-

Looking back over the last two decades of Australian banking, one of the most profound disruptions was the entrance of mortgage originators and brokers to the residential mortgage market.

In a matter of years, market shares of the new competitors had grown to near 20 per cent and margins on mortgages had dropped more than 2 percentage points.

"Many argue the digital banking will be disruptive… to brokers. I’m not in this camp."

Cosi De Angelis, GM Commercial Origination, Australia, ANZToday many argue the emergence of digital banking will be similarly disruptive but this time it is the brokers who will be under pressure. I’m not in this camp but there is no doubt change is coming.

One sector in particular changing before our eyes is the broker model for commercial lending – long forecast to be just as disruptive as in the mortgage market.

DIGITAL

But first digital. Are both the traditional bank-owned and broker models of customer relationships vulnerable to digital disintermediation?

Fundamentally, I believe a customer involved in a transaction is looking for advice and a conversation with someone - not something -they trust. A face-to-face conversation will always offer more than a digital one.

At ANZ, when we look at our relationship strength indicators, what comes across clearly is how the strength of the human relationship is central to engagement and advocacy (as measured by metrics such as the Net Promotor Score.)

For example, one strong advocate noted her relationship manager “knows my business and gets back to me within 24hrs if I have any queries and acts on my concerns.”

“I have dealt with other business banking managers and they have been fairly poor,” the responder said.

Conversely, when scores are poor, a common factor is a lack of human contact and a sense of being treated as part of a program.

FROM HOMES TO BUSINESS

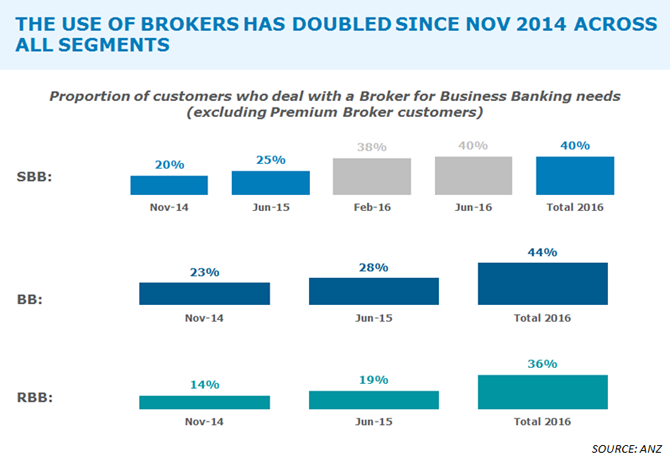

While upheaval in the residential mortgage market has settled down and brokers are now a solid part of the market, the question remains of why the same rapid shift hasn’t occurred in the commercial broking or third party market.

It has grown - just not as fast as in residential mortgages.But I think what we are now seeing is the commercial 3rd Party market in Australia growing with real momentum.

In an economic climate which has seen competition increase, changing demographics, more choices for customers, record low interest rates and banks looking for a greater return on equity and a variable cost service delivery models, third party distribution via brokers makes sense.

All major loan aggregators believe the next two to three years will continue to see the 3rd Party Commercial & Asset Finance market grow at well over 20 per cent each year. In a recent survey by Momentum Intelligence, 85.7 per cent of brokers not currently writing commercial business said that they intended to enter into the market and 80 per cent of brokers who currently offered commercial loans expect volumes to increase.

With system growth in commercial banking forecast to be flat in the midterm, brokers offer incumbent institutions a lower-cost model and the opportunity to grow market share efficiently.

Increased competition has provided more choice to business clients. Many are SMEs and are busy enough running and managing their business without having to undertake the research on the best solutions for their business. Good brokers take on this task.

{CF_IMAGE}

Most traditional lenders in Australia are now operating in the Commercial 3rd Party market, most entering over the last 10 years.

COST STRUCTURE

With a traditional model for servicing small business, physical branches, staff and even technology were fixed costs for banks. Taking on brokers as third party agents allows those costs to vary with demand.

But the decision is not all about margin. Obviously service remains critical and while fixed costs come down, brokers are paid via commissions which must be managed (and, as we have seen in public inquiries, must be properly structured.)

However the research shows good broker relationships deliver superior customer satisfaction (EY MFAA report May 2015), commercial clients who have used a broker generally have higher levels of satisfaction with their bank and greater levels of advocacy.

This equates to a significantly lower attrition rate compared with owned channels, again adding to revenue and reducing the costs of customer churn.

Furthermore, and similarly to the mortgage book, as far as ANZ goes, we have not witnessed any heightened risk metric differentials to our broader first-party channels.

BROKER AND BANKER

I often hear people talk about friction in the residential mortgage channel between first and third party. Commercial is a different proposition.

All brokers need good bankers to service their greatest asset....their customer. For a broker with a long-term client relationship there is no incentive to refer a client to a banker they do not trust will service their client professionally and effectively.

Both parties require trust. The two cannot function and thrive without a partnership built on trust. In our and external research there is clear evidence brokers have become the trusted advisor.

Indeed – and again similarly to what happened in the mortgage market – many brokers were formerly relationship managers in banks.

Some of the findings from our research are:

- Brokers recommend bankers based on prior experience;

- Relationships are increasingly broker only, who then interacts with the banker – a challenge for banks as customer engagement is with the broker;

- Some customers who have begun using brokers due to negative experiences with banks;

- Customers are receiving more frequent and personal contact from their brokers; and

- Customers who used to deal with a bank directly now deal with the same bank but through a broker due to better service and deals.

SMALL BUSINESS, BIG OPPORTUNITY

Around a third of all mortgages are now broker originated, according to the Reserve Bank, although some industry data put the figure significantly higher. ANZ data shows 30 per cent of all mortgages written today are for self-employed applicants. It seems clear then the opportunity for brokers to have a commercial needs conversation with their clients is significant.

Most in the industry believe SME lending will follow the path of mortgages when it comes to 3rd Party flow. With 2,000,000 small businesses in Australia and a growth rate of over 300,000 new SME's each year, the size of the opportunity continues to grow.

HUMAN INTERACTION

Digital disruption will undoubtedly impact the emerging model of broker-based distribution. But what I don’t see changing is the preference for genuine interaction rather than just transactions.

For example, the focus on lending, on debt, is flawed. Disruptors entering the market today, rightly, are focusing on the whole relationship, all the transactions and needs, not just borrowing.

This makes sense for brokers too. The evidence from banking is when an institution holds a greater share of a customer’s financial wallet attrition levels are lower, the customer is more engaged and future funding needs are better understood and dealt with more efficiently.

REGULATION

With the rapid growth in the third Party market it is no wonder the regulators have been keen to understand more about the industry.

We welcome the responsible lending review moving into the commercial space. I believe it is an opportunity to demonstrate the value brokers add to customer relationships and further assist the industry to dispel myths about how brokers operate.

Customers are after a valuable, longer term relationships. The regulatory interest is in ensuring that’s what customers achieve, through transparency, appropriate remuneration and customer protections.

Cosi De Angelis is GM Commercial Origination, Australia at ANZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/technology-innovation/fintech,anzcomau:Bluenotes/technology-innovation/innovation,anzcomau:Bluenotes/technology-innovation/disruption,anzcomau:Bluenotes/technology-innovation/digital

Is the broker of the future a machine?

2016-11-30

/content/dam/anzcomau/bluenotes/images/articles/2016/November/deangelisbrokers_thumb.jpg

EDITOR'S PICKS

-

Banking will look radically different in 10 years’ time, probably even five. It will be digital – even though that means many things to different people. And financial technology start-ups – fintechs – will be behind much of the transformation.

2 November 2016 -

It’s now nine years since ‘fintech’, the buzz term for financial technology start-ups, entered the lexicon and threatened to upend banking as we know it. It hasn’t yet. But will it?

25 November 2016 -

Senior system analysts Sue Nicholas and Karen Oakley have racked up eight decades of experience in bank technology. They have seen it all before.

22 November 2016