-

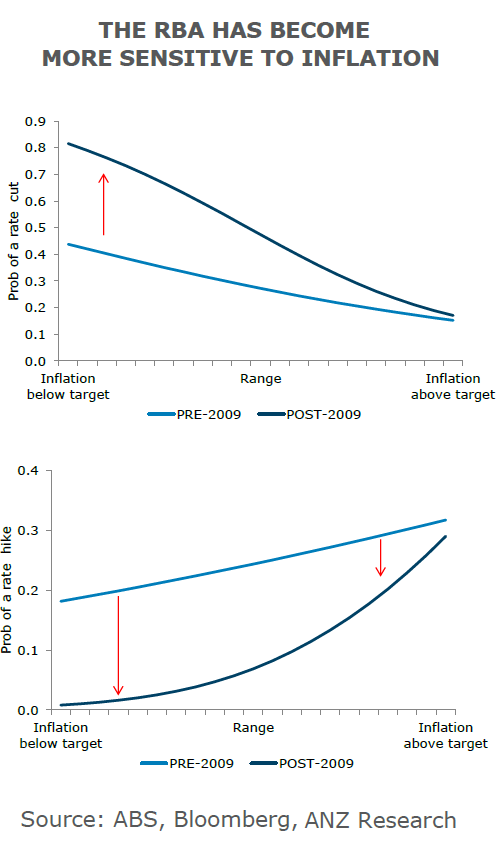

The Reserve Bank of Australia has become increasingly sensitive to below-target inflation readings, new research from ANZ shows, while at the same time less sensitive to shifts in the unemployment rate – historically the biggest factor in interest-rate decisions.

This has a number of implications, among them a model which could effectively predict movements in the cash rate.

"In the near-term there is a greater likelihood of a [cash rate] cut than a hike."

David Plank & Giulia Lavinia Specchia, Head of Australian Economics & Economist, ANZPreviously, a relatively simple way for the RBA to characterise decisions to change the cash rate has been changes in the unemployment rate. Certainly this appears to have captured the major shifts in the cash rate setting over time.

{CF_IMAGE}

Still, there have been times when the movement in the unemployment and the cash rates were not necessarily consistent and this has become more common in recent years.

It seems reasonable to suppose, among other things, the RBA’s reaction to shifts in unemployment may be impacted by the overall inflation backdrop.

In times of relatively high inflation the RBA may be less sensitive to a rising unemployment rate than otherwise and vice versa when the inflation rate is low.

This seems quite reasonable to us. The risk of embedding excessively low inflation outcomes has motivated aggressive policy responses by many central banks in the post-GFC period.

We think the policy implication is the RBA needs to see clear evidence core inflation is trending sustainably higher before it even considers raising interest rates.

A premature tightening of monetary policy may result in even lower inflation outcomes that will have negative feedback implications for wages, among other things.

DRIVE CHANGE

The intent of the model is not to determine what the RBA cash rate should be but rather to consider what seems to drive changes and whether or not the influence of the various drivers has changed over time.

Still, it can be adapted to determine a point estimate for the cash rate. Based on ANZ’s forecasts for inflation and unemployment, the model suggests a rise in the cash rate at the end of 2018.

As things currently stand, the model forecasts a 75 per cent chance of the RBA being on hold over the coming 12 months (compared with an historic average of 62 per cent), with 15 per cent probability of a cut and 10 per cent probability of a hike.

This suggests risks for the cash rate continue to be skewed to the downside. In the near-term there is a greater likelihood of a cut than a hike.

Further evolution of the RBA’s reaction function seems more likely than not, though always within the constraints imposed by the bank’s mandated objectives. This needs to be kept in mind when forecasting the likely policy path for the RBA.

David Plank is head of Australian economics & Giulia Lavinia Specchia is an economist at ANZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/global-economy/economics,anzcomau:Bluenotes/global-economy/regulation

Inflation, not employment, now guides RBA on rates

2017-03-29

/content/dam/anzcomau/bluenotes/images/articles/2017/Thumbs_Jan_Mar/Inflation, not employment, now guides RBA on rates_Thumb.png

EDITOR'S PICKS

-

Unfortunately both in general and for female students, economics is not exactly popular in Australia.

20 March 2017 -

The US Federal Reserve has raised interest rates as expected but all eyes are on the future as a slightly disappointed market reflects on what happens next.

16 March 2017 -

With all the excitement accompanying Hobart’s unveiling of MONA back in 2012, not even the most optimistic among us could’ve foreseen how transformational a privately owned modern art museum would be for the tourism fortunes of the capital or for Tasmania as a whole.

23 March 2017