-

A few of us can still recall our first tentative use of an ATM – an 'automated teller machine' - 35 years ago. The concept of accessing cash from your bank account via an unattended machine was then an alien concept that many people found somewhat confronting. Presenting a passbook at a bank branch counter to withdraw funds was how you got cash. And as with many technology led changes, there was suspicion of this newfangled device.

Today we would be bemused and annoyed if we couldn’t withdraw cash 24/7. The convenience offered by ATMs not only broadened the ability to withdraw funds on an as-need basis, but for a period in the 1980s, it threatened the very fabric of the bank branch network itself.

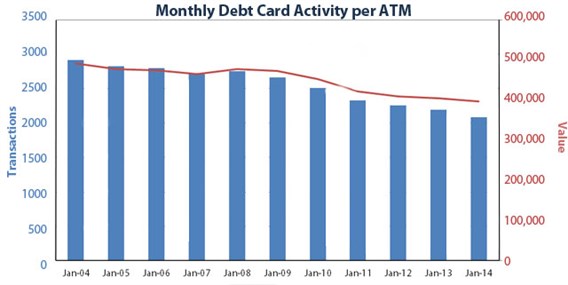

"Despite the absence of growth in ATM deployment, the activity levels per device are decreasing."

Mike Ebstein, MWE ConsultingThe ATM was regarded as the way forward, potentially replacing a staffed branch with an automated self–service banking facility. The size of the Australian bank branch network shrank significantly as the ATM network grew rapidly in size.

Fast forward to today and we see vastly different dynamics at play. The ATM remains a cornerstone of retail banking operations, a basic feature of retail consumer banking. Although new features are still being added to ATMs, device numbers have stopped increasing and bank branches are regarded as a key tactical tool in the marketing drive to attract and grow retail bank operations. What has altered?

{CF_IMAGE}

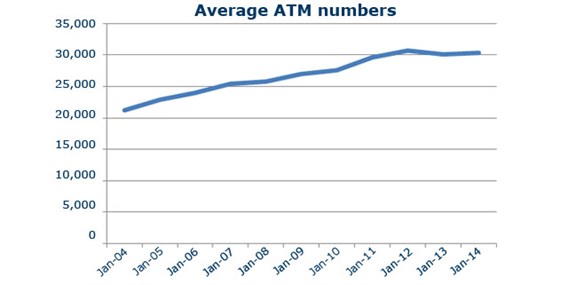

Following the widespread launch of ATMs in the 1980s, the network size more or less doubled every ten years. That momentum has now disappeared.

In June 2014, there were 30,544 ATM operating in the Australian market. That number was almost unaltered from the 30,511 in place two years before in June 2012.

Yet despite the absence of growth in ATM deployment, the activity levels per device are decreasing. That trend had been somewhat evident in the first half of the last decade but has become more pronounced over the past five years.

In that time, direct charging commenced at ATMs and “tap and go” technology gained traction at point of sale for lower value transactions.

{CF_IMAGE}

In 1995, an average ATM processed 4,896 transactions per month with a value of $616,123. By 2004, that had reduced to 2,915 transactions per month with a value of $491,805 and today an average ATM processes 2,087 transactions with a value of $396,314.

The emergence of e-commerce as a threat to bricks and mortar retail is changing the way shoppers purchase and pay.

The development of payment card technology that dispenses with a PIN for transactions below $100 in value is changing the way shoppers pay.

This is true not just in Australia, but also in New Zealand. Over the past 3 years, an average credit card purchase in Australia has dropped from $144 to $135 whilst in New Zealand it has declined from $99 to $93.

That lower figure in New Zealand reflects that New Zealanders are already far more likely to use cards for small value purchases rather than cash – a result of historically lower card fees.

Forthcoming enhanced mobile payment technologies will further alter the way we pay. The common feature is a digital payment product that reduces the need for cash.

The ATM will be around for a very long time. In part, this is because we will not see the cashless society for a very long time. Consumers still require cash and they demand the ability to access it when it suits them rather than when the bank is open.

We continue to see enhancements such as cardless withdrawals and value-add features such as the ability to change a PIN and these satisfy our increasing requirements for convenience and flexibility.

In much the same way, the positioning of the bank branch has shifted from an account access centre with limited availability to a sales and service facility to cater for the increasingly complex needs of our changing lifestyles.

Once threatened by the ATM and the technology it represented, the branch today is recognised as not only a physical manifestation of the banking entity and the security it denotes, but a centre capable of delivering the more complex services needed by today’s society.

Maybe it is premature to predict the ultimate demise of the ATM, but its primary role as a dispenser of cash is less and less important as less and less cash is used. Is it just a matter of time until this staple of late 20th century banking morphs into something else, or even disappears entirely?

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

-

Share

anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/technology-innovation/digital,anzcomau:Bluenotes/technology-innovation/economics,anzcomau:Bluenotes/technology-innovation/innovation

Death to the ATM – is it a matter of time?

2014-09-22

/content/dam/anzcomau/bluenotes/images/articles/2014/September/MWE atms chart 2.jpg