-

Banks have traditionally played an important part in people’s lives. But it’s clear the financial services landscape is changing rapidly, with customers able to access an ever-increasing number of alternative options to manage their financial needs.

At the same time, consumer perceptions of traditional banks are changing. Banks are finding it harder to differentiate themselves from the competition and deliver the products and experience that meet customers evolving expectations.

" Banks are finding it harder to differentiate themselves and deliver an experience that meets evolving expectations."

Rob Colwell, EY Banking Customer Leader for OceaniaThe EY 2016 Global Consumer Banking Survey found a lack of trust, along with increased competition form new players, and changing consumer behaviours and expectations set by digital innovators are eroding the relevance of banks.

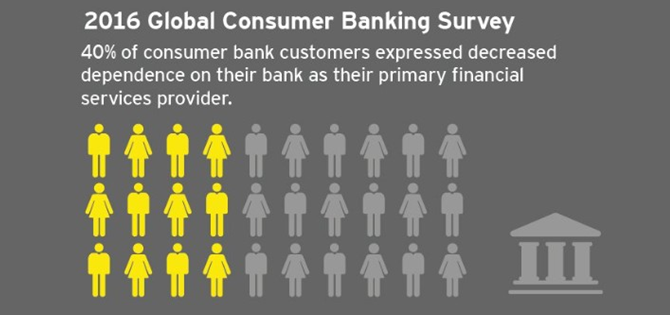

In fact, 40 per cent of the 55, 000 consumers surveyed worldwide report decreased dependence on traditional banks and increased excitement about alternatives.

WANING

Globally, retail banks scored just 75.1 out of a maximum value of 100 on the inaugural EY Bank Relevance Index, which measures how customers interact with banks now, and how they plan to in the future.

Unsurprisingly, bank relevance across the Asia-Pacific region varies quite significantly, reflective of the different stages of maturity among markets.

In Australia and New Zealand, bank relevance remains within the top third of markets surveyed globally, at 78.4 per cent and 80.6 respectively.

However, emerging markets in the region ranked lower on the relevance index, in part due to the fact customers in those areas are typically less likely to consider engaging with a traditional bank for their financial products in future.

Indonesia scored just 66.9 on the bank relevance index, the second lowest result globally. Mainland China and Indian banks also came in at the lower end of the scale, with relevance scores of 69.5 and 71.1.

{CF_IMAGE}

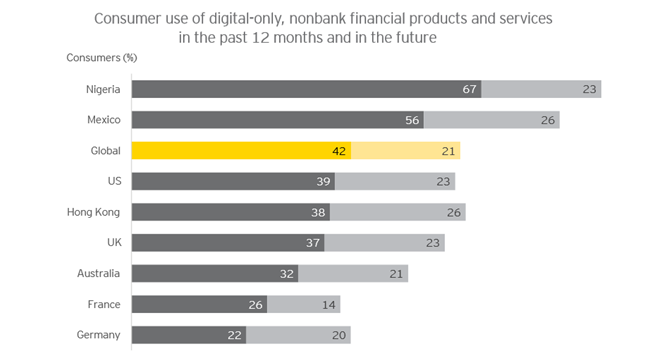

Globally, 42 percent of consumers have used non-bank providers within the last twelve months, and 21 per cent have not yet used them but plan to do so in the near future. In certain Asia-Pacific markets, the presence of non-banks is felt even more strongly.

In mainland China for example, the stronghold local fintechs have in that market is evidenced by just 70 per cent of consumers identifying a traditional bank as their primary financial service provider, much lower than the global average of 85 per cent.

Closer to home, 86 per cent of Australian consumers surveyed still use a traditional bank as their primary financial services provider. But, while most Australians still hold core products (such as mortgages, transaction and savings accounts) with banks, at least a third would consider using a non-bank for these products in future.

Consideration of alternative providers is even higher within particular product categories such as mobile payments (48 per cent), credit cards (42 per cent) and personal loans (41 per cent).

DIGITAL ON THE RISE

{CF_IMAGE}

In line with global trends, Asia-Pacific customers are also migrating quickly towards digital channels – with mainland China, India Hong Kong and Malaysia leading across the region in terms of digital adoption and usage.

In India for example, 67 per cent of customers said they had used online and mobile banking more frequently over the past year, compared to a global average of 37 per cent.

While these results make it clear banks need to deliver on digital experience, the need for offering different forms of engagement still remains.

Up to 70 per cent of respondents in mainland China, India, Indonesia, Malaysia and Singapore indicated the importance of having multiple channels to connect with their banks. Additionally, 54 per cent of respondents in Malaysia and 52 per cent in Singapore said they would not yet trust a bank without branches.

Such statistics illustrate the importance of a truly omni-channel experience. Digital cannot simply replace but rather should complement human interaction. Banks need to make sure their distribution network enables customers to interact and transition seamlessly and consistently across channels, whether online, over the phone or face to face.

But, it’s not enough for banks to segment customers based on digital savviness. Another important factor is their level of financial savviness – their level of understanding of and comfort with financial products.

By looking at a combination of these two factors, banks can get a clearer picture of customer needs and expectations.

One of the key insights from our research is 42 per cent of the digitally mature customers in Asia-Pacific are not financially savvy (and to a much lesser extent, 8 per cent are financially savvy but identify themselves as non-digital natives). This brings to light the challenge facing banks in catering to different types of customers.

While the make-up of customers in each country varies when viewed through the dual lenses of financial and digital aptitude and comfort - across Asia-Pacific as a whole, the largest segment is the aforementioned group of customers who are digitally savvy but financially non-savvy.

This suggests the need for better advice and more hand-holding through digital channels than is currently available in the market. In fact, it is precisely because of a lack of compelling offerings and financial guidance from conventional banks that make this segment ready to migrate to non-banks.

{CF_IMAGE}

MAKE CUSTOMERS LOVE THEIR BANKS AGAIN

Despite these challenges, the fight to remain relevant can still be won and we believe there is a bright future for retail banks if they focus on delivering outstanding value for their customers.

Our survey findings show four key ways traditional banks can improve their relevance among consumers.

• Build and earn trust, not only in a bank’s ability to securely look after customers’ money, but in the ability to always do the right thing for the consumer and provide unbiased, high-quality advice.

• Better understand customer behaviours and attitudes and tailor propositions to different types of customers.

• Rethink distribution and customer engagement, in particular the role of branches and customer journeys across channels.

• Innovate like fintechs to radically simplify products and deliver exceptionally simple customer experiences.

Traditional banks already have a number of advantages from their existing scale, extensive customer base, brand recognition and infrastructure. By keeping customers’ interests front and centre, banks have a real opportunity to maintain – and increase – relevance in their lives.

Rob Colwell is EY Banking Customer Leader for Oceania

The views expressed in this article are the views of the author, not Ernst & Young. The article provides general information, does not constitute advice and should not be relied on as such. Professional advice should be sought prior to any action being taken in reliance on any of the information. Liability limited by a scheme approved under Professional Standards Legislation.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

Share

anzcomau:Bluenotes/business-finance,anzcomau:Bluenotes/business-finance/banking

Are banks still relevant?

2016-10-13

/content/dam/anzcomau/bluenotes/images/articles/2016/October/colwellbanks_thumb.png

EDITOR'S PICKS

-

The seemingly inexorable trend towards a cashless society continues as contactless payments and mobile wallets replace cash in consumer commerce and real-time payments occur deeper and deeper into the world of small as well as large business.

28 September 2016 -

Glenn Stevens retired from the Reserve bank of Australia in September, warning the country risks lulling itself into a false sense of security by constantly retelling the “25-years-without-a-recession” narrative.

5 October 2016 -

In Australia last week, the banking industry was focussed on a parliamentary inquiry into the industry’s culture and response to a range of issues from customer complaints to pricing to market behaviour.

12 October 2016