-

The global economy continues to splutter with the International Monetary Fund once again downgrading its outlook (although still expecting growth) and a swarm of central banks expressing similarly gloomy views.

" In the short term then it is 'risk on' – which if sustained would turn around the dismal cross-border financing data."

Andrew Cornell, BlueNotes managing editorEconomists and policymakers continue to debate the technical issues, such as quantitative easing of monetary policy, negative interest rates and other unorthodox measures.

But behind these official downgrades in aggregate growth, more detail is starting to emerge of the factors behind it and where the impacts are hitting hardest. And whether there’s any blue sky appearing.

The latest Bank for International Settlements (BIS) review, for the December quarter and year, showed the slowdown in cross-border banking activity that began in early 2015 broadened in the final quarter of the year.

“Whereas in Q3 2015 this slowdown was most pronounced for interbank activity and lending to emerging market economies (EMEs), in Q4 2015 it spread across sectors, major currencies and regions,” the BIS said.

“Cross-border bank credit to EMEs in aggregate contracted by 8 per cent in the year to end-December 2015, the largest annual rate of contraction since 2009. Claims on China fell by $US114 billion, the largest drop during the quarter.”

This is not just a story about banks, it is a story about the economies to which they lend.

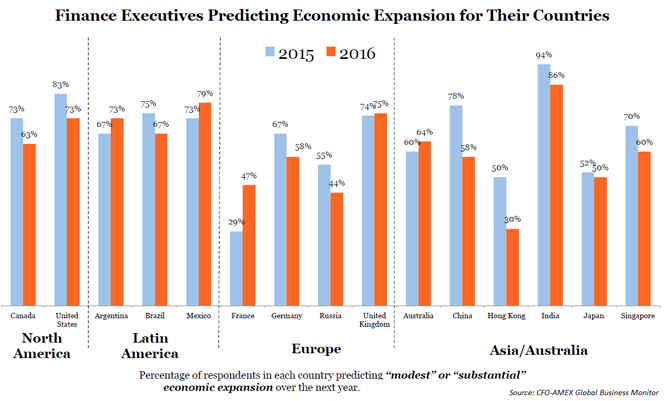

But equally such data show what has happened. For a prospective outlook, American Express surveys global chief financial officers in its annual American Express/CFO Global Business and Spending Monitor.

According to the recent survey, finance executives overall remain cautious around spending and investment decisions due to global economic and political uncertainty. But not without hope.

That echoes IMF and other data however the underlying story is more nuanced and regionally disparate.

According to the survey, in aggregate “caution is not necessarily translating into lower spending and investment. It is motivating companies to reduce exposure by focusing more on domestic markets and increasing investment in risk management and security”.

The United States is particularly buoyant with three quarters of respondents (75 per cent) reporting revenue growth over the past year, the highest of any country. In addition, at 73 per cent expect continued economic expansion next year – again the most optimistic.

That contrasted with Latin America where overall growth was anaemic although respondents were still optimistic and planning to spend and invest.

More concerning was Asia, still the engine room of growth and one – relatively – healthy region in the IMF outlook.

Yet according to the Amex survey, respondents from the Asia/Australia region “continue a multi-year trend of lowering expectations for their economies - primarily due to declines in China and Hong Kong.”

The outlook in Europe is neither here nor there.

The insight from the Amex survey into cross-border lending is telling. The most common response from CFOs to uncertainty will be to pull back and focus on domestic markets. In answer to the question “over the next year, is economic or political uncertainty, whether in your country or in other countries, likely to cause your company to take any of the following actions?” the most common response, from 41 per cent, was “increase our focus on domestic markets”.

That was followed by “increase our investment in risk management or security” (39 per cent) and “redirect planned investments from some countries to different countries” (31 per cent).

{CF_IMAGE}

But even the regional trends are not uniform. “Compared to last year, the US, Japan, and Australia clearly have become more aggressive, while others just as clearly are pulling back,” Amex said. “In particular, companies in Latin America and Europe, along with those in Canada, are more cautious than last year.”

Given the global climate, it is almost a case of the closer you look, the more blurry the picture.

Against the bleakness of the BIS work, the last couple of weekly emerging market insights from the Institute of International Finance have been positively frothy: “party time” in the IIF’s phrase.

“Ebullient oil and commodities continue to boost EMs: Rising oil prices (up over 20 per cent from early April lows) continue to set the rhythm, with the market shrugging off OPEC's failure at their Doha meeting to agree on a production freeze,” the IIF said.

“Steady improvement in the economic data from China, where the economic surprise index is at its highest in over a year, has fed into a sharp pickup in non-energy commodity prices too - up over 8 per cent in the past two weeks. EM equities have pretty much followed suit, while EM bonds, up 2 per cent over the same period, are at their highest level since last May.”

In the short term then it is “risk on” – which if sustained would turn around the dismal cross border financing data.

While the BIS data response may well be “we’ll believe it when we see it”, the evidence from the last banking activity review does actually suggest such a more positive trend is possible – reading between the lines.

“The decline in cross-border lending was more widely spread across sectors, major currencies and regions in Q4 2015 than in previous quarters,” as the BIS says.

“As regards sectors, interbank activity again accounted for the largest share of the quarterly drop. But claims on non-bank borrowers, which had previously held up better than interbank activity, also fell substantially (by $US167 billion): their annual growth rate slowed to 2 per cent at end-December 2015, down from a peak of 10 per cent at end-March 2015.”

So far, so bad. But: “As regards currencies, cross-border claims denominated in euros fell the most ($US324 billion), followed by those in US dollars ($US185 billion). By contrast, cross-border claims denominated in Japanese yen rose slightly, by $US30 billion during Q4 2015.”

That is, the aggregate data doesn’t well capture how fragmented and regionally disparate outlooks are.

The more forward looking Amex survey and improved confidence in the IIF reports of the last two week are at least potentially encouraging. There is however still no indication of a robust, sustained global recovery.

Andrew Cornell is managing editor at BlueNotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

EDITOR'S PICKS

-

World trade is now growing at about half the rate it did before the global financial crisis. On viewing the data several questions immediately spring to mind.

24 March 2016 -

Banks are leveraged plays on economies because they lend their capital many times over. So when economies are strong, banks perform even more strongly.

5 April 2016 -

Death is difficult to talk about. Even the quality media, which have long prided themselves on clarity and simple language, now regularly refer to “passing” rather than dying. There’re more euphemisms for dropping off the twig today than even Monty Python could cope with.

19 April 2016