-

My great grandfather was a banker in Brookings, South Dakota – a town built around a rail junction deep in farm country. His name was John David Wilson but everyone called him ‘JD’.

He was a resourceful, hard-working teetotaler, married to a woman just as smart as he was. They bought a house with extra bedrooms and took in railway workers as boarders.

" Banks are full of numbers to which attention must be paid, but also people whose values and instincts matter."

Harrison Young, Banker, company director & novelistWhen the economy turned against some of his banking customers, he accepted butter and eggs in repayment of loans, selling them in Minneapolis, which was three hundred fifty kilometers away.

When the Panic of 1907 drained all the cash out of Brookings, he and the other two bankers in town sat down at a dining-room table and wrote stacks of personal checks, which circulated as currency for several weeks.

Along with the bank and his butter-and-egg business, JD owned the town’s telephone exchange and a company which built and repaired windmills. He bought the first automobile in the state and drove it on a Sunday. It fell apart under him, which he regarded as a ‘judgment’ for dishonoring the Lord’s Day.

He sent away for the plans and spent his Saturday afternoons reassembling the vehicle, which so impressed the people at Ford they gave him a dealership.

JD’s bank failed eventually, as small banks will in difficult times, but not for lack of prudence. My great grandmother liked to tell a story about her husband seeing one of his borrowers buying strawberries in the weekly market.

He walked straight back to the office and called the man’s loan. No farmer, JD explained, had any business buying strawberries. The man had had one good harvest, so he thought he was rich!

NOT LIKE THE OTHERS

I share this bit of family history to make three points. The first has to do with the central role banks play in an economy. They are not, as some people claim, ‘just like any other business’.

Banks perform an intermediation function, and in doing so resemble markets. JD knew everyone, saw everything and unhesitatingly passed judgment – as markets do.

The second point is the importance of trust. It runs in both directions. The people of Brookings accepted their bankers’ personal IOUs in a panic. When JD decided he didn’t trust that farmer’s judgment, he immediately terminated their commercial relationship.

My third observation is banking is hard. The business is hostage to an uncertain future – which bankers tend not to talk about, lest they frighten depositors. JD had a talent for business. He was as shrewd as any man in town. Of the many enterprises he launched, only the bank failed.

As we walk through the business model of banking, the inherent risks of the model and how those risks are mitigated or managed, it may be helpful to keep JD in mind. Banks are full of numbers to which attention must be paid. But they are also full of people whose values and instincts matter.

Joining the board of a bank is an optimistic act. The more time passes since the last crisis, the more confident management will become. To do their job properly, directors must never lose sight of the institution’s vulnerabilities.

FINANCIAL ARCHITECTURE

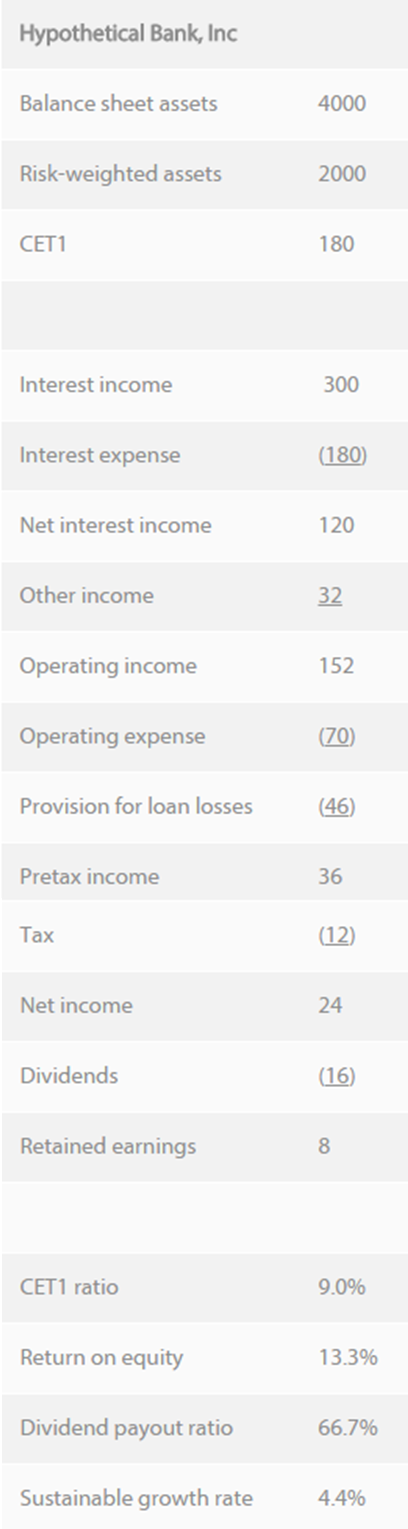

Banks attract deposits by offering safety and convenience. They also pay interest, but less than they would have to if they weren’t banks. They use the funds they attract primarily to make loans.

They also hold government securities as a liquidity reserve. They have a remarkably small amount of shareholders’ equity. That’s the balance sheet at its most basic.

The income statement starts with net interest income, or interest on assets minus interest on liabilities.

Fifty years ago, gross interest income headed the list of revenue items, and interest expense the list of costs. But these figures vary with the level of interest rates, so an increase or decrease in gross interest income doesn’t tell you as much as an increase or decrease in sales would in a non-financial enterprise.

The net interest figure has come to be preferred. Net interest margin – the difference between interest rates earned and paid – gets unwavering focus from both bank managers and bank investors.

POSITIVE

Banks are able to generate positive net interest income for four reasons. As noted above, they pay for deposits in part with safety and convenience. They have equity capital, on which no interest is paid. They engage in maturity transformation. And they charge borrowers a greater spread over the risk free rate than their own liability-holders demand.

Households and businesses turn to banks, and pay those greater spreads, for one of two reasons: they are too small to get access to capital markets, or their financing needs require bespoke analysis and structuring bond and money-market investors are not equipped to provide.

Lending is the engine-room of banking. It is only by making loans that the benefits of a liability franchise can be realised. Most of the risk banks take is credit risk. The credit risk that matters is what happens one year in ten or twenty, when a macroeconomic downturn or an upheaval in an important industry causes losses to bunch up.

‘Maturity transformation’ refers to the way banks turn contractually short-term deposits into behaviorally medium-term liabilities.

People leave their money in a bank. This permits banks to lend long and borrow short, allowing firms and households to do the opposite, which is what they want.

In a normal or upward-sloping yield curve environment, carrying long-term assets with contractually short-term liabilities earns the bank part of its net interest income. In a world where interest rates move around a lot, the mismatch between asset and liability re-pricing dates can make or lose a bank a lot of money.

The discipline that addresses the risk is referred to as ‘asset/liability management’. It came to prominence in the United States in the 1970s and ‘80s.

Savings institutions, which had large portfolios of long-term, fixed-rate mortgage loans, were badly squeezed – in some cases risking capital insolvency – when the Fed’s battle with inflation meant short-term interest rates rose sharply and they had to increase what they paid on their savings deposits to avoidb becoming liquidity insolvent.

Mismatch risk is a form of market risk. It is an intrinsic feature of the business model. You sign up for it when you invest in a bank. Tools exist to limit mismatch risk, which is what most commercial banks try to do. Some banks elect to accept mismatch risk, or even to take additional market risk by buying bonds and financing them in the overnight ‘repo’ market.

Banks are compensated for taking market and liquidity risk – and for various lower-risk services – with commissions and fees, plus trading profits. ‘Operating income” is the sum of these items plus net interest income.

Banks make a profit when operating income exceeds the sum of operating expenses plus provision for loan losses (trading losses and operational losses, when they occur, are typically deducted in arriving at the “other income” figure).

Operating expenses, such as salaries and rent, can be managed. They will tend to grow but they need not fluctuate a great deal. Losses are different. Most of the time they seem predictable.

Analysts build them into their financial models. Banks set prices that cover business-as-usual or “expected” losses. But every decade or so, a recession will make loan losses balloon. Or a sudden shift in market rates will catch the bank’s treasury in a painfully mismatched position.

Every so often, a rogue trader or an IT snafu will cost some bank a bundle. Such events are sometimes referred to as ‘unexpected losses’, but that is a misnomer. The big ones are hard to predict but you know they will happen eventually.

Banks seek an acceptable return on equity with a combination of low margins and high leverage. The limit on leverage – or to be accurate, one of the limits – is the need to absorb occasional large losses.

The more volatile net income is in any enterprise, the greater its need for capital. Bank capital is a fraught subject. I won’t go into it here. But to fill in this sketch, let me note the other limits on bank leverage are the confidence of depositors, the opinions of rating agencies and government regulations.

The last bit of architecture to note – since we are speaking of return on equity – is banks answer to a number of stakeholders in addition to owners.

All enterprises do, but the central role banks play and the government sponsorship they receive gives them more stakeholders, and more vociferous ones.

It is possible to view banks as clearing houses, balancing the competing claims of depositors, borrowers, shareholders, bond investors, employees (both staff and managers), suppliers, the government of the day and the community at large.

This description fits banks better than it does non-financial corporations – and helps explain why many banks (and insurance companies) once operated as mutual organisations.

Whatever corporate form is adopted, the inherent risks of banking are pretty obvious: a collapse of depositor confidence, peak loan losses, earthquakes in the market, operational catastrophes (whether from fraud or honest error) and changes in the terms of whatever ‘deal’ banks have with government and society.

This last phrase refers to the fact politics, community expectations and historical accident together determine the regulatory framework and industry structure banks contend with and benefit from.

CHARACTERISTIC FEATURES

Over time, banks have found ways to mitigate the risks and uncertainties they face – approaches sufficiently widespread enough to be better described as features of their business model than as risk management strategies.

Strategy involves choices. Arguably, to have a strategy, you must be able to cite things you are not going to do. For example, is diversification optional? You can get into a semantic muddle pursuing such questions. Suffice it to say in describing banking to someone new to the subject, you’d probably at least mention the aspects of the business called out below in bold.

Since banks have significant leverage – as little as three or four dollars of equity for every hundred dollars of balance sheet assets – they can’t handle big individual losses.

Diversification – to answer the question in the previous paragraph – is therefore mandatory and becomes instinctive. A well-run bank will prefer ten loans to different borrowers to a single, giant credit, despite the greater administrative expense.

If those ten borrowers are in industries which respond differently to the macroeconomic cycle, that’s even better. By the same token, a sensible bank treasurer will feel uncomfortable if too many of his time deposits come from only a few customers or geographies.

Diversification means there are thousands of risk decisions to make, with the result that decision-making authority is dispersed among large numbers of employees and executives.

Causing all those foot soldiers to make wise choices is a significant managerial challenge. Banks respond with detailed policies, procedures, limits and controls – layers of bureaucracy sometimes referred to as a ‘risk management framework’.

All organisations face risks, of course, and find ways to manage them, but the density of administration devoted to risk management is peculiar to banking.

Another feature of the business that deeply affects bank behaviour is the asymmetrical nature of credit risk. There is far more downside than upside. Lenders earn a scrap of net interest but can lose the whole loan. Boldness is not normally a virtue.

A banker I know describes his situation this way: “I am in the business of not making mistakes. My strategy is attention to detail.” There are no successful sloppy banks.

Managing a deposit franchise, a loan portfolio and the mismatch between them is strengthened by a bank’s deep understanding of customer needs and counterparty behaviour. To be successful over the long term, banks must be perpetual students of their own assets and liabilities.

We see the accumulation of proprietary knowledge as a fundamental characteristic of the business model. There was a time when this meant observing the daily cash flows in and out of a borrower’s account to monitor the health of his business. Today, banks increasingly rely on algorithms to keep watch.

Successful bankers have traditionally been good judges of character. Many people are skeptical about a computer’s capacity to play that role. I believe they misread the matter. The job of computers is not to replace human intuition but to spot warning signs less obvious than a farmer’s purchase of strawberries.

Despite the prevalence of computers – in some cases because of it – banks are not invariably good at handling the transactions and information they touch. The poet, Randall Jarrell, facetiously but accurately defined the novel as “a prose fiction of a certain length that has something wrong with it”.

In that spirit, a bank could be defined as a leveraged enterprise with data problems. Having to wrestle with those problems and the legacy systems that spawn them is a fundamental feature of life inside a bank.

THINK IT WORKS

Maturity transformation only works so long as people think it works. Sometimes depositors panic. They mostly panic because they think other people will, so there isn’t necessarily logic to it.

Over the course of the 19th Century, the Bank of England gradually accepted a role as ‘lender of last resort,’ and other central banks have followed their example.

Strictly speaking, a lender of last resort provides temporary funding, in unlimited quantities but at a penalty rate, to a bank that runs out of cash, provided the bank is capital solvent and can post good collateral.

A banking crisis does terrible damage to the real economy. It doesn’t matter whether the crisis is a function of irrational panic or was precipitated by very real credit or dealing room losses. Businesses fail that shouldn’t have to. People lose their jobs, and perhaps their houses.

Over time, lender-of-last-resort facilities have been supplemented in many countries with deposit insurance, explicit government guaranties, loans against more dubious assets, and a history of intervention that can function as an implicit guarantee.

There is a vast literature on whether any of this was or is good public policy. But it is an observable fact most banks around the world enjoy some sort of government support. In my opinion, this is better seen as a feature of the business model than as moral failure.

Having put taxpayers at risk in the interest of financial stability, governments feel entitled and obliged to moderate bank risk-taking. In this endeavor they have issued whole shelves of regulations, which specify minimum capital ratios and liquidity buffers, control branching, require approval of mergers, limit the activities banks can engage in, and in some countries impose floors or ceilings on the interest rates they can offer or charge.

Under ‘fit and proper’ provisions of many banking acts, you cannot be a senior officer or director of a bank without regulatory approval. One way or another, most countries find ways to control the ownership of banks. And supranational organisations in Basel and Washington now publish guidelines telling national regulators what they ought to be doing.

Seeing the amount of time and energy devoted to the project, non-bankers might conclude perfecting regulation is the answer to it all. They would be wrong. Rules alone won’t make a bank resilient. The business model of banking only “works” because of additional features that confront human limitations indirectly.

The first of these is governance arrangements which create checks and balances. Boards rather than management must decide – at a high level but in a formal way – how much risk the bank will take.

A bank must have a risk function that monitors compliance with the board’s directives and is headed by a chief risk officer with direct access to the board. A board must have a majority of independent members.

Implicit in all this is a judgment that risk-taking benefits from the involvement of individuals, some of them part of management, some non-executive directors, who maintain a bit of distance from the business.

The second ‘soft’ feature of the business model is the importance of culture – both the ‘organisational’ and ‘risk’ varieties. If ‘culture’ is defined as a set of beliefs, behaviors and skills that characterise a particular society or organisation, ‘risk culture’ is those aspects of organisational culture that help bankers see risks, provide a language and occasions for discussing them, and offer guidance when there is no rule.

As the word is generally used, ‘governance’ refers to how power, accountability and reward are distributed in a society or organisation.

This makes compensation part of governance. But there’s overlap here, because the compensation system has a significant impact on an organisation’s culture.

One root cause of the Global Financial Crisis was the tendency of some bankers to define themselves as opportunistic entrepreneurs. This was sometimes referred to as the ‘bonus culture’.

My final observation is banks work best when bankers see themselves as members of a profession. By ‘profession’ I mean the world-wide company of bankers and the knowledge and instincts that have always characterised the best of them.

This includes a sharp pencil and a sceptical temperament, to be sure, but also a sense of fiduciary obligation matching the privileged position banks occupy.

Both institutional and systemic resilience benefit when bankers take a long-term view and define their job as serving the full range of bank stakeholders.

Harrison Young is a company director, the former chairman of NBNCO, a former banker and regulator. You can follow him on Twitter @harrisonyoungpa, at his blog or on Medium.

This story originally appeared on LinkedIn.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

Share

anzcomau:Bluenotes/business-finance,anzcomau:Bluenotes/business-finance/banking

LONGREAD: How banks really work

2016-09-02

/content/dam/anzcomau/bluenotes/images/articles/2016/September/youngbanks_banner.jpg

EDITOR'S PICKS

-

Like the shirt on a farmer’s back, the cotton industry is tight. It’s an industry with its act together, with collaboration and connections all the way from industry leadership to the integration of production, ginning and marketing.

25 August 2016 -

Climate change creates risks for all businesses and incorrectly assessing the impact of climate change on in the market they operate puts sustainable growth at risk.

23 August 2016 -

Award-winning Illustrator Rod Clement shares his uniquely quirky take on the corporate world. This week: #winterofdiscontent.

26 August 2016