-

While most eyes are focussed on the macroeconomic imbalance causing pushing oil prices below $US40 a barrel, elsewhere the real crisis for oil is accelerating with the adoption of autonomous electric vehicles.

" As hybrids become cheaper, all-electric vehicles and the infrastructure to support them becomes viable."

Alex Kewley, Director, Client Insights & Solutions, ANZIn November, I wrote on the biggest trends reshaping the automotive industry, covering key pressures and what the sector might look like in 2030 and beyond. One topic not covered in depth is what it all means for oil. Spoiler alert: it's bad.

LESS THAN 1 PER CENT

There are currently over one billion petrol driven vehicles globally and roughly 45 per cent of all barrel oil powers them.

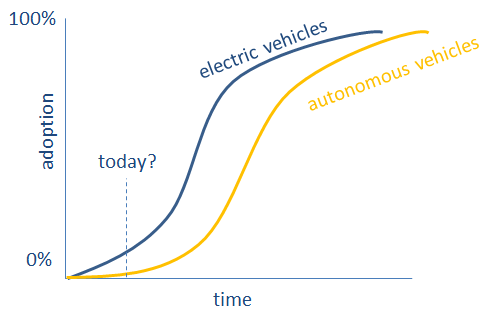

The US and China are the world's largest car markets and in 2015 less than 1 per cent of cars on the road in the US and China were electric. However, adoption rates have been staggering.

Compared with2013, this sub-1 per cent share still represents a 130 per cent increase in in the US, and 800 per cent increase in China. Even in some of the fastest automotive growth markets – China, India and ASEAN – which are still inclined to buy petrol cars today, the infrastructure is growing and the culture leaning towards it.

Even this growth is a snapshot taken at the hockey stick point of the S-curve (a typical technology adoption model) - that is, at a point of least impact before a surge.

As hybrids become cheaper, all-electric vehicles and the infrastructure to support them becomes viable. As hydrogen and other technologies come online, the sensibility gap to petrol engines will widen further.

This accelerated adoption is also compounded by global regulatory pressure and incentives and a crisis of confidence in diesel which spread from a brand-specific issue to another nail in the coffin for combustion.

OPEC expects just 5 per cent of vehicles will be all electric by 2040. This is seems a ludicrous assertion when auto and tech firms are investing billions in all electric autonomous vehicles today. Norway alone is already at 22 per cent.

Either OPEC is wrong or Google and the entire auto supply chain will be bust by 2040. I know which side I would back.

Furthermore, not only will vehicles be less reliant on petrol, there will be less of them. The average use of a vehicle is around 30 minutes a day. There are almost no examples elsewhere of such underutilised assets.

The inevitable transition to shared autonomous vehicles means optimal allocation of out-of -use vehicles.

Many of us will use a car when we need one rather than own it - be it the Zipcar borrow-on-demand model or, taken to the extreme, shared autonomous vehicles which know where you are going without asking (and may not even ask you to pay). Even haulage and delivery will be autonomous drones on land and in air.

The combination of hybrid technology and Uber gives us a glimpse into the possibility. In just over 10 years, the Toyota Prius has gone from an oddball celebrity vehicle which Toyota was losing money on, to being the fastest selling used car in Britain today, and ubiquitous choice for pay-as-you-go shared transport (a.k.a. Uber).

Extrapolate to this pay-as-you-go shared infrastructure being the default, and all-electric rather than hybrid, and you have a real demand crisis for oil.

DEMAND CRISIS

In 2014 around three billion barrels of oil were consumed in the US. Let's imagine in 2030 we have a 20 per cent market share of electric vehicles, and further 30 per cent hybrid. Even ignoring other drags on oil, and conservatively assuming five barrels a year consumed by a petrol vehicle, that could mean up to half a billion less barrels consumed per year in the US alone.

Ultimately there are many complex drivers for oil demand - and the price could be supported by lower production. However, without question it will be a commodity less in demand.

I would speculate on that basis that

we could see levels around the current mark for the long run, and the supply side needs to structurally adjust for the long term.

"Thirty years from now there will be a huge amount of oil - and no buyers. Oil will be left in the ground. The Stone Age came to an end, not because we had a lack of stones, and the oil age will come to an end not because we have a lack of oil."

Sheik Ahmed Zaki Yamani, June 2000, former Saudi oil minister.

The new normal for transport means a new normal for oil. The danger is no longer one of running out of oil, but running out of a need for it.

In which case, the crisis in fact spreads, and the challenge becomes as much macroeconomic and geopolitical as environmental given the implications for country trade flows and job losses in the industries affected.

Alex Kewley CFA is Director, Client Insights & Solutions at ANZ.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/global-economy/commodities,anzcomau:Bluenotes/global-economy/economics

The other impending oil crisis

2016-03-31

/content/dam/anzcomau/bluenotes/images/articles/2016/March/real-oil-crisis-aev-chart-thumb.jpg

EDITOR'S PICKS

-

World trade is now growing at about half the rate it did before the global financial crisis. On viewing the data several questions immediately spring to mind.

24 March 2016 -

Japan has entered its third “lost decade" of economic malaise following the collapse of its bubble economy in the early 90s.

30 March 2016 -

Remember the days when newspapers and TV decided what was news and consumers responded accordingly? Just as the news value chain splintered into a world where people create and share media, the food industry also confronts a changing landscape.

21 March 2016