-

After several years of losing share to debit cards – reflecting more cautious consumers – the data for 2014 have shown credit cards are back in vogue. But not the credit card of old.

Consumers are still reluctant to take on debt hence they are maintaining lower balances and paying less interest on “revolving” debt – that is debt not paid off each cycle.

"[Payment cards have increased their] hold on the market despite minimal stimulation from external economic and business drivers."

Mike Ebstein, Founder and principal of MWE ConsultingThe real difference in credit card usage in 2014 has been the amazing take up of new “tap-n-go” point of sale technology where credit cards – more typically used in high value transactions – can be used for a coffee or newspaper (if anyone still buys them).

Overall, credit and debit card spending maintained momentum in 2014 despite minimal stimulation from external economic and business drivers.

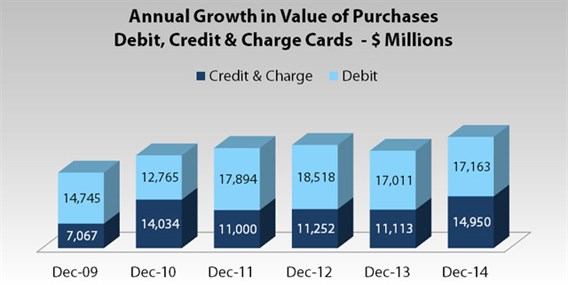

The growth in card spending rose to its highest point in five years in 2014, according to data from Reserve Bank of Australia, on the back of a strong increase in credit card use.

The increase in debit card spend has been quite consistent in recent years with greater volatility being seen in the credit and charge card market. This reflects the wider use of credit and charge cards for discretionary spending, compared with debit which is used more for routine spending.

{CF_IMAGE}

Using estimates for the month of December 2014, there was a considerable lift in the annual growth in credit and charge card spend in 2014 over 2013, with the overall lift in annual card spending exceeding $32 billion.

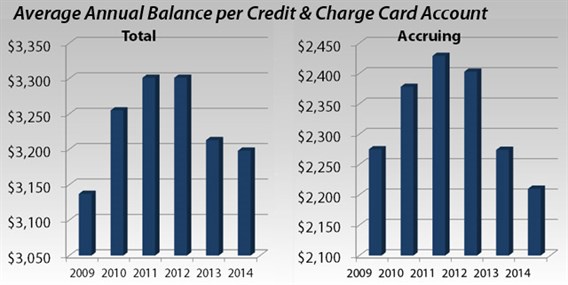

Underlying changes in cardholder behaviour continued to alter the payment card dynamics. Despite sound growth in card spending, an aversion to debt maintained a lid on card balances.

Although the slide in average balances was largely addressed in 2014, the balances on which interest was being paid continued to fall. Credit card spending is less likely to contribute to growth in balances and card balances themselves are less likely to be earning interest for the card issuers.

{CF_IMAGE}

However, average credit card balances contracted in the year to May 2014. A number of factors led to this contraction, the first time it has been seen since records commenced in 1985.

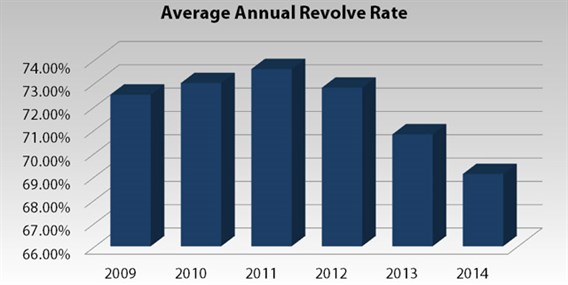

Whilst cardholders were expanding their use of cards (through drivers such as tap-and-go and online) an underlying softness in consumer sentiment delivered rates of card debt repayment that were high by historical standards.

In addition, competition between card issuers in a market that was offering a shrinking number of new accounts led to offers of low and zero rates on balance transfers and new purchases.

The impact on the revolve rate has been considerable. The proportion of total balances on which interest was being paid exceeded 73 per cent in 2011. It then started to decline and in 2014 fell to 69 per cent, its lowest point on record.

{CF_IMAGE}

A significant trend though is the replacement of cash by cards. Cash has traditionally been the payment method choice in the low-value arena, particularly up to $20. It has been in this lower-value segment where tap and go technology has delivered benefits to cardholders and to merchants with a very much faster and simplified experience at point of sale.

One result has been a decline in the average value of a purchase made with a personal credit card from over $131 five years ago to less than $120 in 2014.

Statistical data released by the RBA in January 2015 shows tap-and-go transactions accounted for 23 per cent of the number of card transactions in 2013, with swiped or inserted credit cards at 37 per cent and swiped or inserted debit at 41 per cent.

The figures were higher for supermarkets where tap and go was at 28 per cent and at petrol retailers where it was 26 per cent.

Unsurprisingly, given tap and go targets transactions under $100, the median transaction value for tap and go at $26 is lower than for transactions where the card is swiped or inserted with credit at $45 and debit at $32.

The one exception is at petrol retailers where the median tap and go value of $50 just exceeds swiped or inserted credit at $49 and debit at $40.

The displacement of cash by cards has been considerable. The withdrawal of cash at ATMs is a good indicator of cash use and we see the annual total value of cash transactions per debit and credit card combined has dropped by 25 per cent over the last five years. In 2009, the total exceeded $6,400 per cardholder but that had dropped to below $4,800 in 2014.

{CF_IMAGE}

The migration from cash to cards was most recently quantified in the RBA’s 2014 paper, “The Changing Way We Pay: Trends in Consumer Payments.”

At a top level, this report showed between 2007 and 2013 cash declined from 69 per cent to 47 per cent of the volume of consumer payments whilst cards increased from 26 per cent to 43 per cent. Cash accounted for a little under half of the volume of payments.

Between 2007 and 2013, cash declined from 38 per cent to 18 per cent of value whilst cards grew from 43 per cent to 53 per cent of value.

Payments made in person represent the great majority of consumer payments at 84 per cent but these make up just 50 per cent of the value.

There are a large number of low-value transactions at point of sale but half of the total value now occurs via the internet, with smartphones at 2 per cent, telephones at 5 per cent and mail at just 1 per cent.

Technology has facilitated a significant change in the composition and nature of payments but this is not the entire story. Convenience, security and confidence are all powerful influences in determining consumer spend and payment patterns. Cards appear to be continuing to fit the bill.

Mike Ebstein is founder and principal of MWE Consulting, a specialist payment card, loyalty and reward scheme consultancy. He has nearly three decades experience in the payments business and consults to major banks and retailers.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

-

-

Share

EDITOR'S PICKS

-

The recently forged New Payments Platform, with 12 financial institutions signed up to take part, will change the way Australia does business. With the ability to receive real time payment confirmation, businesses and individuals will have greater confidence to exchange.

9 December 2014 -

As Australian – and global – reforms of payments systems have demonstrated, they are complex networks. Complex to operate, complex to regulate, complex to forecast. But they are vital to efficient economies.

20 January 2015 -

For many, many years I have presented at payments conferences about how consumer payments are habit forming. People tend to be “locked in” to how they pay for things by the time they are 30 years old. A much stronger – not just slightly stronger - “value proposition” is needed to knock them out of their old payment habit and into something new.

14 January 2015