-

Even in the 1990s, when Australian banks copped a lot of flak for closing branches, consumer behaviour was changing.

"The shift from [traditional banking] has been immense. But the next generational shift in financial services – and services more generally – will be even more confronting."

Andrew Cornell, BlueNotes managing editorThe banks may not have undertaken their branch network rationalisations in the most amenable fashion for the wider community but even then, as data from the Australian Prudential Regulation Authority show, actual points of representation didn’t change as much as the headlines suggested.

Indeed, points of representation actually increased for 11 straight years from 2001, the first year APRA started compiling proper data.

The shift from traditional branch banking and physical currency has been immense. But the next generational shift in financial services – and services more generally – will be even more confronting. What happens when your financial advice comes from artificial intelligence?

Branches were closed because of mergers and because foot traffic shifted – less large high-street branches, more shopping centre ones – but mainly because customers changed. They started using ATMs and Eftpos and telephone banking for basic transactions.

With the arrival of the internet and then ecommerce, even more everyday activity was undertaken outside the branch.

Yet branches have not, and won’t for the foreseeable future, disappear. To date – and this is where the development of AI looms large – certain categories of financial services have resisted full automation. They are typically higher value and more complex interactions such as home loans, financial advice and wealth management.

THE EDIFICE EFFECT

Even with the opening of ANZ’s newest branch, in Martin Place in Sydney, bricks and mortar (or maybe glass and polycarbonate) are just as striking as the digital services.

Bank branches were originally the grand buildings of old because of what was known as the ‘edifice effect’ – substantial buildings gave the impression of greater security and were important in attracting deposits.

To a large extent brands have replaced edifices in modern financial services but as ANZ’s head of Australian banking Fred Ohlsson told BlueNotes at the opening of the branch, human interaction is still critical in a digital world.

There is certainly resistance to removing human interaction from key services, extending beyond finance. Government services in particular are often criticised for automation and the use of call centres although frequently this is because the process itself is implemented poorly, rather than automation per se being unpopular.

Despite concerns automation and online services disenfranchise vulnerable and marginal groups, it is service itself which is the issue: poor service, whether human or machine, creates particular issues.

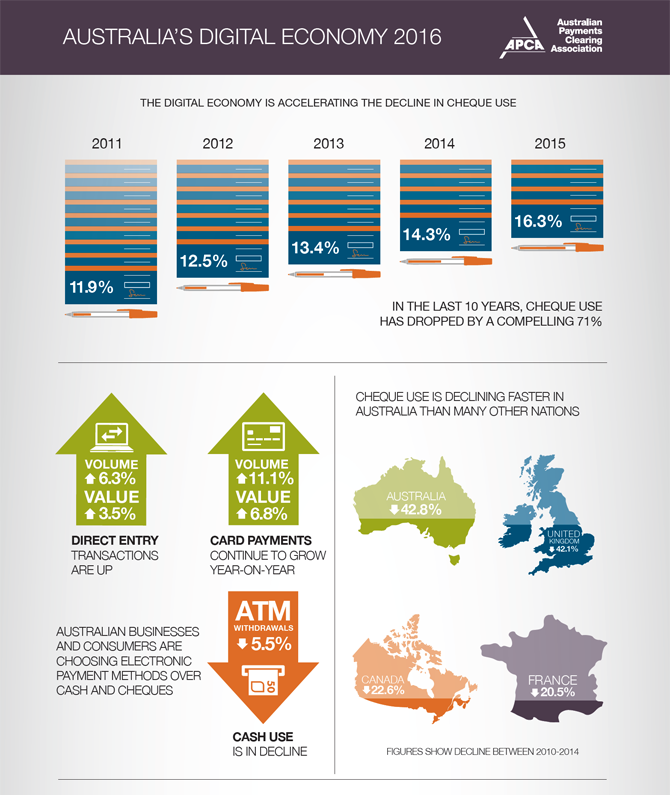

Cheques and indeed cash are a case in point. People have a traditional attachment to them as a means of exchange. Moves to shift towards the elimination of cheques in both the UK and Australian faced a strong community backlash.

But the Australian Payments Clearing Association’s annual review of payments shows the use of cheques has been in steady, terminal decline for over a decade.

“Cheque use is declining faster in Australia than many other nations although the decline in cheque use is a global phenomenon,” APCA said in its latest report.

“Australia has the third highest appetite for digital engagement in the world following Canada and the USA. Digital interactions influence 40 per cent of in-store visits in Australia, compared with 27 per cent in the UK.

“Of these digitally influenced shoppers, 65 per cent use a digital device before and 31 per cent during a shopping trip. Not only do consumers browse in-store and then go online in search of the lowest-cost option, but they also research online and buy in-store.”

“The key driving motivations for Australian online consumers are convenience and cost, with the top purchases being travel, books/music/stationery, and groceries.”

Now Medicare, the Australian health insurance system, has announced it will no longer use cheques to credit rebates, only digital means.

Yet in some ways these trends are yesterday’s stories. There will no doubt be sturm and drang about branch closures, call centres, automation, lack of cheques, for years to come. We are all creatures of habit.

{CF_IMAGE}

Yet with the arrival of artificial intelligence (AI), already evident in rudimentary form with so-called “robo-advice”, and virtual reality, the next evolution will not just be about replacing paper with bits.

Legendary investor Warren Buffett made waves when he told his millions of fans it was better to have most of your investments in passive, index funds rather than use active investors. His argument was active investors as a group did not outperform the indices they were benchmarked against and charged high fees for failing to do so.

The work of New York University’s Thomas Philippon argues the unit costs of financial services have barely declined in over a century. While financial services have become more complicated, Philippon, like Buffett, believes the costs of human agents have been the main impediment to lower prices.

{CF_IMAGE}

There is some evidence over the last decade and a half that unit costs are falling. That may well be to do with far greater levels of automation.This is where AI and roboadvice could make a difference.

But there is a difference in kind between what has happened with the digitalisation of transaction services and the incursion of automation into complex advice. Transactions are in essence straightforward. Whether by cash, cheque on online, fixed value is transferred from one store of value to another.

Passive funds in a way are similar. They track an index.

When it comes to financial advice however, the variables are far more numerous - the client’s individual circumstances, risk profile, even changing economic circumstances. Even for a home loan, the possible choices and influences are vastly more complicated than a payment.

The legal ramifications too are only just being explored. Consider the analogy of a self-driving car. If there is a crash, who is responsible when there’s no driver? The car manufacturer? The software company which designed the driving system? The operator of the network which the software relies upon?

That’s not to say AI won’t have a profound impact, nor people inherently trust other people more than a machine. Consider the Japanese shirt selling robot with better sales figures than humans – because customers trust it to be honest.

Andrew Cornell is managing editor at ANZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

Share

anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/technology-innovation/disruption,anzcomau:Bluenotes/technology-innovation/fintech,anzcomau:Bluenotes/technology-innovation/innovation

The next evolution of financial services

2016-05-24

/content/dam/anzcomau/bluenotes/images/articles/2016/May/cornelldig_thumb.png

EDITOR'S PICKS

-

In an age of disruption, can big companies ever really innovate? Or does the culture of incumbency run too deep? And how can they survive if they won’t?

5 May 2016 -

ANZ’s new ‘centre of the future’ in Sydney is part of a shift in the banking sector to bring digital into the branch for both staff and customers, ANZ Group Executive Australia Fred Ohlsson says.

12 May 2016 -

Imagine being able to make real-time data rich payments easily and quickly, any time, any place. This is the future with NPP in Australia.

13 May 2016