-

ANZ has lowered its growth forecast for the Australian economy and have now factored in two 25 basis point rate cuts over the first half of 2015.

"We think the first rate cut will come in March."

Warren Hogan, ANZ Chief Economist

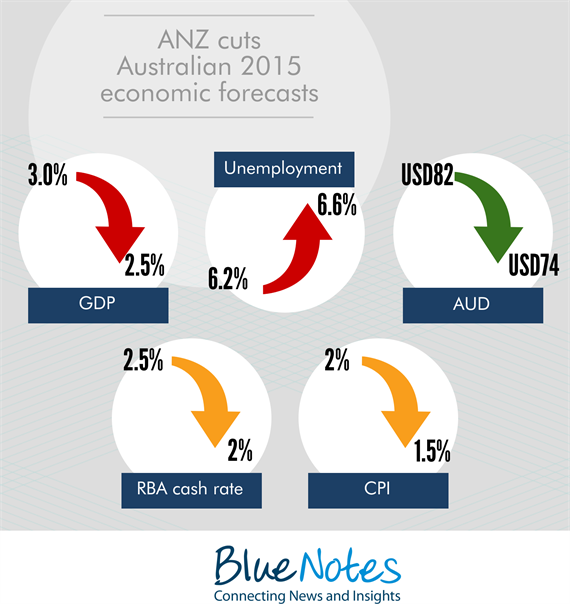

Our decision to lower our growth forecast follows the weaker third quarter GDP report and signs of continued sluggishness in the non-mining economy outside of residential construction. We now expect growth in 2015 of 2.5 per cent, down from 3.0 per cent as of November last year.

Growth in 2016 is broadly unchanged at 3.2 per cent given the lower forecasts for rates and the currency outlined below.

We think the first rate cut will come in March following confirmation of low inflation in late January as well as a read on housing trends in February when the market re opens after the summer lull.

The second is likely after the first quarter inflation report in late April which is likely to show the disinflation trend in place from falling energy prices and a soft labour market. These cuts would take the cash rate to 2 per cent following the May RBA board meeting.

Our decision is not based on the Australian economic outlook deteriorating in any substantial way. Rather, the downward pressure on prices from lower energy costs and the risk the Australian dollar’s depreciation may stall as global interest rates fall make monetary policy a potentially important policy lever once again.

To hold rates steady as inflation falls and housing credit slows would be to allow a proxy tightening of policy to occur. To maintain an accommodative policy stance, the RBA board may be forced to reduce the nominal cash rate over the months ahead.

ANZ has had a fairly consistent view of Australian monetary policy for the past 18 months, that is, rates on hold with a rise likely sometime 'down the track'. This reflected our cautiously optimistic view of a global recovery and that the non-mining recovery in Australia would gradually materialise.

We remain confident the Australian economy will make the transition from the mining boom back to what we call 'business as usual'. A steady expansion of the economy lead by business spending, housing investment, consumer spending employment growth across a wide range of sectors is still the most likely outcome.

Monetary policy has been stimulatory as evidenced by the pick-up in housing activity in recent years. But the broadening of the non-mining recovery beyond housing and construction has been disappointingly slow.

The RBA board has been reluctant to provide further monetary stimulus in the past year, questioning the effectiveness of further interest rate reductions while hoping financial conditions would ease via stronger asset markets and a lower currency.

As we enter 2015 the fall in oil prices and a further significant reduction in global term interest rates have brought into question the RBA's previous policy approach.

Following the fall in global oil prices we have cut our expectations for Australian inflation for 2015. A sustained drop in oil prices will filter through to core inflation via the downward pressure it will exert on energy costs more broadly and the impact of this on business costs.

In the presence of a weak labour market, a lower headline inflation rate is more likely to filter through to wages and then core inflation as well. We now expect CPI to trough at around 1.5 per cent in mid 2015 from 2 per cent previously. Core inflation is now expected to be near 2 per cent in late 2015.

We have pushed up our unemployment rate forecast in 2015 a little. Weaker domestic growth and the recent profile of unemployment rate outcomes suggest the unemployment rate will now ‘peak’ at 6.6 per cent in Q2 before stabilising. We do not expect the unemployment rate to trend lower until mid-2016.

Lower growth and lower inflation have increased the scope for the RBA to provide more help to the non-mining recovery via lower interest rates. Indeed, under these forecasts, a stable cash rate will result in higher real interest rates and by implication, tighter monetary conditions.

With the non-mining recovery still sluggish outside of housing and unemployment drifting up, we believe that the risks from inaction on monetary policy are now greater than the risk of further rate reductions. We expect a 25bp cut in March 2015 followed by another after the Q1 CPI in May. Rates are not expected to remain at 2 per cent for long. We expect 100bp of tightening commencing mid-2016.

The Australian dollar is expected to depreciate further than previously anticipated due to ongoing weakness in commodity markets, a winding back of mining capital investment and lower domestic wholesale interest rates. We now expect the Australian dollar to fall to USD0.74 in the second half of 2015 as Australian interest rates fall over the first half of the year.

The other feature is the housing market. The demand for new mortgages has clearly slowed over the last quarter of 2014. The latest housing finance figures show a substantial slowdown in new mortgage demand in late 2014. Auction clearance rates in Sydney and Melbourne have softened and the threat of excessive leverage is abating. A robust housing market is important to the economy’s transition to a sustained non-mining economic expansion. Outside of Sydney and Melbourne owner occupied mortgage demand remains soft while the pace of price rises is slow.

These changes largely impact ANZ’s economic and financial forecasts for 2015. Our medium-term view on the Australian economy has not shifted substantially. We still believe Australia will successfully make the transition to a non-mining led economic expansion over the medium-term.

While the non-mining recovery has disappointed us thus far, we have no reason to believe it will go into reverse.

The chance of genuine recession in the Australian economy over the next two years remains low. Lower inflation and a softening in new mortgage demand over the final months of 2014 have provided the RBA with scope to provide a boost to domestic demand. A modest reduction in Australian interest rates combined with lower energy costs, low wage growth and a falling currency should ensure a return of robust growth across the economy in 2016.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/global-economy/economics

ANZ cuts Australian growth, rates outlook for 2015

2015-01-15

EDITOR'S PICKS

-

For those looking to borrow, the renewed fall in interest rates has delivered near-perfect conditions.

2015-01-14 18:41 -

A softer inflation outlook could give the Reserve Bank of Australia a little more wriggle room than previously anticipated to support business and consumer confidence and help grow the non-mining economy.

2015-01-12 17:38 -

Home building approvals hit an all-time high in Australia in November on the back of a surge in plans for multi-dwelling constructions like apartments.

2015-01-08 17:01