-

A softer inflation outlook could give the Reserve Bank of Australia a little more wriggle room than previously anticipated to support business and consumer confidence and help grow the non-mining economy.

{CF_IMAGE}

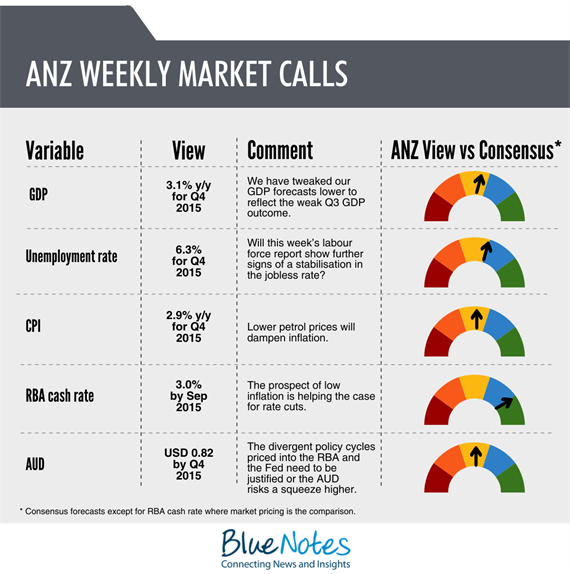

For some time ANZ Research has thought the best course of action for the RBA was to keep interest rates on hold. With global energy costs falling substantially and both core and headline inflation likely to be lower than previously thought there is increasing scope for rates to be reduced in the first half of 2015.

"With global energy costs falling substantially… there is increasing scope for Australian interest rates to be reduced in the first half of 2015."

ANZ ResearchThe early focus in 2015 has been on global disinflation as Euro area inflation recorded its first decline since 2009. ANZ research now thinks it likely the European Central Bank (ECB) will adopt outright sovereign bond purchases in January, a further unconventional loosening of monetary policy.

The unrelenting drop in oil prices is likely to see inflation staying negative in the Euro region for longer than the five-month period experienced in 2009.

This weakness matters also for the US. Recent comments for the US Federal Reserve were fairly consistent with the first rate hike in US rates coming around mid-2015.

Inflation in the US is expected to be low near-term (reflecting, in part, low oil prices) but the Fed expects this effect to be transitory and inflation should eventually rise as the effects of the fall in energy prices dissipate.

In Australia, a benign inflation environment is supporting ongoing speculation of a rate cut. Late last year, the RBA seemed comfortable with the outlook but noted that it was a bit softer than just a few months prior.

While dousing expectations of an imminent rate cut, the RBA left the door open for further monetary policy easing, noting that “if at some point we can be more helpful for confidence by doing something different, then obviously that will be on the table, and we will take a fresh look at all these things in the New Year.”

The RBA would clearly prefer the Australian dollar to depreciate further and do much more of the heavy lifting by supporting financial conditions. The $A is now down to the low $US0.80s but the currency needs to fall further to help rebalance growth in the economy by encouraging the non-mining sector to lift its investment spending.

Recent economic data haven’t provided a clear guide on the outlook for monetary policy.

The November building approvals report showed that low rates are continuing to stimulate the Australian housing sector. The high level of approvals and strong pipeline of activity suggests dwelling investment will continue to contribute solidly to growth through 2015.

Housing finance continued to ease. The softening in investor housing finance will be welcomed by policymakers and should satisfy the prudential watchdog that investor housing credit growth is cooling for now.

Of even more importance will be the employment report due out later this week. While recent data-quality problems suggest we need to be circumspect with these numbers, the labour market outcome remains a key variable in RBA deliberations. For December, some modest retracement in employment looks likely.

The wind-back is likely to be modest given the more positive signals on employment being sent by partial indicators of labour demand including job advertisements and capacity utilisation.

The unemployment rate looks likely to remain unchanged although the risks are tilted to the upside. Further deterioration in the unemployment rate will heighten speculation of a near-term rate cut.

Soft labour market conditions will continue to cap wage increases. This combined with falling oil prices will keep inflation subdued through 2015.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/global-economy/economics

Market calls: a rate cut for H1?

2015-01-12

EDITOR'S PICKS

-

The market reaction to soft domestic trade data released recently highlights the considerable economic challenges Australia still faces. While US activity remains strong, the third-quarter figures clearly demonstrate our domestic headwinds.

8 December 2014 -

The Reserve Bank of Australia is not expected to move on interest rates for at least 12 months after ANZ Research pushed back its forecasts for a rate rise until at least November 2015.

1 December 2014 -

Home building approvals hit an all-time high in Australia in November on the back of a surge in plans for multi-dwelling constructions like apartments.

8 January 2015