-

The abolition of signatures as a means to verify credit card payments has prompted some alarming media coverage, such as the story noting a restaurant owner had to send customers around the corner to an ATM to get cash to pay their bill.

I never even realised you could get cash from an ATM using your signature….

"Are restaurant diners tipping less?"

Now it transpires getting rid of signatures is costing waiters their tips. Diners apparently, whether confused by new PIN only devices or embarrassed at the scrutiny, are no longer tipping as much.

The evidence for this is anecdotal but it’s a hand-to-mouth example of the complexity of the forces interacting in a payments system. It’s easy to leap to the most obvious conclusion and indeed that is what has happened with the entry of Apple into the contactless payments universe with iPhone 6 and Apple Pay.

For many, Apple’s entry is the beginning of the end for traditional players as Apple takes over not just payments but also traditional banking.

Yet payments is such an arcane universe that it is never easy to analyse who or what causes what to what or who. In Australia, the Reserve Bank has been courageously grappling with improving the price signals in payments for over a decade.

{CF_IMAGE}

Photo: Jean Tirole, professor at Massachusetts Institute of Technology (MIT), speaks at a macro policy discussion during the International Monetary Fund (IMF) and World Bank Group Spring Meetings in Washington, D.C., U.S., on Wednesday, April 17, 2013. Photographer: Andrew Harrer/Bloomberg via Getty Images.

Jean Tirole was awarded the Nobel Prize in Economics for a body of work on complex economic systems including payments.

For an easy read, have a look at “Must-Take Cards: Merchant Discounts and Avoided Costs” co-written with Jean-Charles Rochet which identifies “four key sources of potential social biases in the payment card systems’ determination of interchange fees: internalisation by merchants of a fraction of cardholder surplus, issuers’ per-transaction mark-up, merchant heterogeneity, and extent of cardholder multi-homing”.

Are restaurant diners tipping less? And if they are, is the reason economic – times are tough – or structural – a new system?

Before joining ANZ, I happened to do a bit of restaurant reviewing and wrote quite a bit on the economics of restaurants. One of the interesting themes which emerged after the introduction of surcharging by merchants on card payments was tips went down.

I haven’t seen any formal research on this but anecdotally restaurateurs and waitstaff told me (and other reviewers) diners who objected to the surcharge would register their ire by not tipping. You’re charging me 3 per cent to use Visa? Why would I tip?

Of course, and the RBA would be sympathetic to this lack of pricing fidelity, not tipping punished the staff who had nothing to do with choosing to surcharge. The customers’ response was pointless unless staff then banded together and demanded the surcharge be dropped. Unlikely.

The complexities in the world of Apple Pay are even deeper.

Apple hasn’t taken over the payments business of banks. What it has done is facilitate the use of its new phones as contactless payment cards (the card being an invisible presence in the phone). Typically, Apple is not the first to do this. Many android phones have used NFC (near field communication) technology to do this for years.

But Apple has negotiated with a number of financial institutions to be paid to do this. This is new – in phones at least.

In the US, Apple’s first market for payments, so called issuing institutions (analogous to the bank which “issues” a customer a payment card and holds the funds) have agreed to pay Apple a slice of the transaction or interchange fees.

The thin end of the wedge, many argue.

Yet that ignores the fact it can make sense to sacrifice revenue per transaction if there is greater overall volume – that is, unit revenue is lower but total revenue higher.” . Presumably those institutions which have struck a deal with Apple, and they include Wells Fargo, Citi, American Express, Visa, MasterCard and dozens of others, believe access to Apple’s 800 million plus customer base justifies paying out a reported 15 basis points per transaction.

The Financial Times’ Lex column noted mobile payments are just 7 per cent of total in-store transactions in the US. “Banks have been unable to build a compelling technology,” Lex said.

“Apple has the tech expertise, brand recognition and the devices. A token system protects personal data and is expected to make mobile transactions safer than cards. Lower fraud expenses would help the banks offset the Apple discounts.”

In Australia there was an analogous situation when eftpos was first launched in the 80s. Facing the classic chicken and egg dilemma, where consumers wouldn’t use the system if merchants didn’t accept it, the banks agreed to pay Woolworths, Coles Myer and the largest petrol chains a share of the interchange fee – much more than 15 basis points – to accept eftpos and build critical mass.

This so-called 'negative interchange' remains an anomaly of the Australian system.

Media coverage outside the US has focussed on when the payments capability will be switched on in local markets, but there are particular characteristics of this deal and the US market which mean it is not universal.

The Apple share of US smart phones is about 40 per cent of the total and just under 20 per cent of total mobile phones - much higher than most other markets. Therefore, partnering with Apple delivers more bang for US institutions. In most other markets though the Apple smart phone share is closer to 10 per cent.

Moreover, analysis of the share price of other payments-related stocks after the announcement suggests investors don’t see Apple as eating their lunch. Both Visa and MasterCard for example, who have teamed up with Apple, saw a rising trend in their share price.

That leads analysts to argue Apple has concluded it can’t take on the banks and networks by itself. With a handset market share around 10 per cent setting up a 'closed loop' – where Apple does everything itself – wouldn’t have critical mass. And it would mean being regulated like a bank.

Payments insiders also believe that Apple’s lower penetration coupled with lower overall interchange fees in other geographies mean it will face more opposition to this sort of deal offshore.

Australia, New Zealand and many Asian markets are also different to the US in that banks act on both sides of a transaction – as issuers of payment vehicles and processors or 'acquirers' of merchant transactions. In the US different institutions play on the two sides.

In China, while the Chinese payment scheme UnionPay is likely to be a network partner, one would expect this interchange sharing arrangement to have to be negotiated differently.

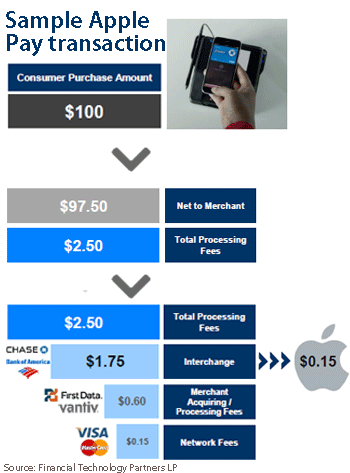

As Steve McLaughlin of Financial Technology Partners wrote in an excellent piece of analysis, “Apple’s entrance into the payments space has the potential to be highly disruptive however, the structure of Apple Pay preserves the role of the incumbent players in the payments value chain”.

That’s not to say revolution is not afoot in payments. Potentially more disruptive for incumbent players is MasterCard’s far lower profile deal with Facebook. MasterCard will access Facebook Asia Pacific user data to generate insight into online consumer behaviour – and sell these insights to banks. It will also work with banks to tailor specific offers.

Macquarie Research noted “what is interesting about this partnership is that should MasterCard successfully utilise the Facebook user data, this could be a catalyst for Facebook to become more of a digital disruptor with the goal of driving a wedge between the banks and their customers”.

Macquarie reckons data analysis and packaging could just be the “tip of the iceberg for these new world competitors” with payments, merchant acquiring and lending all in the crosshairs "with around 25 per cent of system revenue the ultimate target”.

And that wouldn’t be offset by extra volumes. But as the demise of tipping revenues makes clear, it is difficult to determine what will cause what.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/technology-innovation/digital,anzcomau:Bluenotes/technology-innovation/innovation,anzcomau:Bluenotes/technology-innovation/payments

An Apple on Pay won’t keep the banks away

2014-10-21

EDITOR'S PICKS

-

In Melbourne’s Docklands precinct, where the ANZ mothership is berthed, there’s dozens of small cafes and lunch spots. Almost all accept contactless card payments, the so-called “tap and go” system.

9 June 2014 -

The Medicis in the 15th century (‘God’s Bankers’) were constrained by the Catholic Church’s ban on usury - the charging of interest - on loans.

1 September 2014 -

If my wife had said to me 10 years ago I would wake up at 3am to watch the launch of a new mobile phone on the other side of the world, I would have told her she was crazy and gone back to watching reruns of Seinfeld.

20 October 2014