-

Positive sentiment has crept back into iron ore markets amid weaker-than-expected export data from Australia and expectations of Chinese restocking. Our advice is not to get too excited - we still believe China will destock in the post-Lunar New Year period as proposed steel capacity cuts are delayed.

With support from stronger Chinese prices unlikely to eventuate, iron ore therefore is susceptible to further weakness. With risks still heavily skewed to the downside, we expect to see prices below $US40 a tonne in the coming months.

" While there has been chatter about potential restocking after Chinese New Year, evidence suggests the likelihood of such a scenario is low."

Daniel Hynes, Senior commodity strategist at ANZSeasonal trends post-Lunar New Year do not support higher prices. While there has been chatter about potential restocking after the holiday, evidence suggests the likelihood of such a scenario is low.

{CF_IMAGE}

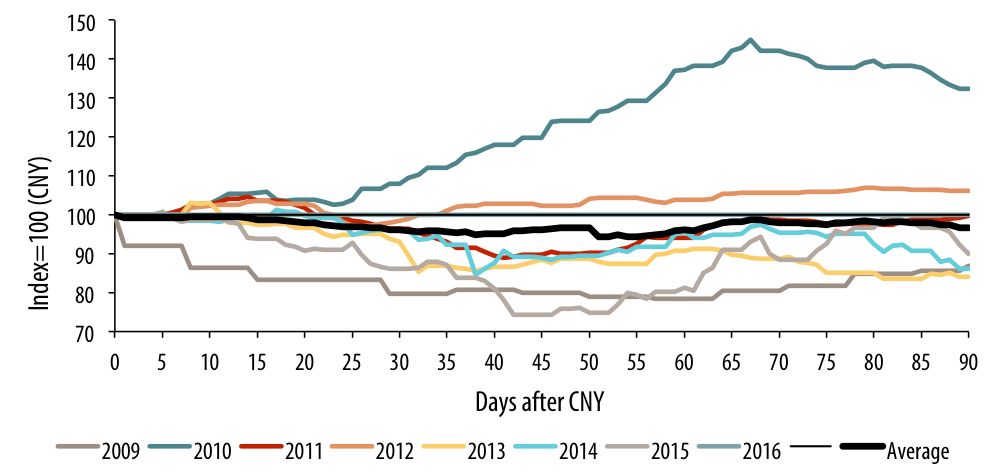

Chinese steel production has traditionally been a little bit stronger in the months following the Chinese New Year holiday. Discounting the month after the holiday, growth in steel production has been relatively modest.

Even so, this hasn't resulted in a similarly consistent pick-up in iron ore demand. While the second month following the holiday has seen (on average) a pick-up in imports over the past 10 years, this quickly turned around in later months. A consistent build in inventories late in 2015 also makes the likelihood of a restock unlikely.

{CF_IMAGE}

Therefore, it should not come as a surprise prices have continually disappointed post New Year. Outside of 2010, iron ore prices have fallen every year one month after the Chinese New Year. And in all cases bar 2010 and 2012, prices have still been lower than before the Chinese New Year some 90 days later.

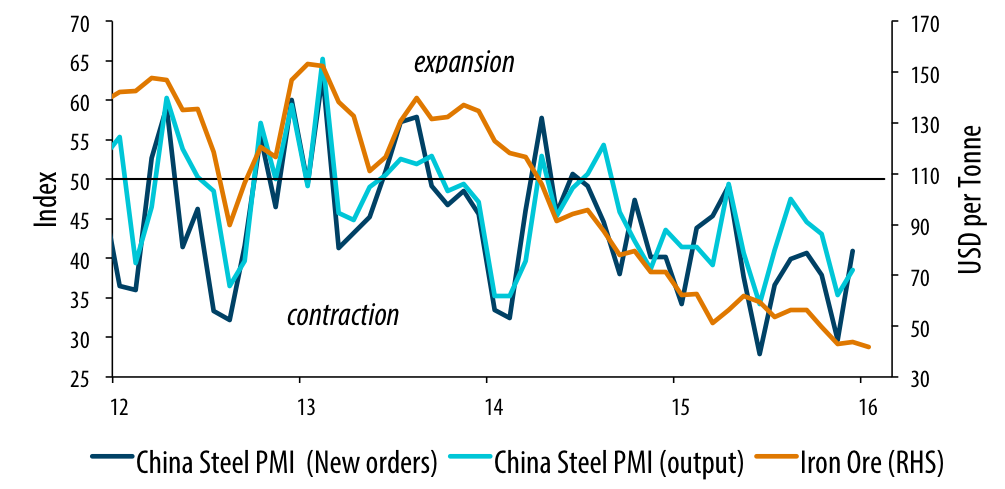

China's State Council announced earlier this year it will reduce steel production capacity by 100 million tonnes to just 150. This follows on from a reduction of more than 90 million tonnes between 2011 and 2015.

{CF_IMAGE}

This continues to be reflected in the Chinese steel PMI. While it recorded a small gain in December 2015, it presently remains in contracting territory at 40.6. The new order and output subsectors also remain weak, with both well below 50.

Daniel Hynes is a senior commodity strategist at ANZ.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/global-economy/commodities,anzcomau:Bluenotes/global-economy/economics

No, China will not save iron ore

2017-02-16

/content/dam/anzcomau/bluenotes/images/articles/2016/February/iron-ore-banner2.jpg

EDITOR'S PICKS

-

Successful multiculturalism is obviously a lot more than a taste for foreign spices.

10 March 2015 -

The economic world is a different place today than it was just a few weeks ago. Fundamentals remain steady but ructions on Chinese markets, Wall St and a New Year's offering of bleak news has a lot of people on edge.

21 January 2016 -

“For last year's words belong to last year's language And next year's words await another voice". - “Little Gidding", TS ELIOT

11 January 2016