-

It has been a mixed, sometimes volatile year for the global economy. The good news is ANZ expects 2015 to offer moderate gains in financial markets – albeit with increased volatility - as global economic growth grinds up a gear.

"ANZ expects 2015 to be a year of moderate gains in financial markets with increased volatility as global economic growth grinds up a gear."

ANZ Chief Investment Officer, Stewart BrentnallIn 2014 growth disappointed with lower-than-expected inflation and geopolitical concerns out of Russia and the Middle East. Nevertheless, financial markets posted reasonable returns supported by stimulus measures from the world’s central banks.

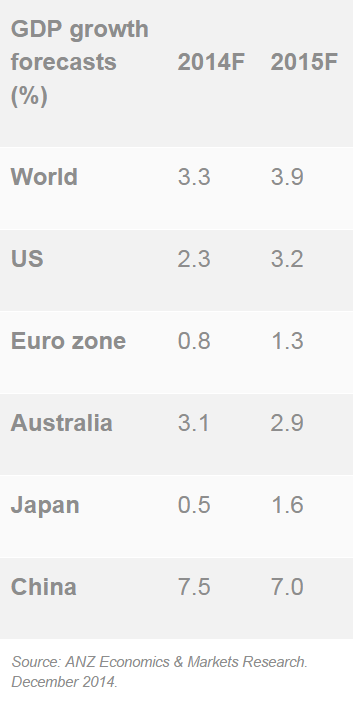

In 2015 ANZ expects global growth to rise back to more traditional levels after being below average for the last three years. The US is expected to support this pickup through increased trade and there will be a continued benefit from low interest rates, less government spending cuts and lower oil prices, which is expected to boost consumer spending power and business profitability.

Importantly, ANZ sees a combination of lower commodity prices and excess capacity across much of the developed world, indicated by persistently high unemployment, keeping inflation subdued.

ANZ expects the global growth outlook to support continued outperformance in global sharemarkets over defensive assets. However as rate rises near in the US ANZ’s focus is on quality growth assets while minimising exposure to less liquid and higher-risk assets such as emerging markets shares and debt.

ANZ is underweight Australian shares which face headwinds from weaker commodity prices and neutral on New Zealand shares for similar reasons, although the headwinds are likely to be less severe.

While ANZ expects only moderate growth and low inflation to keep bond yields well anchored the risks are skewed towards a rise in bond yields (a fall in prices) that would see fixed income assets underperform over the coming year.

With the US economy leading the global expansion and the US central bank likely to be the first to raise interest rates, ANZ expects the US dollar to continue to strengthen against most major currencies.

At a country level, the US economy is the locomotive likely to pull the rest of the world with it. This is expected to benefit Europe and Japan, both of which faltered in 2014.

While Chinese growth should be much higher than in the developed economies, it is still expected to be well below its own average of the previous decade as China continues to shift focus from exports and investment to domestic consumption.

The Australian and New Zealand economies are expected to grow close to a trend pace although lower commodity prices are a headwind for growth.

Australia

Growth in Australia remained solid in 2014 despite falling mining investment. Weak national income growth and soft consumer confidence hampered the economy’s transition to stronger non-mining demand, resulting in a gradual rise in unemployment.

ANZ expects the transition of the economy to continue in 2015 as the lower Australian dollar boosts competitiveness. Stronger growth in major developed economies should also assist. With household saving rates high, any improvement in consumer confidence should help assist a pickup in consumption alongside continued growth in housing construction.

Progress will likely be slow, however, as falling commodity prices remain a significant headwind to national income in the near term. This could see unemployment rise further, limiting any improvement in consumer confidence. ANZ believes an even lower $A is needed to support this transition.

Meanwhile, the lack of progress on unemployment and contained inflation should see the Reserve Bank of Australia maintain the cash rate at its current low level throughout most, if not all, of 2015.

NEW ZEALAND

Economic growth in New Zealand has been above trend in recent years. Despite this, there has been little to show in the form of inflationary pressures. The only exception has been the Auckland housing market.

ANZ expects domestic NZ growth to ease but remain robust over the next 12 months, in part due to a growth boost from the Christchurch rebuild coming to an end. Weaker terms of trade, in particular declines in dairy prices, are also expected to contribute.

Our expectation is slower growth and the continued absence of inflationary pressures will see the RBNZ keep interest rates unchanged in 2015.

THE ASIAN REGION

The uneven recovery in exports is likely to continue throughout Asia in 2015. While a pickup in consumer spending and business investment in the US should boost demand for Asian exports, subdued growth in Europe and China respectively is expected to offset some of the benefits.

Lower commodity prices offer a bright spot for Asia. As most Asian economies are large net oil and commodity importers, a sustained period of low prices can potentially improve trade and current account balances.

Lower oil prices can also mean smaller energy subsidies for governments and higher disposable income for consumers. In particular, India is expected to be a beneficiary of these favourable dynamics, and its star may shine brighter as the prospects for serious reforms improve in 2015.

Finally, contained price pressures also open the door for rate cuts. While the policy stance in the region would probably need to remain restrictive to act as a shock absorber to rising US rates, the painful cycle of rises has probably run its course.

CHINA

China’s economy suffered from growing pains in 2014 as the long transition towards a consumer-driven growth model continued. This new economic framework is expected to see China continue to shift from a high-growth to a lower-growth trajectory.

In addition, China’s desire to slow credit expansion and shadow banking is likely to continue to weigh on the economy in 2015. The country’s weak property market would also be a drag to the economy; to date it has yet to respond convincingly to greater government mortgage support and relaxation of ownership restrictions. Some relaxation of the transaction tax on the housing market also appears likely.

Not surprisingly, the risk of deflation is rising against this lacklustre growth backdrop. While the government has preferred to use more targeted easing measures in 2014, ANZ cannot rule out the possibility of broader based pro-growth measures such as a further cut in interest rates or the reserve requirement ratio especially if growth starts to slow sharply in 2015. The capacity for policy makers to respond with more widespread stimulus means the risks of a sharper downturn remains low in 2015.

Over the long term, new growth drivers such as the development of innovative and high-end equipment industries as well as the ongoing urbanisation program should help China achieve higher quality and more sustainable growth. But growth pains cannot be avoided in the near term.

JAPAN

The year started strongly in Japan as the Bank of Japan (BoJ) was successful in driving the yen lower. However, an increase in the value added tax (VAT) rate in April drove the economy back into a technical recession. This highlighted the dichotomy between a fragile consumer and a strengthening producer sector.

ANZ expects growth in 2015 to be supported by lower oil prices and the BoJ’s strong commitment to do whatever necessary to drive the economy out of deflation. The continued expansion of its balance sheet is likely to push the yen lower. The announcement of a delay in the next tax rise and potential for further short-term government stimulus are also positive for the growth outlook.

However, if there is any lesson to be learned from the past two years, it is sustainable inflation in Japan can't be achieved via a lower currency. Indeed a lift in inflation without a pickup in wages simply hurts households' purchasing powers, and with it growth.

More needs to be done on the structural reform front to boost labour supply and wages in order to be confident on Japan’s long-term prospects. The government will need to progress this reform agenda in 2015.

Download the full ANZ 2015 Global Market outlook to gain in depth insights about what to expect in investment markets around the world in 2015.

Stewart Brentnall is Chief Investment Officer, ANZ Global Wealth.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

Share

anzcomau:Bluenotes/global-economy,anzcomau:Bluenotes/global-economy/economics,anzcomau:Bluenotes/global-economy/markets

Where the Asia-Pac economy is going in 2015

2014-12-22

EDITOR'S PICKS

-

In some countries, the issues of climate and economics are treated entirely separately, divorced from one another except insofar as finance is required to fund environmental initiatives.

9 December 2014 -

Chinese officials in Shanghai, the largest city in the world’s rising financial behemoth, have made no secret their desire for the region to become a global trading hub. Shanghai has a stated goal of becoming a major global centre for finance, commodity trading and shipping by 2020. A key part of its answer to this has been the Shanghai Free Trade Zone.

5 December 2014 -

The Reserve Bank of Australia is not expected to move on interest rates for at least 12 months after ANZ Research pushed back its forecasts for a rate rise until at least November 2015.

1 December 2014