-

The ructions in China have inevitably shifted thinking around the role of China's currency, the renminbi (RMB). While China's stated long term aim is opening up its economy and internationalising the RMB, market turmoil and growth concerns have created new uncertainty.

" Trade flow between China and its region are increasingly occurring in RMB."

Andrew Cornell, Managing Editor, BlueNotesIndeed, the reaction of the Chinese government to the market volatility has led to a wave of speculation more regulation looms and the internationalisation of the currency may be put on hold.

But the evidence tells a different story with consistent steps towards a greater role for the RMB - even if those steps are not the headline grabbing leaps like the inclusion of the Chinese currency in the International Monetary Fund's international basket of currencies.

Take two key examples: the RMB is increasingly important in regional trade flows while the Chinese central bank, the People's Bank of China, has just made it easier for foreign issuers of debt and foreign investors to participate in the Chinese bond market.

Both of these developments contribute to the “deepening” of the Chinese financial system which ANZ's Caged Tiger: “The Transformation of the Asian Financial System" report argued was essential for a more mature Chinese economy.

“Continued progress in financial reform, deregulation and opening up to global markets in Asia will be essential to support high levels of economic growth in the region,” the report said. 'China is central to this Asian Century scenario.”

Last week's step by the PBoC to give foreign investors greater access to its domestic bond market (where foreign investor holdings are currently in the single digits) is a major move to deepen the bond market. A larger investor base will also encourage more issuance of debt, further deepening the system.

While the move demonstrates liberalisation continues it should also have the more immediate impact of attracting capital into China – offsetting to some degree the capital outflows the volatility has exacerbated.

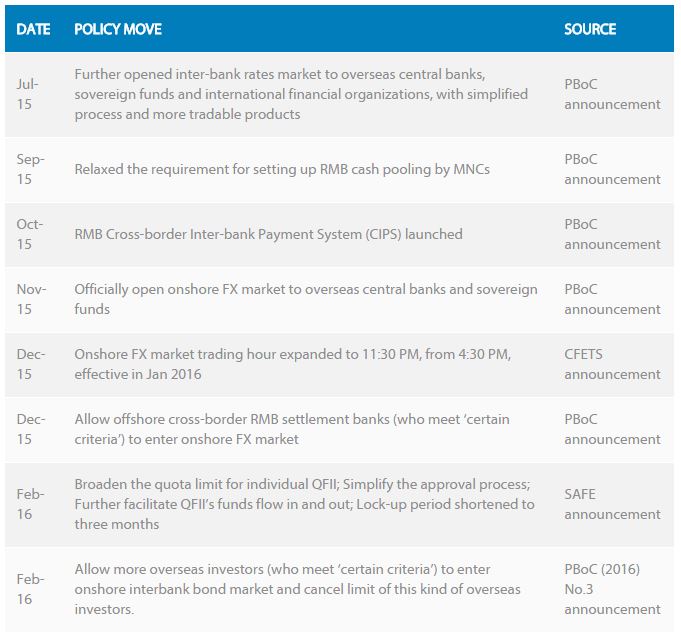

ACTIONS ON ONSHORE MARKET LIBERALISATION

{CF_IMAGE}

Meanwhile trade flow between China and its region are increasingly occurring in RMB – as you would expect as corporates and investors become more confident in the currency's more permanent global role.

"Despite volatility in China, and widely reported economic slowdown, the South-East Asian markets, such as Singapore, Thailand and Malaysia, have been enhancing RMB payment capabilities, including the establishment of RMB clearing centres,” says Michael Moon, Head of Payments, Asia-Pacific at global payments system SWIFT.

“This growth reflects the extensive trading relationships between South-East Asia and China, which continues to be very important for the region."

Bankers in the region are seeing that growing trade more broadly – and SWIFT reports greater use in the middle east too – with Korea trade another corridor using RMB more intensively.

For example, SWIFT data shows Malaysia's use of the RMB for payments with Mainland China and Hong Kong increased by 68 per cent over the last 12 months and by 214 per cent over the last three years. Since January 2013, the Chinese currency moved from position number three to position number two for payments by value, overtaking the Malaysian Ringgit.

{CF_IMAGE}

The opening of the bond market is potentially even more significant as it should help grow a critical financing market in China while raising demand for the Chinese currency and attracting capital back.

According to ANZ Research, “following the scheme to allow foreign central banks, supranational and sovereign wealth funds to invest in the interbank bond market last summer, China's (new) move to allow other foreign institutional investors access as well is a significant step in China's financial sector reforms”.

“Not only are more foreign investors given access but the process is being simplified and there will no longer be any quota limits.”

This comes on top of other actions the PBoC has been taking to stem capital outflows as well and reduce speculation in the currency, including cross border pooling restrictions and reserve requirement for deposits from offshore entities.

Looking at interest rates onshore and offshore for Chinese currency assets, known as CNH and CNY, FX rates are pretty close which suggests Chinese regulators have been largely successful in removing arbitrage from the CNY/CNH market.

Moreover, three foreign banks were banned from cross-border FX trading for three months which also sent a pretty strong message to the market.

Of course the liberalisation project remains delicate. China is a huge economy balancing a history of state control with an economy in transition and a desire to more closely integrate with liberalised global markets.

While China is yet to give up exchange rate control – particularly with recent capital outflow pressure - capital reform needs to continue as ultimately that will help deliver a more flexible exchange rate regime.

The bond market reform in particular should help balance inflows and outflows. It is estimated the move will see an estimated $US3 trillion flow into the country, helping to support the currency.

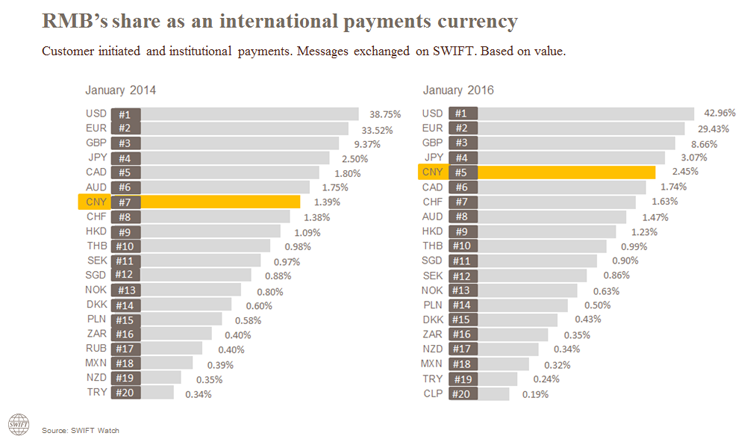

According to SWIFT, in January 2016, the RMB was the fifth most active currency for global payments by value and accounted for 2.45 per cent of global payments, a slight increase from 2.31 per cent in December 2015. Its activity share is higher than last month even though RMB payments decreased by 5.7 per cent in value, while at a global level, all currencies decreased by 11.2 per cent in value over the same period.

{CF_IMAGE}

The greater use of RMB in trade flows should grow as intra-Asian trade grows – it has never been logical to use a third country currency like the greenback however until the RMB began to internationalise, there was no real alternative. (Even the Japanese Yen in the Japanese heyday never assumed that role.)

Australia and New Zealand are actually a bit of an outlier in this regard although there is certainly pressure for those bulk commodities historically priced in USD to be shifted to RMB for China trade.

Plenty of challenges remain. As the RMB has weakened, credit ratings onshore are largely meaningless and ongoing intervention in the FX and equity markets will keep investors nervous. While limitations on outflows may make investors cautious on how they can exit positions and repatriate offshore.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

Share

anzcomau:Bluenotes/asia-pacific-region,anzcomau:Bluenotes/asia-pacific-region/currency

Despite volatility, China policy continues to support growing internationalisation of the RMB

2016-03-01

/content/dam/anzcomau/bluenotes/images/articles/2016/February/rmb-int-payment-thumb.jpg

EDITOR'S PICKS

-

It now appears inevitable China's currency the renminbi (RMB) will be included in the International Monetary Fund's (IMF) Special Drawing Rights (SDR) basket when the IMF Executive Board meets next week.

27 November 2015 -

The Chinese central bank's recent actions have sent a strong message to those looking to short sell the Chinese currency: don't.

27 January 2016 -

The Chinese central bank's surprise decision to fix the Renminbi (RMB) below its last closing price serves as a statement on softening monetary policy which will place more pressure on the country's already heavily sold equity market.

7 January 2016