-

Singaporeans are avid property investors, both individually and at an institutional level, within Singapore and globally. They have a shrewd eye for returns and Australia is a major focus, as indeed it is for other Asian and global investors.

Singapore and Australia have long standing economic and social linkages which are likely to get stronger over the years. Australia was the first country to establish diplomatic relations with Singapore post its independence in August 1965.

"When it comes to Australian property Singapore punches far above its weight."

Rohit Mohindra, Head of Commercial Real Estate, Institutional Banking, ANZ SingaporeBilateral trade with Singapore totals $A20 billion a year and Singapore was Australia's fifth-largest trading partner in 2014, with direct investment reaching $A43.5 billion in 2014.

About 50,000 Singaporeans live, work or study in Australia and 20,000 Australians do so in Singapore. About 100,000 Singaporeans are alumni of Australian universities. Last year alone 400,000 Singaporeans visited Australia while 1,000,000 Australians visited Singapore.

The relationship between the two nations is strong, amplifying the Singaporean appetite for property.

ABOVE ITS WEIGHT

When it comes to Australian property Singapore punches far above its weight. Although China is traditionally seen as the biggest buyer of Australian property from Asia, Singapore is fast catching up.

Indeed, in the five quarters to the end of Q2 2016, total commercial real estate investment into Australia was $US14.6 billion and Singapore had the largest share at 27 per cent, compared to China at 24 per cent.

At least 12 of Singapore’s 30 plus listed real estate investment trusts have significant assets in Australia across the office, hospitality and industrial sectors.

Singapore’s market lead is remarkable given that Singapore is only 3 per cent of China in terms of GDP (Singapore $298b. China $9.24t), with a small population of 5.2 millon people (or 3.2 million citizens) relative to China’s 1.36 billion. Australia is more than 10,000 times the size of Singapore.

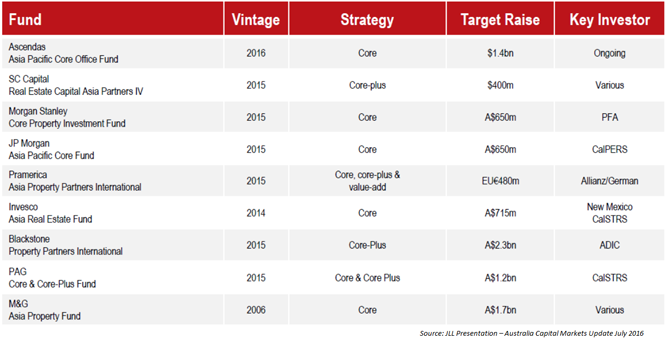

Singapore’s Ascendas group paid around $A1 billion for GIC’s Australian logistics portfolio, the second largest industrial property transaction in Australian history. This was further bolstered by a string of transactions by Singapore sponsors as captured below.

CAPITAL FOR ASIA-AUSTRALIA

Foreign investment in Australian real estate is concentrated in three key states: NSW (around 40 per cent), Queensland (around 15 per cent) and Victoria (around 15 per cent). The top three sources of foreign capital are China, United States, and Singapore.

{CF_IMAGE}

WHY AUSTRALIA?

Australian CBD office space represents just 1 per cent of global office space but for such a small market it is remarkably popular with investors. According to Colliers International 2016 Global Investor Outlook Survey, Australia Ranked second in target countries for investment whilst Sydney and Melbourne were ranked the second and third most popular destinations in the Asia Pacific.

The latest ANZ Property Council Survey reaffirmed the outlook for commercial property being more positive than the residential sector.

Foreign buyers have shown keen interest accounting for 84 per cent and 75 per cent of all hotels asset purchases in Sydney and Melbourne in 2016. Similarly in the commercial office space the foreign buyer share was 56 per cent and 40 per cent.

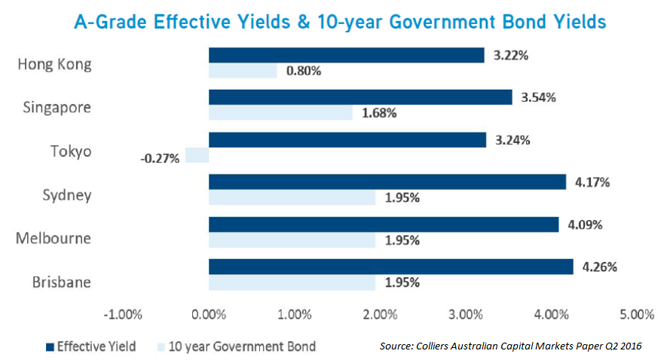

A key reason for the interest is post-GFC, Australia had significantly higher cash rates than most of the region, while cap rates (ratio of net operating income to property asset value) remain relatively richer than comparable overseas assets.

{CF_IMAGE}

Another reason is leases for commercial property in Australia tend to be longer, with rollover options and indexation/escalation provisions, increasing their attractiveness against shorter options in Singapore and Asia in general.

While currency values are a challenge to forecast, the depreciation of the Australian dollar over the past two years has made prime Australian assets, previously considered expensive from a buyer’s perspective, attractive or reasonable.

ARA Group Chief Investment Officer Moses Song says Australia remains an important market for investors in the sector.

“Australia is a strategic market for ARA Group with $S30 billion in assets under management across Asia,” he said. “We hope to build on our recent success in acquiring high quality properties across the country with a view to growing local AUM to several billion dollars over the next 18 to 24 months”.

AUSTRALIA HOLDS SEVERAL OTHER KEY ATTRACTIONS FOR INVESTORS IN THE REGION, INCLUDING:

- Transparent market, with freehold titles and clear enforcement rights derived from Common Law.

- Strong links to Asia due to significant Australian college alumnus and expat populations, China now has the third largest migrant community in Australia, after the UK and New Zealand, representing 1.8 per cent of its total population. China-born students make up 20 per cent of all international enrolments in Australia.

- Strong Liquidity in the market due to significant presence of Super- funds and well rated institutional developers/privates.

FINANCING CONSIDERATION

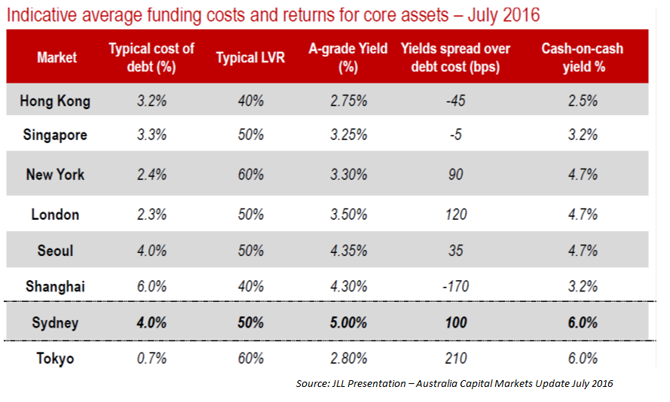

Singaporean investors have typically sourced onshore financing for their acquisitions which provide a natural hedge against their investments. Financing terms have been broadly conservative with leverage levels ranging from 40 per cent to 60 per cent and loan tenors between three to five years.

While on an absolute basis Australia’s interest rates have been higher than Singapore, when property yields are considered the net spread is substantially higher (as seen in the table below).

As an example, an A-Grade office building in Sydney would provide a yield of 5 per cent, compared with 3.25 per cent in Singapore.

{CF_IMAGE}

AUSTRALIA V SINGAPORE

Singapore’s property market continues to face headwinds in the near future in all sectors. In the office sector, around 4.2 million square feet (sqft) of office supply is expected to be completed by 2017, representing 3.5 times the average net absorption rate.

The substantial supply coupled with waning demand and downsizing from financial services sector represents headwinds for the sector.

The outlook for retail and industrial reflects similar challenging dynamics with tenants unwilling to commit given global uncertainties. As a result the office, retail and industrial sectors are likely to come under pressure in the near term with declining rents and valuations.

For the residential market, vacancies island-wide have reached a 16 year high of 8.9 per cent and is expected to trend higher given oncoming supply.

At ANZ, our experience is not only are Singaporean investors keen to expand their Australia footprint, many have over the past two years established onshore offices in Australia with local management teams to oversee their portfolio expansion.

Rohit Mohindra is Head of Commercial Real Estate, Institutional Banking, ANZ Singapore

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/global-economy/housing

Singapore’s quiet Aus property portfolio

2016-10-18

/content/dam/anzcomau/bluenotes/images/articles/2016/October/mohindraproperty_thumb.jpg

EDITOR'S PICKS

-

Whether China has a property bubble is an academic debate. The bottom line is the odds for a prolonged property slump are low on the back of urbanisation and the end of the deflationary threat.

14 September 2016 -

If you’re lucky enough to own your own slice of heaven in the land of the long white cloud you should consider yourself so.

5 September 2016 -

The Reserve Bank of New Zealand’s most recent M10 housing report shows the value of New Zealand’s housing stock (capturing changes in both the price and the number – and quality – of houses) increased in the June quarter to $NZ 959,850 million, or 381 per cent of nominal GDP. Australia has followed a very similar trajectory.

25 October 2016