-

Ratings agency Moody’s Investors Service noted investment-grade 10 year corporate bond yields had, on hitting 4.42 per cent last week, reached their lowest level since 1957. Yields on the global benchmark US 30 year Treasury bonds are also at historic lows.

In the inverted world of debt capital, that means the cost of raising new debt is historically low and debt investors are paying up (driving down yields). That’s one reason debt capital issuance by banks has also hit record levels. Another, more specific, reason for banks is global regulators have demanded more conservative balance sheets since the financial crisis.

"This latest transaction shows Dim Sum is now well and truly on the menu alongside established (but less appetisingly named) US dollar and euro transactions."

Andrew Cornell, Managing EditorThat translates into more capital but also more and different subordinated bonds and other debt instruments with particular characteristics – such as conversion to equity – which regulators like.

In this climate, ANZ’s RMB2.5 billion ($A500 million) Tier 2 “dim sum” five year bond issue last week fits a pattern. It satisfies the regulatory gnomes in Switzerland as Basel III compliant and the market considered the pricing extremely favourable.

But there’re a couple of other more universally interesting facets. One is that while interest rates are low – and the European Central Bank’s shift to buy government debt implies they will stay low – markets are very volatile.

For this issue then what was critical was the spread of investors, many new to ANZ, who bought the debt. Particularly given the issue was in RMB. And that’s the other interesting point: this is further evidence of the “deepening” of Asia’s capital markets.

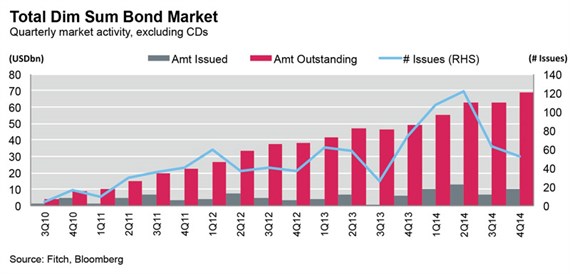

When the so-called CNH market (where organisations raise debt in the Chinese currency outside of China, nicknamed dim sum transactions) launched a few years ago, it was seen as interesting but risky. Funds raised in RMB were very hard to swap into other currencies. The market was shallow.

Although ANZ does not publicly reveal whether it does swap out of foreign currency transactions, the market is aware its first RMB issue in 2010 was not only smaller but couldn’t be swapped. Market players are in no doubt the RMB has now reached a level of maturity where swapping is straight forward.

This deepening of the Asian financial system, where more investors participate, more instruments are available, more cross border activity takes place and markets grow dramatically in size was the central argument of ANZ’s report “Caged Tiger: The Transformation of the Asian Financial System”.

Notable in this transaction was execution was entirely in Asia with investors from Hong Kong, Singapore and Taiwan. It was the first CNH Tier 2 transaction ever issued by a non-Chinese bank and largest CNH Tier 2 transaction ever issued. Almost half of the orders came from Taiwan with Hong Kong accounting for 36 per cent and Singapore 14 per cent. In terms of investor type, 53 per cent were insurance firms, 36 per cent fund managers, 7 per cent banks, 3 per cent private banks and 1 per cent hedge funds.

Pricing was also extremely competitive, not just compared with specific benchmarks but against global alternatives and investor diversification was very strong. Not only were the more than 60 investors entirely from Asia but around a quarter of them were new to ANZ.

For all issuers in the region, especially frequent, large issuers like the Australian banks, that level of new investors is remarkable and speaks directly to the deepening of the investor base in the region. Reuters said “it is the size of the deal that makes it a potential game changer, with ANZ able to raise significantly more than the three senior unsecured Dim Sum bonds from Australia's major banks”.

ANZ first issued in the RMB segment in December 2010 with a RMB200 million two-year offering and then a RMB1 billion three-year note in August 2012. National Australia Bank sold a RMB400 million two-year Dim Sum in May 2013. So both size and tenor are increasing.

A new report by ratings agency Fitch argues “the currency of China, the world’s second-largest economy, continues its ascent among global payments settlement, trade, and currency investment. Support is coming from a rapidly expanding network of offshore yuan (RMB) clearing centres, which facilitate direct access to China’s onshore financial markets”.

The Fitch report, Growing Interest in China's Currency, Debt by Matt Jamieson and Sabine Bauer, says “we expect the proliferation of these offshore clearing centres to drive greater issuance of Dim Sum Bonds (DSB) by both Chinese and non-Chinese governments, financial institutions and corporates in 2015”.

ANZ was the first foreign issuer to sell a Basel III-compliant capital instrument in RMB.

Reporting on the transaction, Reuters noted “when Aa2/AA-/AA- rated ANZ first announced the offering, most market participants had expected it would simply go through the motions to reinforce its pan-Asian credentials, but the size of the issue and the relatively tight pricing to Chinese banks raised the prospect that Dim Sum bonds could be a valuable new financing tool for foreign lenders”.

“ANZ was heard to be looking for an issue size of RMB1 billion but it easily surpassed that after garnering a RMB3.5 billion book and was also able to tighten from initial guidance of 4.875 per cent area to price at 4.75 per cent, or 82.7 basis points over one-year CNH Hibor (the low risk benchmark),” Reuters said.

In deals like this, the major factors which come into play are the rating and reputation of the issuer, the pricing and tenor of the issue and the demand from the investor base. While every deal, particularly in volatile times, is opportunistic and trends can rapidly disappear, this transaction demonstrates there’s a broader range of particularly Asian investors prepared to look at much more diverse asset classes.

(On Friday ANZ also announced a domestic Australian issue of ANZ Capital Notes 3 to raise somewhere around $A750 million. Those constitute Basel III-compliant Additional Tier 1 Capital under the Australian Prudential Regulation Authority’s (APRA) current capital adequacy standards.)

Caged Tiger argued it is this expansion of Asian markets that will be both necessary and typical as Asian financial systems catch up with broader economic growth.

“The area with the most significant growth potential is the debt markets,” the report said. “Asia currently has a relatively small bond market, but a viable alternative to bank finance needs to be developed. ANZ projects that the Asian domestic debt market (excluding Japan) could be worth around $US80 trillion by 2030 (with China accounting for over half).”

Moreover, “the RMB market will dominate in Asia not only because of the size of the Chinese economy but also because it will be a regional funding currency”.

From the perspective of banks raising debt in the region, this latest transaction shows Dim Sum is now well and truly on the menu alongside established (but less appetisingly named) US dollar and euro transactions. And the Asian financial system is deepening.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

Share

anzcomau:Bluenotes/asia-pacific-region,anzcomau:Bluenotes/asia-pacific-region/markets

New ANZ debt issue shows Asian tiger leaving the cage

2015-01-27

EDITOR'S PICKS

-

The Swiss National Bank not only roiled markets last week but potentially signalled the beginning of the end for the ability for central banks to calm markets.

2015-01-21 20:05 -

Looking at the top 10 stocks on the Australian stock exchange, the dominant role played by the Big Four banks in equity portfolios is clear. The top two stocks are banks: Commonwealth Bank and Westpac Banking Corp. In positions four and five are ANZ Banking Group and National Australia Bank.

2015-01-20 19:58