-

Someone asked me the other day whether millennial customers are driving ANZ’s new digital product design.

My answer was no.

"Companies can do everything under the sun to make digital products easy to use but it’s pointless if customers can’t … access them in the first place."

Liz Maguire, Head of Digital & Transformation, ANZ NZLet me explain why. And why this is a bigger story than just ANZ.

I recently attended the annual G-20Y Summit in Switzerland, at which 150 corporate leaders came together to discuss recommendations on a range of economic and geopolitical issues – including digital innovation.

It was a fascinating session not only because the recommendations are designed to assist G20 leaders but also because the Y in G-20Y stands for ‘Youth’. My daughters found that hilarious.

It was here we were discussing millennials – people born after 1980 - who tend to be more engaged with technology. Of course, there’s no shortage of research examining digital behaviour.

Millennials make up about a third of our workforce, spend about a third more time online on their smartphones and interact with organisations online more than the rest of the population combined.

We even know they are twice as likely to be online in the bathroom, a fact which may either shock you or force you to feign shock to maintain professional credibility.

Either way the plethora of research demonstrates millennials are an important and growing part of the digital consumer base.

But when someone asked me if ANZ design banking products for millennials, it was an emphatic no.

THEN WHO?

ANZ designs products for all customers – but particularly, we design them for the least digitally-able customers in the market. I think it’s a very important philosophy.

If an 88-year-old great grandmother can use a digital banking app to transfer money to her friend for the bridge tournament they’ve entered – just hypothetically speaking – then I know it’s a well-designed product.

Of course, I’m not deliberately being ageist, and of course age is not the only reason people struggle to use digital technology. And, in fact, I have talked to an 88-year-old ANZ goMoney whiz but I’m not sure if she was a bridge player. She may have been more into poker for all I know.

The point is digital products and services must be easy to use for customers of all ages and levels of digital experience. For any successful digital product, two simple boxes need to be ticked above all others.

Firstly, is it better than what already exists? The fact it uses some new whizz bang technology just isn’t enough – it has to improve the way we do things.

Secondly, do all customers have the ability to use it if they choose? That’s the responsibility of the provider. No matter how intuitive a provider feels it is, it’s up to them to show customers not only how use it but understand why they would benefit it from using it in the first place.

This process of education encompasses everything from product design and marketing to how well staff in branches or on the phone or at any other distribution point know the product.

Of course this is only one aspect of digital inclusion. Companies can do everything under the sun to make digital products and services easy to use but it’s pointless if customers can’t afford the digital connectivity to access them in the first place. And that’s a much deeper and trickier social issue than good product design.

BARRIERS

According to AUT’s ‘World Internet Project’ report released earlier this year, along with age, household income is the biggest barrier to internet usage. Banking aside, the implications this has on the education of the youngest generation is immense.

As a digital banking executive I find this tough. But as a mum I find it gut wrenching. Most schools are connected to the internet and their pupils have access to great devices. But tens of thousands of New Zealand households with school-age kids are getting left behind because they have no digital connectivity once they get home. That’s an issue for us all.

The recommendation of G-20Y Summit was to establish a more ambitious global target of 90 per cent coverage for mobile and home broadband access, compared with the current projected level of 71 per cent.

At the moment the New Zealand Government is investing in two major internet initiatives - the Ultra-Fast Broadband Initiative (UFB) and the Rural Broadband Initiative (RBI).

Both are aimed at delivering better, faster internet and both are ambitious, necessary and impressively on track. The government is even installing free residential UFB connections until the end of 2019 so the price of the connection is not an issue.

However, there will always be some families who cannot afford the ongoing price of the data. There are some positive steps happening for that group though.

For example, Spark recently announced, it would provide thousands of free modems and subsidised broadband in low income homes through its Spark Foundation Charity. There are many examples of schools, community groups and local government organisations working together to help low income families get online.

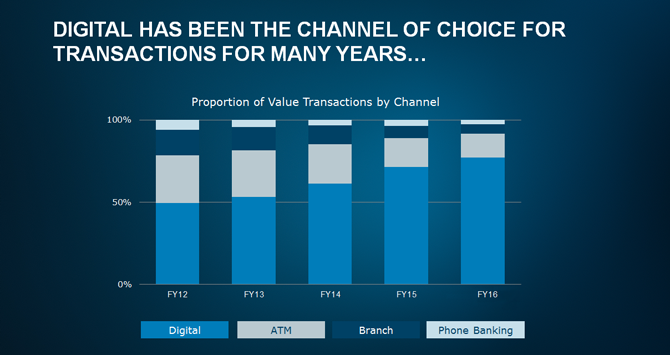

From a banking perspective, the functionality of online banking tools is leading to the evolution of the branch. Increasingly people are doing simple transactions online and using branches for significant interactions like signing up to a mortgage for the first time.

Nearly 80 per cent of ANZ New Zealand’s simple transactions (for example, transferring, withdrawing and depositing funds) are now completed using digital channels, as you can see in the chart below.

{CF_IMAGE}

Additionally, more than 20 per cent of new product requests come through digital channels, almost double the same period last year.

If people are unable to get the digital connectivity to bank online, they are unfortunately excluded from these channels.

Businesses can make digital products easy to use and provide all the support under the sun to help but they can’t solve the issue for everyone, as much as they would like. I find that tough.

POCKETS

Banking isn’t the only industry at risk of excluding pockets of the community. The move towards eServices is the norm rather than the exception in healthcare, transportation and many government departments.

I don’t know what the exact solution is but the price of data seems to be a sticky point – some may say an unfortunate commercial side effect of a small population surrounded by a big sea.

However, I think providing as many free and secure community Wi-Fi zones as possible would be a great start.

What I do know is digital inclusion – in the technical capability sense – sits squarely with those who make the products. But digital inclusion – in the connectivity sense - needs an integrated approach from many groups.

It needs government to keep taking the leadership position and it needs councils, schools, at-risk minority group representatives and businesses to get together, get on the same page and make it happen.

Liz Maguire is Head of Digital & Transformation, ANZ NZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/technology-innovation/innovation,anzcomau:Bluenotes/technology-innovation/fintech

Digital inclusion - age, a new stage and getting on the same page

2016-11-22

/content/dam/anzcomau/bluenotes/images/articles/2016/November/maguiredig_thumb.png

EDITOR'S PICKS

-

Banking will look radically different in 10 years’ time, probably even five. It will be digital – even though that means many things to different people. And financial technology start-ups – fintechs – will be behind much of the transformation.

2 November 2016 -

The only way for banks to survive in the new world of fintech is by embracing the disruption all around them, incorporating that disruption into how they operate.

21 November 2016 -

Senior system analysts Sue Nicholas and Karen Oakley have racked up eight decades of experience in bank technology. They have seen it all before.

22 November 2016