-

A senior regional policy advisor I really admire refuses to describe the Chinese economy as ‘slowing’. I agree. But we are not 'slowdown deniers' - we both acknowledge a slowing China is a reality but feel this term in particular is a misnomer.

Something far more complex and profound is happening in the Chinese economy which only at the simplest level could be described as a slowdown. Rather, the Chinese economy is de-industrialising and rebalancing remarkably early in this phase of its historical development profile.

"Something far more complex and profound is happening in the Chinese economy which only at the simplest level could be described as a slowdown."

Glenn Maguire, Chief Economist, South Asia, ASEAN & Pacific at ANZMany will say this de-industrialisation is premature and China cannot rebalance so rapidly. But history tells us otherwise, particularly with the global rupture of the Chinese industrialisation and modernisation episode of the 1990s and 2000s.

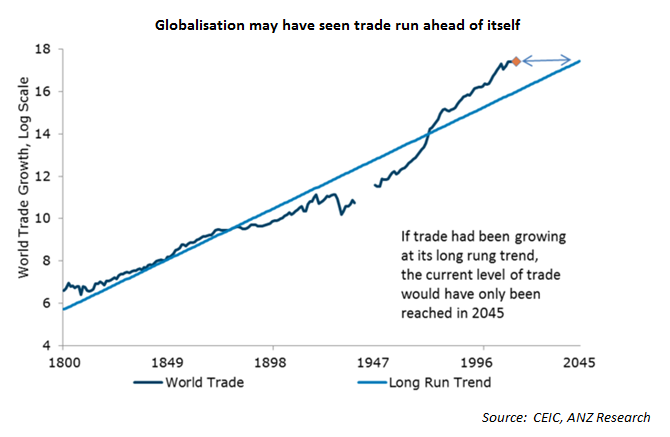

It was only 15 years ago China completed Word Trade Organisation ascension. Over that period the country rapidly emerged to account for 14 per cent of global merchandise trade in 2015 - from just 3.9 per cent in 2000.

{CF_IMAGE}

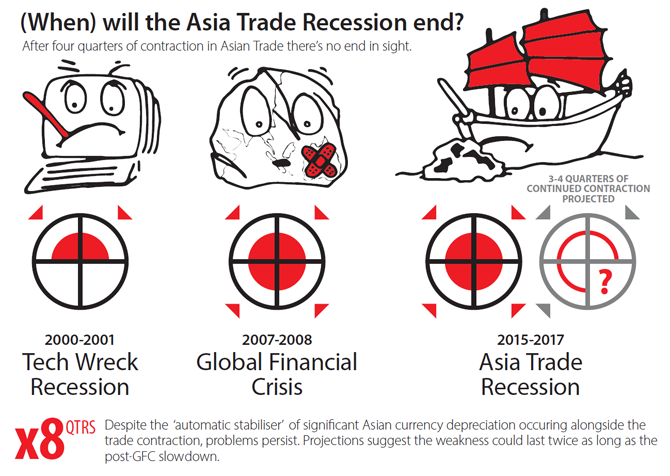

The 2000/01 tech wreck saw two quarters of trade contraction. The 2007/08 global financial crisis saw four. The current period has seen four quarters of contraction already and on our current forecasts, we expect to see it extend for another three to four quarters. ILLUSTRATION: Matt Nicol

It was China’s heavily led production and investment growth model which accounted for the bulk of the rise in global trade share as it built itself into the factory of the world and imported the commodities, capital goods and inputs to enable that.

So how did China go from being such a positive support to global trade to a negative disruptor, particularly for the rest of Asia?

REBALANCING

{CF_IMAGE}

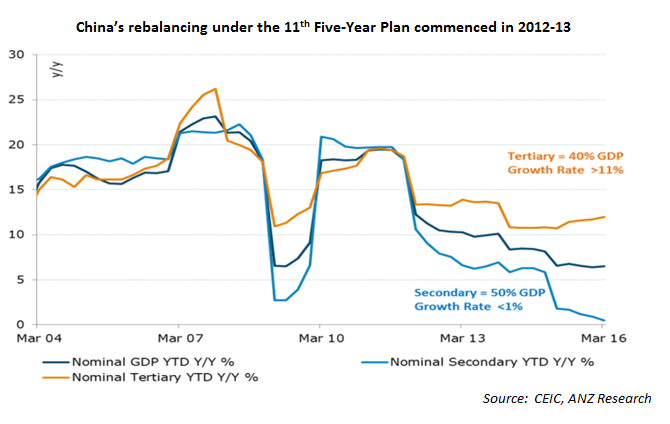

With the benefit of hindsight – and a few charts – the pivotal moment is now clearly apparent. The Twelfth Five-Year Plan (debated in mid-October 2010 at the fifth Plenym of the 17th Central Committee of the Communist Party of China (CPC) and approved by the National People's Congress in March 2011) clearly stated China’s ambitions to move to create a more sustainable growth model.

The model was to shift economic growth away from a reliance on exports and investment toward domestic consumption.

Aligned with this, industry structure would aim to accelerate the growth of China’s services industries whilst targeting a reduction in those industries suffering from overcapacity or inefficiencies – largely heavy industry associated with infrastructure and industrial production.

{CF_IMAGE}

That was just over five years ago. It is very clear shortly after the relative performance of the Chinese industrial structure started to bifurcate with tertiary industry (services) maintaining a strong growth rate whilst secondary industry (investment and production aligned sectors) started to slow.

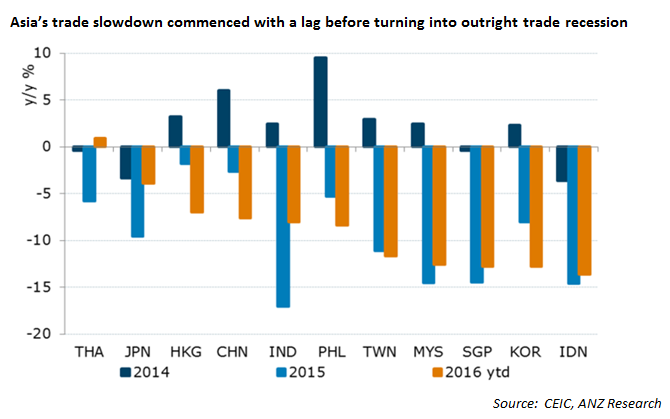

With a lag of around one to two years, Asian Trade started to slow in step, before falling into a dramatic contraction over 2015 and thus far into 2016.

If relative rates of growth of the tertiary and secondary sector are maintained, than in a similar period of five years, services will be a larger component of the Chinese economy than industry.

That is to say, China will have engineered a deindustrialisation in the space of just five years.

This is a dynamic unprecedented globally but in the Chinese context business as usual (if fundamentally re-engineering the economic model can be called business).

There are many causal factors behind Asia’s trade recession, some cyclical, some structural, some related to globalisation, but developments in China seem to be at the nexus of all explanations.

During this reengineering and rebalancing the Chinese economy finds itself in what economists refer to as a disequilibrium position.

It is this transition away from the old industrial/investment led model that was so heavily reliant on the rest of the world that has caused global trade and commodity prices to swoon.

NEVER BEFORE

The impact on Asia of this disequilibrium has been as profound as it is unprecedented. Never has Asia experienced a retrenchment in trade of the extent, duration, breadth and depth that it is now experiencing.

Though the disequilibrium is having extremely disruptive impacts, it can be explained relatively simply. The supply side of the Chinese economy is increasingly becoming a services one, requiring the demand side of the Chinese economy to be a consumption-led one, not an investment-led one.

The Asian Trade Recession is evidence of the sharp decline in the contributions to growth from both industry and investment, hence the type of goods (components and capital goods) Asia has provided to China are no longer required.

However, though a rebalancing to services and consumption is evident, at this time it is not sufficient to offset the decline in industry and investment.

As long as China’s consumption demand (particularly for services) can be met from domestic supply, China’s call on the rest of the region is likely to remain low. Hence, our intuition is China will remain a significant contributor to the regional trade recession for the foreseeable future.

A TALE OF TWO ECONOMIES

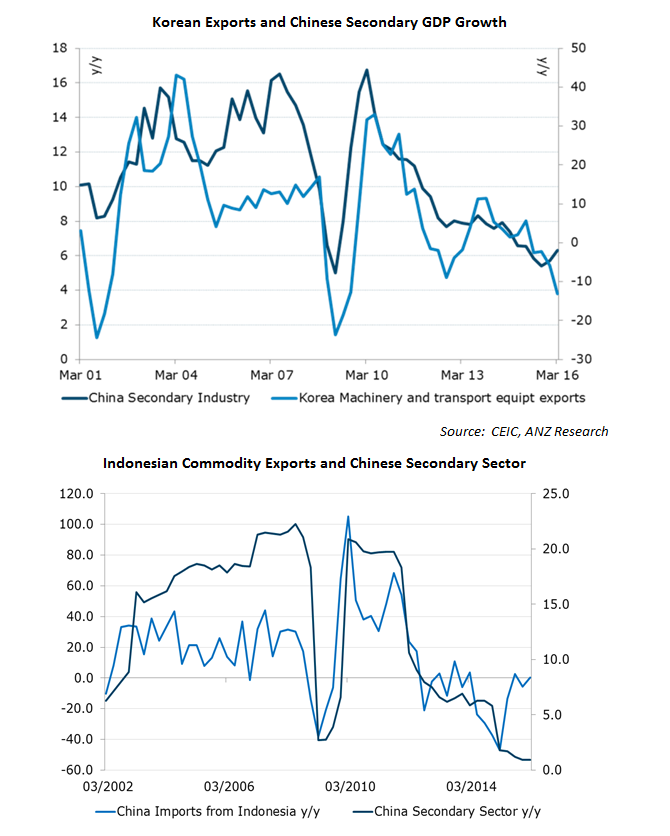

The breadth and depth of China’s hold on the rest of Asia is illustrated by considering two economies at opposite ends of the value-added spectrum. South Korea is an exporter of high-value added capital goods such as semi-conductor foundries. Indonesia is an exporter of lower value added raw commodities.

{CF_IMAGE}

China is also changing the region in a more technical way – via its utilisation of and position in supply chains. As a result of an ageing population and strong increases in wages, production of some lower-value added activities has already begun to shift to lower-cost economies in the Mekong.

This automatically lowers actual investment in new production facilities in those sectors in China and increases outward foreign direct investment into other economies capital stock.

Meanwhile, the benefits of over nearly two decades of strong foreign direct investment (FDI) into China has allowed it to move into production activities which add more value - but more importantly, it no longer needs to import those mid-value components from the region it historically did in the 2000s.

Rather, China is now producing these mid-to-high value added components itself, adding an additional structural element to the impact on the regional trade recession.

{CF_IMAGE}

The shift from an investment-led growth model to a consumption-led growth model will obviously see China import less investment goods from the rest of the world.

But as it moves into producing its own mid-value goods, such as electronics, chips, components and parts for handsets and tablets as well as those goods themselves, China’s call on Asian supply chains will also fall.

This is dramatically reflected in the sharp fall of China’s import-intensity over the post crisis period.

{CF_IMAGE}

China and hence the region now finds itself in an awkward position it is historically unaccustomed too. The country is producing enough services and consumer goods domestically to satisfy current levels of domestic demand.

Yet the regional and global supply chains China is firmly embedded in are structured not just to meet Chinese domestic demand but also its production of manufactured goods (consumer and industrial) for the rest of the world.

As China’s appetite for consumer goods and services grows, it is likely its capacity to produce those goods and services will also grow, so the question of whether China ever again fully engages regional and global supply chains is a valid one.

Until then this rebalancing will continue to create a trade recession in the rest of Asia.

How quickly will this trade recession end? We can’t be sure. What we can be sure of is a rebalanced China is both a necessary and sufficient condition for Asia’s trade recession to end.

Unfortunately that dynamic looks to be a little bit further in the offing than the consensus suggests.

Glenn Maguire is Chief Economist, South Asia, ASEAN & Pacific at ANZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

-

-

-

Share

anzcomau:Bluenotes/asia-pacific-region,anzcomau:Bluenotes/asia-pacific-region/economics

How China’s rebalancing has created a trade recession in Asia

2016-07-20

/content/dam/anzcomau/bluenotes/images/articles/2016/July/maguireasia_thumb.png

EDITOR'S PICKS

-

The Asia-Pacific is growing old. Fast. But it is also a ‘silver mine’ worth prospecting by a wide range of companies.

28 June 2016 -

Opportunity is not the whole story. New Zealand knows the Asian opportunity: Asia makes up a quarter of global GDP and ANZ expects this to rise to over 50 per cent by 2050. That’s a big playground.

14 June 2016 -

With hindsight, policy makers might not choose to launch what is called by some an Asian EU at this point in time.

18 July 2016