-

One of the themes that came up a number of times during the range of meetings during my recent trip to North America was about where the next crisis was most likely to come from. In particular there was focus on how the banking industry was likely to cope during some future financial crisis.

The question was interesting as it starts with the premise the problems will start with, or be felt most acutely by, the banking system itself. While there is no doubt that the banks will be impacted by any future financial crisis, the question seemingly ignores the fact the post-Lehman environment has forced banks to de-risk in most areas of market making and book running.

"The regulatory environment has effectively made the entire investment structure more risky."

Sean Keane, Principal of market analysis, Triple T ConsultingIn fact, the degree of change in this area has become meaningful enough that the banks themselves are not likely to be the source of the next financial crisis. US regulators have focussed the major elements of the Dodd-Frank Act and the Volcker Rule on bank risk-taking activity. The impact of these rules, and the consequent reduction in risk capacity brought on by these reforms, has been further amplified by Basel III (global regulations) and the imposition of much tougher local liquidity standards on banking activities.

{CF_IMAGE}

What this means is the world's largest banks no longer have the ability, or the appetite, to take on or hold very large proprietary positions - even in the most liquid of markets. The huge moves seen in mid-October were indicative of the changed environment. Those charged with global financial stability should have been terrified by the price action witnessed in the US Treasury market on October 15.

The US Treasury market is the world’s deepest and most liquid traded bond market and it sets the benchmark interest rate off which every single asset is priced globally. This includes all fixed-income products as well as every other asset which is priced with reference to a discount rate or comparison yield spread. It also includes every foreign bond market which is inevitably priced with either direct or indirect reference to the US bond market.

Volatility and illiquidity in this market therefore has global consequences and far reaching repercussions.

The horrific price action on October 15 told us the post-2008 regulatory response to the GFC has been misguided. In focusing attention solely on bank risk-taking activities in financial markets (not even the cause of the GFC) the world’s regulators have forced banks to substantially downsize their role as the conduit of financial market interactions.

While this may be a very good thing in reducing the specific risks that exist in this specific part of the financial market infrastructure, the markets themselves are now faced with managing more financial assets than ever before. And they are less well able to do so because of the reduced role of the largest banks.

The Financial Times noted some IMF numbers showing the “amount of money in mutual funds and exchange traded funds (ETFs) has tripled since the crash to near $US1 trillionn.” The IMF also noted most of that money sits “in high yield corporate debt and emerging market government bonds”.

Global fund managers - both fast and real money - continue to accumulate ever larger pools of invested capital, much of which is coming from the global savings industry that is being encouraged by governments everywhere.

Savers are expecting fund managers to shelter them from the ravages of the financial repression that is being brought on by quantitative easing. For investors and fund managers the world’s major equity markets have become the preferred 'tin hat' chosen by the fund managers.

As the amount of money invested in these funds has steadily increased global fund managers have steadily deployed the incoming cash into all corners of the world's markets. As returns have fallen the managers have accepted a little more risk on their investments by going into lesser traded names; they have accepted a little less transparency in their investments, buying stocks that refuse to grant full disclosure; and they have accepted longer terms for their investments by pushing money further out the curve to capture some additional carry versus the cash rate.

In virtually all cases they have willingly accepted more risk for the same (or lower) levels of return.

By reducing the operational capability of the banks to comfortably accommodate movements into and out of these markets, the regulatory environment has effectively made the entire investment structure more risky. Fund managers who want to move or hedge their huge positions now find liquidity more difficult to access from the banks which have traditionally acted as price makers and book runners in these markets.

Banks are unwilling and unable to accommodate the type of proprietary risks they sought and accepted pre-Lehman and in many cases they will only accept a trade when it’s obvious they have the liquidity to clear it. The pre-GFC willingness and appetite to capture and facilitate flow and to hedge it across other products and markets has been significantly reduced. Bank traders have been placed under much tighter risk controls. Stop-loss limits are tighter and the days of bank book runners doubling down on positions are long gone.

What this means for the fund management community is that in normal markets bid/offer spreads are narrow and incremental position additions or modifications are reasonably easily facilitated, with low operational costs. It also means however that in fast markets spreads widen very quickly to levels that would never have been imagined 10 years ago as everyone takes a step back and waits to see where the next clearing price appears.

Price leadership is abandoned with everyone waiting to see what everyone else will do. Few in the price making community are rewarded or encouraged to take on risk for which there is no immediate and clear exit.

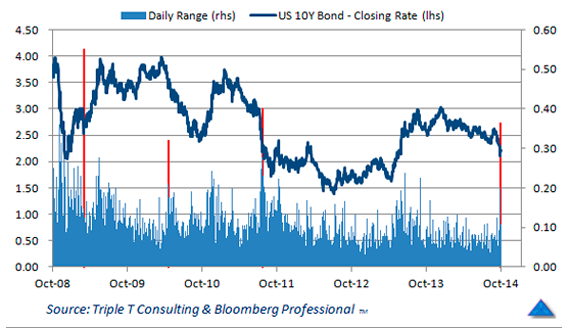

The near 10 sigma event seen in the US Treasury market on October 15 was every bit as scary as the equity flash crash of May 2010. In many ways it should be thought of as a much more serious warning shot about the way in which market performance is breaking down.

The US 10-year bond contract traded a massive 36.5 basis point range, most of which was covered in less than one hour’s trading during the morning session. The range traded last Wednesday was the third largest recorded in the world’s most important fixed-income market since October 2008.

The difference this time around was that nobody appeared very clear about what the real drivers of the move were other than bad positioning and terrible market liquidity.

{CF_IMAGE}

The reason that US financial markets are the most deep and liquid in the world is precisely because US financial markets are the most deep and liquid in the world. Liquidity begets liquidity in financial markets.

Global investors and fund managers flock to the US markets because bid/offer spreads are tight, liquidity is deep and transaction costs are low. Issuers follow because that's where the vast majority of investors prefer to do business. When markets fracture, as they did that day, everyone takes a step back.

Eyebrows are raised in surprise and caution creeps in. Those who are in the business of habitually providing liquidity as market makers pull down their shutters and retreat into their shelters. This in turn amplifies the volatility in the markets and worsens the way in which asset prices trade.

Illiquidity begets illiquidity and in the post-Lehman world the risks of stepping into provide market liquidity are often not equal to the reward for those whose mandate is to clear flow.

It’s an ironic outcome of the post-GFC regulatory changes that in 'de-risking' the banking system the likelihood is the world's major asset markets may become less stable and more volatile during periods of change. The ability of real and fast money managers to move positions in a fast market is considerably reduced compared to 2007 because banks now have less ability or desire to take on the risk the market wishes to move. They will generally only do so if they can see an exit without loss.

This reduction in bank facilitation may actually end up triggering the next crisis itself, though the major catalyst likely won't be found in the banking system. Instead it will come from those who now hold most of the risk - and who will not necessarily have realised how difficult it will be to manage their positions in such illiquid markets.

The older, larger and more established money managers have seen this movie play out at various times in the past and likely have strategies and plans in mind to deal with some of these problems.

The obvious one is that the funds themselves will increasingly have to take on the cross asset and basis risk that the banks previously held. They will of course need the capital and collateral to be able to do this.

Some however will likely be assuming the liquidity and price competition that existed on the way into a trade will also be there on the way out. That almost certainly won't be the case. October 15 was a clear warning shot as to what might happen.

In what was a strange quirk of timing Reserve Bank of Australia Assistant Governor Guy Debelle warned of this exact risk just 24 hours before the US fixed income market descended into frenzy on the Wednesday. He said:

“there are a number of investors buying assets on the presumption of a level of liquidity which is not there. ...this is not evident when positions are being put on, but will become readily apparent when investors attempt to exit their positions.... here are probably a sizeable number of investors who are presuming they can exit their positions ahead of any sell-off. History tells us that this is generally not a successful strategy. The exits tend to get jammed unexpectedly and rapidly.”

As much as AG Debelle’s prescient words were remarkably insightful given what happened to US fixed income markets the next day, his focus was actually on the risks around a large sell-off in bond markets, rather than the sudden rally that was actually witnessed.

The fact the market reacted so violently and in such a fractured manner is however evidence of the fact that liquidity was an issue and investor assumptions were not appropriately calibrated for the current environment.

Where Debelle was absolutely right was in saying that one thing he was sure of was "that the spike in volatility will be blamed, rightly or wrongly, on regulation-induced reductions in market-making.”

In the rate market in particular the price action in the Treasury Notes was appallingly dislocated and market participants were shocked at the decline in liquidity as yields plunged and then corrected in the morning session.

In the usually liquid and highly traded Eurodollar interest rate strip liquidity simply vanished as price makers withdrew and there were various suggestions that black box algorithms had been switched off due to the incredibly volatile conditions.

For some time that day it wasn't at all clear where prices were actually trading because liquidity became so thin.

This report was originally written by Sean Keane of Triple T Consulting for Credit Suisse and is reproduced with their permission.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

Share

anzcomau:Bluenotes/business-finance,anzcomau:Bluenotes/business-finance/banking

Safer banks = more volatile markets

2014-10-29