-

It now appears inevitable China's currency the renminbi (RMB) will be included in the International Monetary Fund's (IMF) Special Drawing Rights (SDR) basket when the IMF Executive Board meets next week.

The plethora of acronyms aside, is this a non-event or something more substantial?

"The effects [the RMB's SDR] inclusion is more likely to be gradual rather than immediate but a range of implications and opportunities will clearly emerge."

Daniel Everett, Global Head of RMB, Strategy and Execution at ANZThe IMF says the RMB now “…meets the requirements to be 'freely usable' and…proposes the Executive Board…include it in the SDR basket as a fifth currency". It is expected to ratify this determination when it meets on November 30.

China's push for the RMB to be included in the SDR alongside the USD, GBP, EUR and JPY has received substantial media attention and a range of conflicting views but at the end of the day the question is whether it will really change the landscape for the RMB.

The short answer is a resounding “yes". It is clearly a very important step forward and will signal a number of key changes over time for the RMB, increasing its growing integration and importance to the global financial system.

The effects of inclusion are more likely to be gradual rather than immediate but a range of implications and opportunities will clearly emerge.

Right off the bat, including the RMB in the SDR basket is a big show of support by the IMF for the currency as a reserve asset and is also a vote of confidence in China's ongoing reform program.

This in itself places the RMB in a very elite group of currencies. While the concept of the SDR is not well understood, it is best to focus on what inclusion symbolises and what flow on effects will come over time, rather than on its use in the actual SDR basket.

CENTRAL BANK BIAS

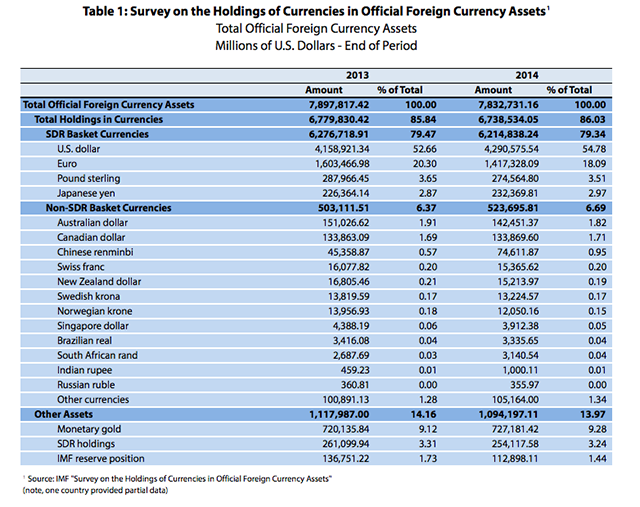

At present, almost 80 per cent of global reserves (including gold and other assets) are held in the four SDR currencies so clearly there is a bias by central banks worldwide to hold SDR currencies.

Interestingly, according to an IMF survey conducted earlier this year, during 2014 central bank RMB reserves increased from $US45.4 billion to $US74.6 billion (64 per cent growth) which was the largest dollar-value increase in any currency aside from the USD .

So even if we ignore SDR inclusion, RMB is becoming increasingly important to global central banks as a reserve asset.

{CF_IMAGE}

It is unlikely central banks will automatically benchmark their reserve holdings to the RMB's weight in the SDR (they don't for other SDR currencies), however it appears certain RMB reserve allocations will increase as a result of its newly minted reserve status.

How big could the switch be? At present, the RMB accounts for just less than 1 per cent of global foreign currency reserve assets. Assuming this weighting moves to around 4 per cent, global RMB reserves could swell by as much as $US230 billion according to ANZ Research.

This will promote greater demand, liquidity and turnover in RMB with resulting benefits to corporates and investors using the market for their hedging and investing activities.

Another beneficiary from SDR inclusion is likely to be China's onshore bond market. Already the third largest in the world at around $US5.5 trillion, it has very low foreign ownership (less than 2 per cent) due to controls around market access and a largely closed capital account.

However, in July this year Chinese authorities announced central banks and sovereign wealth funds now need only preregister to access China's bond market and were free to do so without a quota. This change has made it much simpler for central banks to increase RMB reserve holdings in Chinese bonds, a key pre-requisite for any reserve currency.

Increasing demand over time for Chinese bonds will likely see growth in new bond issuers, new investors and will likely see significant growth in the market's size, diversification and liquidity.

At present, China's GDP is roughly 13 per cent of global GDP yet its bond market is around 5 per cent of the global bond market.

This is clearly set to change and presents enormous opportunities for investors and issuers over the next few years, particularly as yields on RMB still exceed those of the other SDR currencies.

BALANCE REQUIRED

This forecast growth in the bond market, however, will need to be balanced with a need for greater transparency, a more robust credit framework, stronger corporate governance as well as improved and differentiated pricing for risk.

SDR inclusion will also see downstream impacts as well. A resulting growth in two-way liquidity in RMB and recent policy changes by the People's Bank of China to theoretically allow the RMB spot price be more market driven (key to SDR inclusion as well), will have flow on effects for corporates and investors.

A currency which is liquid and with more pronounced market driven two-way volatility will compel many Chinese corporates to favour RMB invoicing and borrowing for more prudent risk management.

China's offshore trading partners can therefore expect to see continued growth in RMB trade. In addition, the likely corresponding increase in use of hedging products (such as FX forwards and options) will allow the RMB derivatives market to grow in size and liquidity both offshore and onshore.

A greater overall use of the RMB by businesses and the continuing relaxation of capital controls around cross-border financing will give regional treasury centres unprecedented flexibility around their use of RMB in their global cash pools and improved flexibility in hedging RMB related exposures.

In short, this is quite a big deal and the first time the SDR basket has changed since 1999. This isn't about the SDR itself but rather what SDR inclusion means more broadly to global markets and how RMB usage will likely evolve moving forward.

The RMB is continuing its rapid ascension and SDR inclusion is another important milestone to trigger increased acceptance and global flows in RMB.

Daniel Everett Global Head of RMB, Strategy and Execution at ANZ

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/business-finance

RMB reserves place among the elite

2015-11-27

EDITOR'S PICKS

-

When the IMF said late last month it would review to consider adding China's RMB into its Special Drawing Rights basket it became pretty clear we have reached another inflexion point in China's currency story.

10 June 2015 -

In an upcoming special report The Renminbi Takes Centre Stage, ANZ will provide insights on the evolution of the RMB into an international trading currency. In a special preview, exclusively on BlueNotes, the infographic below demonstrates the RMB journey so far.

1 June 2015 -

I have many conversations about the renminbi (RMB) yet I almost never walk away without some new insight, perspective or appreciation of the opportunity emerging as China liberalises its currency and financial markets.

15 July 2015