 per cent to more than 50 per cent. (Although definitions differ but while the numbers may vary the trend is clear.)

In 1992 Australian mortgages made up 18 per cent of the Australian major bank lending – it is now 54 per cent. Interest only loans – where no principle is paid down and considered the most risk loan type – constitute around 40 per cent of new lending.

Housing matters.

GORDIAN KNOT

But housing is a Gordian knot of complexity and there’s no Alexander the Great to simply untangle it with one swing of a sword.

Politicians want affordable housing for first home buyers and those swinging voters in the mortgage belt. Investors want somewhere to grow their cash when interest rates are historically low. The economy is relying on housing growth as business growth remains limp. And banks need mortgages for earnings growth.

There are multiple levers but no one policy lever or even simple mix addresses all the needs and indeed there are inherent contradictions. For example, the International Monetary Fund recently released research demonstrating the relationship between low interest rates, high house prices and household indebtedness – pre-conditions for a financial system problem.

The RBA explicitly referred to this challenge when announcing no move in its official interest rate on Tuesday: the bank said “by reinforcing strong lending standards, the recently announced supervisory measures should help address the risks associated with high and rising levels of indebtedness”.

In Australia, while raising interest rates may tamp down some property lending and offer investors relatively more attractive alternative investments, higher rates may also choke off broader economic growth – in turn affecting salaries, employment and business investment.

Consider the measures being considered to address affordability and stability: changes to negative gearing; capital gains tax; allowing early access to superannuation for first home buyers; changes to grant systems; prudential measures to reign in investment and higher risk lending.

Last week APRA released another slate of measures intended to cool the property market. On Monday ASIC released its own warning to lending institutions to be aware of their responsible lending obligations at a time when new rates are being introduced into different sectors of the mortgage market.

To help stability, APRA wants to limit growth in the historically more-risky sector of interest-only investing (and also investor lending although historically that has actually been lower risk).

It has done this by telling banks to limit growth directly and also flagging higher capital to be held against categories of loans to offset the greater risk – which in turn should make those loans more expensive and slow growth. Indeed the banks have already begun to move ahead of more direct action and increased the interest rates on investor and interest-only loans.

These moves followed two major speeches by RBA officials flagging action to address the heat in the housing sector.

The make-up of the housing challenge is complex, with multiple moving parts and policy issues, but the scale of the sector demonstrates why what is happening in the mortgage market is more than just a side dish at a Sydney dinner party.

The political and social challenge of housing is not just to reduce its importance to the economy (particularly when there few other sources like a resource investment boom) but to balance competing winners and losers.

CONFLICTING SIGNALS

Consider some of the often conflicting policy signals:

• The government wants higher housing affordability but if the measure to address this is to make lending more expensive for investors, one outcome will be higher margins for banks – not necessarily politically desirable.

• The RBA wants stability in the economy so needs to balance taking heat out of the housing market without too much collateral damage to other sectors. If, for example, household interest payments rise already soft retail spending may fall further.

Greater housing supply is also one way to cool the market but, if there is uncertainty in the market, construction is likely to be held back until there is more certainty.

On the upside, higher interest rates lift yields in other asset classes giving investors more alternatives to rental income which offers returns currently barely higher than bank deposits (and property prices are rising faster than already high rents, further cutting yields).

Differential pricing on investor and interest only loans will expose some categories of borrowers more: the spending power of those on interest only loans will be much lower, perhaps to the extent they have to offload some property; retirees may find they finish their working lives with considerable debt still outstanding, reducing their retirement income.

APRA’s statutory obligation is stability in the financial system but it has limited power to restrict lending by non-bank financial institutions outside its mandate (it has taken some measures via the banks). For the supervisor, bank profitability is actually a good thing – less chance of failure and better protection for depositors.

The RBA is fundamentally concerned with financial stability, as is its mandate. It has been increasingly concerned since first taking action to “lean” against the property market in 2014.

“There was very strong demand for residential housing loans, particularly by investors,” assistant governor Michelle Bullock said in a recent speech.

“Price competition in the mortgage market had intensified and discounts on advertised variable rates were common. There also seemed to be a relaxation in non-price lending terms.

“The share of new loans that were interest only was drifting up and the growth of lending for investment properties was accelerating. Unsurprisingly in this environment, the growth in housing prices was strong, particularly in Melbourne and Sydney.”

SAND IN THE GEARS

Bullock referred to the regulatory response as putting “a bit of sand in the gears”. That sand kicking is just what APRA and ASIC have done again in recent days, demonstrating as she said “the initial effects on credit and some other indicators we use to assess risk may fade over time. We are continuing to monitor their ongoing effects and are prepared to do more if needed”.

But other issues emerge. One is the so-called balloon squeezing affect: squeeze one part of the balloon and it simply expands in another. In this case, non-APRA regulated financiers may simply increase their lending.

While housing is expensive it is not essentially over-priced: someone is willing to buy at these prices. There could be price falls - which demonstrate buyers are no longer prepared to pay those prices.

That could be due to market sentiment, it could be due to increased supply (although that would take time and be quite visible) or it could be due to policy shifts.

If the market is truly overheated, then by definition it should fall or at least stop growing. But what would be the impact on consumer and business confidence of that?

That also raises other complexities. Take the idea of allowing first home buyers to access the superannuation for a house deposit. Ignore for a moment the other, substantive debate over whether compulsory superannuation is the best retirement prophylactic. Using super to give a category of buyers the capacity to pay even more will increase not decrease prices.

Meanwhile, the property ecosystem is not quarantined from the broader economy, as the IMF’s concerns about household indebtedness demonstrate.

Think of some other potential consequences: higher financing costs for investors may actually limit new supply so the cost of renting (already another issue) may rise; the forced switch from paying interest only to interest and principle or paying higher interest only will impact the cash flow of about a third of mortgage holders; the flow-on impact to the property construction and servicing industry; a revenue hit for Fairfax and News Ltd (the publishers of the glossy property marketing magazines).

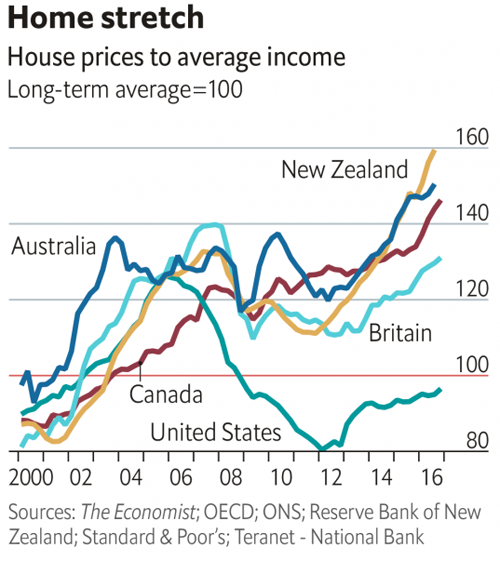

Residential property and its associated debt is the great policy challenge of the day. Prices continue to surge - CoreLogic capital city house price data for March showed a further acceleration, with house prices up 12.9 per cent year-on-year in March compared with 11.7 per cent year-on-year in February.

According to ANZ Research, this is the strongest annual price growth since the first half of 2010.

“In seasonally adjusted terms, we estimate that capital city house prices rose 0.7 per cent month-on-month in March – compared with 1.4 per cent in February,” ANZ said in a report.

“While the pace of monthly house price growth has slowed a little, we think it too early to conclude annual house price inflation has peaked. Both auction clearance rates and the housing credit impulse suggest the peak is still to be seen.”

{CF_IMAGE}

MASSIVE SCRUTINY

Nor, although it is early in the rising rate cycle, have borrowers responded as the might be expected to by increasing how much of their borrowing they fix as opposed to allow to vary.

For example, Mortgage Choice saw demand for fixed rate home loans dip, not rise, accounting for just over 20 per cent of all loans written throughout March compared with 22 per cent in February.

With all this uncertainty, the massive scrutiny of the property market – including in the mainstream media – is a welcome recognition of its huge impact on both the economy and economic policy.

The ‘chase for yield’ dynamic is one which is often over-looked but as the investment writer Chris Joye has argued, this is another source of growing risk in the economy.

“Rational investors are forced, through central bankers’ “financial repression”—or artificially low cash rates—to chase risks they would never ordinarily assume to eke out an income that satisfies their retirement needs,” he wrote.

“This is one of the key drivers of demand for investment properties: incredibly low gross rental yields of 4 per cent look enticing when at-call deposit rates are around half that level.“

“Since 1991 the RBA's cash rate has, on average, furnished savers with a real return above inflation of about 2.5 per cent annually. This made deposits and bonds viable investments with low risk. Today that is no longer true for many retirees.”

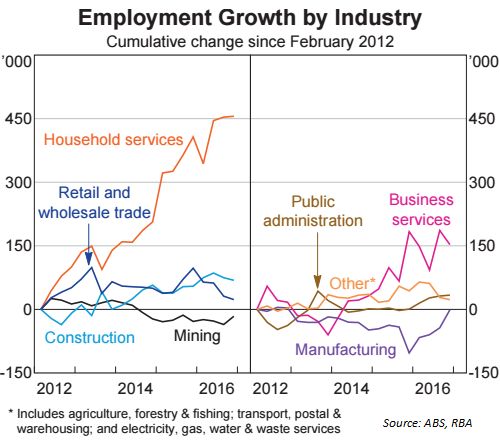

According to the Australian Bureau of Statistics, total dwellings investment increased 9.8 per cent and contributed 0.5 percentage points to GDP growth in 2015-16. This was the third consecutive year of growth in total dwelling investment.

“The increase in 2015-16 was driven by investment in new and used dwellings (up 13.1 per cent),” the ABS said.

Residential property construction and wealth effects are also inextricably linked to employment, a key part of both the growth in employment in household services and construction.

Housing is not just a roof over a head, it’s a roof over the economy.

Andrew Cornell is managing editor at BlueNotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/global-economy/housing

Housing: boom or doom?

2017-04-05

/content/dam/anzcomau/bluenotes/images/articles/2017/April/cornellproperty_thumb.jpg

EDITOR'S PICKS

-

The world is preoccupied with rating the city. From the towering skyscrapers of New York to Tokyo’s colourful neon and Melbourne's amiable public spaces, it seems there’s a way to grade every aspect of the modern metropolis.

6 March 2017 -

The challenge of companies and individuals shuffling income and assets between jurisdictions - a major issue in the ASEAN region - has come to the fore in both Australia and Indonesia.

27 March 2017 -

A demand for increased duration, diversification and the rise of Asian liquidity are the biggest factors facing Australia’s capital markets sector as we head into the middle of 2017, according to the co-heads of capital markets at ANZ.

29 March 2017