-

For many, many years I have presented at payments conferences about how consumer payments are habit forming. People tend to be “locked in” to how they pay for things by the time they are 30 years old. A much stronger – not just slightly stronger - “value proposition” is needed to knock them out of their old payment habit and into something new.

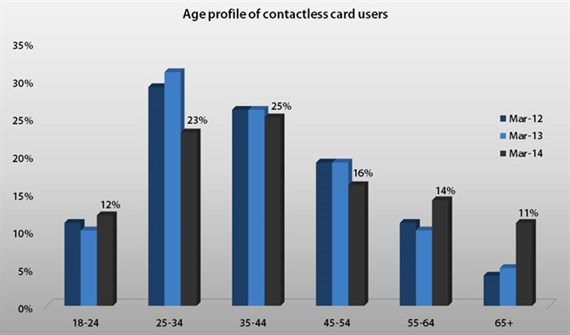

That’s not to say the way the population pays does not change over time, rather these changes usually take a long time to manifest, as shown in the chart below – in this case, 12 years.

"An interesting facet of the growth of “Tap ‘n’ PIN” is nobody has been promoting it."

Lance Blockley, Managing Director – Consulting, RFi Group

However, in card payments at least, a number of things have occurred in Australia over the last few years that have made me revisit my own habit of thinking. Firstly, the startling speed of adoption of open-loop contactless card payments by Australians, who now make more point-of-sale (POS) “Tap ‘n’ Go” transactions per cardholder than anywhere else in the world.

Following significant market preparatory work since contactless card issuance began in 2006, usage took off in 2012 with touchpads rolled out through the Coles and Woolworths store networks. Tap’n’go is not a youth phenomenon, the market segment usually the quickest to adopt new ideas, it has become an accepted way to pay across all age groups.

Secondly, the removal of signature as a form of transaction authorisation at POS on Australian issued chip cards required a change in behaviour by around eight million cardholders over a roughly two 2 year period – and this seems to have occurred with hardly any of these people noticing.

When the final move of the PIN@POS initiative occurred in the second half of October 2014, when each card issuer’s host computer system was reprogrammed to “reject” transactions not accompanied by a PIN when they should have been, there was hardly any disruption at point of sale at all. When most cardholders received a “rejection” message on the POS terminal screen, they just proceeded to enter a PIN (which they clearly knew all along) and complete the transaction.

What made the change to PIN go so smoothly? Was it Australia’s 30 year exposure to using PIN at the point of sale terminal (due to EFTPOS)? Was it that Australians are more flexible and adaptive than most; and becoming more so? Was it the great planning and communications campaigns of the issuers, acquirers and the Industry Security Initiative? Probably a combination of all of these.

But the most recent change in behaviour, which has not been pushed by the card industry at all, is the dramatic growth in “Tap ‘n’ PIN” for POS transactions over $100. This is where a contactless card transaction occurs which is above the “no authentication needed” limit of $100 and the cardholder then enters their PIN to authenticate the payment.

One of the major international schemes has reported 15 per cent of all its contactless transactions in October 2014 were for amounts over $100 - a percentage that has shot up from next to nothing just six months earlier. It appears this behaviour has been wholly driven by both cardholders and merchants themselves, who seem to have noted how quick, easy and convenient a “Tap ‘n’ PIN” transaction can be, as it avoids the need (and time) for finding the slot in the terminal in which to insert the card and then having to select between Cheque/Savings/Credit.

Both the adoption of contactless and of PIN@POS were accompanied by significant industry spend on communications programmes, using both above and below the line channels, and “hammering” cardholders and merchants with consistent and hard hitting messages.

Yet a particularly interesting facet of the growth of “Tap ‘n’ PIN” is nobody has been promoting it, it is just that cardholders and merchants have identified its benefits and changed behaviour accordingly. Tap’n’PIN has a strong but nascent value proposition discovered by the users themselves.

So maybe I need to alter my conference slides and change my own habit of talking about habit forming behaviour!

Lance Blockley, Managing Director – Consulting, RFi Group.

Chart sources: RBA Payment Statistics and HP - RFi Australian Payments research, Marc 2014.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

Share

anzcomau:Bluenotes/business-finance,anzcomau:Bluenotes/business-finance/payments

Tapping the biggest shift in consumer payments

2015-01-14

EDITOR'S PICKS

-

When is distribution like a circus act? When it’s about juggling and balancing.

3 December 2014