-

The investor-focussed traditional weekend media in Australia did a thorough go over of the implications of the Reserve Bank’s somewhat surprising decisions to cut the overnight cash rate 25 basis points last week.

The broad themes of the coverage were what strategies fixed interest investors like retirees should adopt and, given everyone wants yield assets to make up for the drop in official rates, where should money go?

"International investors are now back in the frame following a period of selling."

Andrew Cornell, Managing EditorAustralian banks, because they are stable and pay relatively high dividends, are an obvious choice - leading into another popular theme: will Commonwealth Bank of Australia beat CSL (a blood plasma specialist) or Cochlear (hearing technology) to one hundred bucks a share (Aussie)?

Given the skyrocket under banks share prices in Australia when the RBA announced, CBA would seem a good bet.

But there are more moving parts to this than Australian retirees’ search for yield (and fully franked dividends, an edge CBA has over those other stocks approaching their ton).

For one, international investors are now back in the frame following a period of selling when the Australian dollar began its dive against the Greenback a year or so ago. That’s potentially good for Australian stocks and bank shares.

On the downside, the international banking regulators in Basel once again reminded investors they were looking at capital levels very seriously and hence returns on shareholder funds will come under pressure.

The currency theme has been treated a bit marginally but it is potentially a major swing factor for continued strength in stocks. A morning note by Macquarie last week did a good job pointing out an Australian currency now seemingly lodged under US80c makes Australian equities attractive. Foreign shareholdings in Australian banks range between 20 and 30 per cent.

When the Aussie was falling from $US1.10, foreign investors were losing money even if $A prices were stable. The risk of further capital losses on the $A value is now much lower.

Meanwhile the sharp run up this year and late last year in Australian major bank share prices in $A terms means some local investors have an incentive to sell to balance portfolios and take profits.

Macquarie’s trading desk reckoned offshore exposure to Australian equities was probably at its lowest for two decades but at current currency levels interest is returning – particularly in financial stocks. Given US stocks, thanks to that economy improving and the US currency rising, are becoming expensive. Europe is still on the nose. So Macquarie argues foreign investor interest in Australia could be at an inflexion point.

Will domestic Australian bank investors be tempted to sell shares? Yes, they are at the top end of valuations and their combined market capitalisation would unbalance many balanced portfolios. But investors have been burnt recently selling major bank shares on valuations as stocks have rallied again.

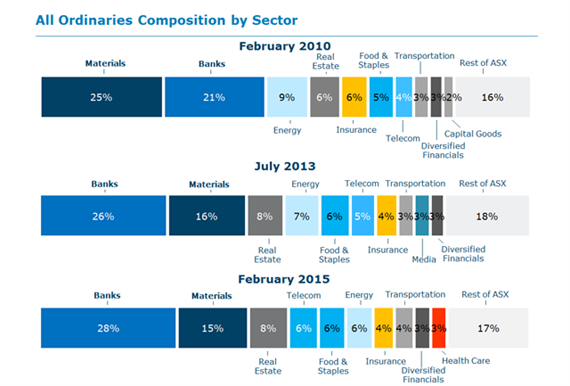

Just as rates like the 10 year government bond hit historic lows, other fascinating market dynamics are coming into play. ANZ research shows banks have moved from being around 23 per cent of the value of the market before the financial crisis to around 28 per cent now – largely as the value of the big miners has decreased.

Couple that with the amount of money coming into global funds which focus on yield via the money printing of central banks and there is something of a positive feedback loop emerging: funds buy on index weights, weights go up, funds buy more.

The domestic yield differential though is fundamental. Commentators suggest the differential between the yield on ordinary deposits and bank dividends (apart from during the acute phase of the financial crisis) is historically high. When term deposits are less than 3 per cent and grossed up dividend yields double that, it’s pretty enticing.

More technically, some analysts are starting to lower what is considered the “risk free rate”, a forecast of what supposedly risk free government bonds will average over the next decade. Given markets value yield as a measure of risk, lowering the risk free rate equates to a higher return for the same risk. Again, fuel for share prices.

CLSA bank analyst Brian Johnson ran through the rate cut ramifications in a note citing six factors. The key ones were banks picking up margin on term deposits (where prices paid for deposits lag the cost benefit of official rates coming down), credit losses staying low due to subdued credit demand (one of the reasons the RBA cut) and low financing costs, foreign investors coming in and the dividend yield story.

So net-net a good story for bank share prices.

But what of the downside? Bank investors last week conveniently forgot the debate over bank capital levels, mandated by the G20 and the various Basel-based regulators (and geed on in Australia by the Financial System Inquiry recommendations) is still alive.

On Friday ratings agency Standard & Poor’s warned moves to implement formal rescue plans for banks deemed too-big-to-fail would likely lead to ratings downgrades for major American and European banks.

“We expect to place our long-term ratings on the (holding companies) of the eight US G-SIBs on CreditWatch with negative implications once we believe that US authorities have made sufficient progress towards implementing an actionable resolution plan,” S&P said.

The warning related to northern hemisphere banks and so-called globally systemically important banks (G-SIBS) but just because Australian banks are not G-SIBS they are not unaffected.

Early Saturday morning Australian time the Basel-based Financial Stability Board published submissions made on the subject of total loss absorbing capital (TLAC), the first wall of defence for a failing bank.

The Australian Bankers’ Association was a notable submitter. The ABA began its submission by doffing its cap to the global agenda. But it warned there were significant consequences for the Australian banking system if TLAC translated to more core capital – one of which, although the ABA didn’t mention it, would be a hit to bank shares.

“The ABA agrees with a key sentiment of the TLAC proposals that (improved stability) can be done through mechanisms other than holding further Common Equity Tier 1 (CET1) capital,” the submission said. “The broader definition of TLAC strikes an appropriate balance between ensuring stability while not adding significant cost which would be passed onto bank customers.”

Acknowledging the Australian banks are not G-SIBs and therefore the TLAC proposals are not intended to directly apply to them, the ABA argued “the proposals and the consequential increase in capital levels will affect all banks which compete for capital and funding in international markets”.

It added the FSI had emphasised Australia should follow international rules.

Bank stock investors in the run up to the Murray FSI report did have a bit of a heart flutter around fears of more capital, which with hindsight didn’t really lie in the inquiry’s domain, but they now seem almost blasé about the more clear and present work on capital in Basel.

The yield on bank stocks is very attractive. There are no present signs of operational dangers like higher bad debts. Official rates are now forecast to go lower. But the market in general and retail investors in particular having been dancing the bank dividend tango for quite a while now but there’s no indication the band will take a break.

Those overweight banks may well be contemplating the immortal lines of – former – Citigroup chief executive Chuck Prince: “As long as the music is playing, you've got to get up and dance.” Then the music stopped.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

Share

anzcomau:Bluenotes/business-finance,anzcomau:Bluenotes/business-finance/banking

Do rate cuts mean full steam ahead for Aussie bank shares?

2015-02-10

/content/dam/anzcomau/bluenotes/images/articles/2015/February/Basel_banner.png