-

The G20’s deliberations over the weekend demonstrated the financial crisis is not over some eight years later. Global growth is fragile, monetary policy fraught, trade barriers are growing not falling (for example, in the year up to the latest confab, G20 governments imposed 350 new measures discriminating against foreign commercial interests, almost four times the number in 2009).

The financial system, which caused the crisis, is however a relatively positive story. While some banks globally remain weak, an intense program of re-capitalisation and several waves of new regulation mean the leaders of the major economies didn’t need to worry too much about systemic crisis.

" The financial system, which caused the crisis, is a relatively positive story."

Andrew Cornell, BlueNotes managing editorBut that doesn’t mean the focus on the banking system is lessening. Indeed, the post-crisis regulatory agenda is entering a newer, less prescriptive but perhaps even more significant phase.

One of the world’s higher-profile central bankers, Andreas Dombret, an executive board member of the Deutsche Bundesbank, captured this in a speech just before the G20 aptly titled “Are we done now? Reflections on the post-crisis supervisory and regulatory regime”.

“In my view, the supervisory and regulatory changes witnessed in Europe and in many other parts of the planet do not represent a response to a call for "optimal" stability, but they have set the basis for an evolutionarily fit regime. It is not just a matter of quantity, as suggested by current arguments about calibration and by newspaper articles focusing on over-regulation,” he said - a warning that while the current regulatory pipeline may be nearly empty, that’s not the end.

In fact, Dombret reminded the banking industry there would be more and more scrutiny of more intangible measures such as culture and social licence.

“Supervisors have even sharpened their focus on the culture and behaviour of bank officials,” he noted.

“There is in fact a link between the behavioural inclinations of these officials and actual solvency: all of the steps taken are geared to minimising the likelihood of deterioration and failure at the earliest possible stage.”

OVERSIGHT

Just what this means can be discerned in another document released in the run up to the G20, the Financial Stability Board’s (FSB) second progress report on Measures to reduce misconduct risk.

Stressing how important ethical conduct and compliance with both the letter and spirit of applicable laws and regulations is for public trust, the FSB noted “misconduct is also relevant to prudential oversight as it can potentially affect the safety and soundness of a particular financial institution”.

Despite the political atmosphere in Australia and other incidents in Asia, this dimension of the financial system has been far more critically injured in the northern hemisphere, both during and after the financial crisis, and so the global regulatory work has orbited those events.

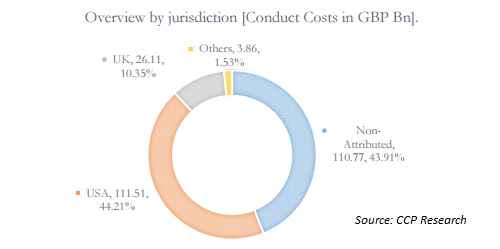

According the London-based Conduct Costs Project, the running total of fines for the most penalised global banks between 2011 and 2015 was £252 billion.

As Roger McCormick, managing director, CCP Research Foundation and director of the Conduct Costs Project says in his forward to the project’s latest report“not even the largest banks can now settle for regarding them merely as ‘costs of doing business.’ And the public would hardly condone such an attitude or see it as consistent with a desire to regain trust.”

This is the broad context around why banks globally are now paying such close attention to fundamental questions such as their own culture and their role in society, not just the economic contribution they make in terms of jobs, tax and shareholder returns but as part of a healthy society.

Certainly, in Australia at the moment, that broader social debate is front and centre even when the monetary value of conduct costs, while obviously significant and undesirable, are a fraction of those incurred by banks in the northern hemisphere.

In this context, the FSB’s workplan covers whether reforms to incentives, for instance to governance and compensation structures, are having sufficient effect on reducing misconduct; improving global standards of conduct in the fixed income, commodities and currency (FICC) markets; and reforming major benchmarks.

The FSB has been consulting widely with the industry, undertaking rigorous research, and is looking at compensation tools such as rapidly adjusting bonuses and clawing back remuneration already paid. The board is also looking at compensation standards.

In addition, the FSB also held a roundtable with major financial services companies to discuss governance frameworks to address misconduct.

FURTHER STRENGTHEN

The second focus is market practices under the auspices of the International Organisation for Securities Commissions (IOSCO) which continues to explore ways to further strengthen the current global framework to address misconduct by firms and individuals in professional markets.

The Foreign Exchange Working Group of the Bank for International Settlements (BIS) issued its first phase of the Global Code of Conduct for the Foreign Exchange Market earlier this year with a complete code and adherence mechanisms to be released in May 2017.

The third focus is financial benchmarks and extensive work is being undertaken globally, including in the Asian region, to improve the integrity of these vital components of financial markets.

“IOSCO has undertaken a number of projects with respect to benchmarks reform which are aimed primarily at assessing the degree of implementation of the Principles for Financial Benchmarks by benchmark administrators operating in IOSCO jurisdictions,” the FSB said.

“By end-2016, IOSCO will finalise guidance for benchmark administrators on the content of the statements of compliance that administrators are expected to publish.”

The scale and rigour of these programs is clear evidence the global regulatory complex will have a much greater focus on culture but that, despite what will undoubtedly a new library of regulation, does not mean a proper culture can be regulated into being.

As Dombret said in his speech, financial systems “adapt” very readily and by that he meant no amount of prescriptive regulation can guarantee good behaviour. Good behaviour though makes money and so it is enlightened self-interest for institutions to take it very seriously.

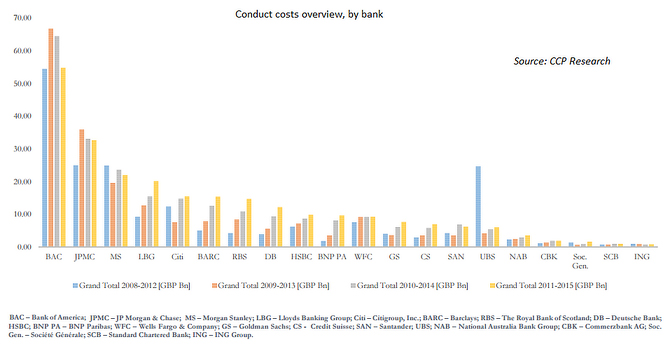

For a number of banks in the northern hemisphere, fines and compensation have wiped out profits for several years running. International bank investors now factor in a discount on bank share price valuations to account for unknown but expected conduct costs.

{CF_IMAGE}

“The conduct costs incurred by these systemically important financial institutions have impacted materially on their performance (and in some cases led to prudential consequences) - not to mention the incalculable reputational cost, the difficult-to-ascertain indirect costs of misconduct and, of course, the ‘unknown unknowns’,” says Chris Stears, the CCP Research Foundation director.

In jurisdictions like Australia, even where direct regulator-imposed conduct costs have not reached this scale, the financial sector faces the cost of political inquiry and reputational issues. Regulation though, as the global regulators recognise, is only part of the answer.

Andrew Cornell is managing editor at BlueNotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

EDITOR'S PICKS

-

It’s indisputable the level of core capital banks must carry is rising higher and higher; nor is it in dispute capital was too low when the financial crisis hit. Indeed, some prominent authorities, including former Bank of England governor Mervyn King and Financial Times columnist Martin Wolf, believe in even higher levels of capital.

16 August 2016 -

Shareholders are meant to focus on creating long-term value but is this possible in an environment which measures returns daily and where analyst reports focus on this and next year’s outcomes? Similarly, public companies aim to deliver superior medium-term results but are measured quarterly.

11 August 2016 -

What finally sees off an ageing, ailing business model is not always the most obvious threat. In journalism, for example, the end of print newspapers may not come just because Facebook or the iPhone are now what is read on trains.

30 August 2016