-

We are seeing a shift in generations, from those who grew up with the internet to those who have 'discovered' the possibilities of data. A shift from 'Digital natives' to 'Data natives'. Data natives expect their world to be 'smart' and to seamlessly adapt to them and their preferences.

The mobility trend that began with smart phones is rapidly expanding with the proliferation of connected devices. Distribution channels as we once knew them are growing to include connected devices, creating new opportunities. Cars are already internet enabled - several already integrate to iTunes. It’s only a matter of time before you can access a banking app like goMoney from your car using voice commands.

Digital Natives want to be able to program their thermostat - and connect to it over the cloud to check the heating is on. Data Natives want the thermostat to be intelligent - to learn how warm they like each room in Summer and Winter. And optimise these preferences to reduce their energy bill.

Digital natives might use a cloud-connected baby monitor. Data natives expect their monitor to calculate crying percentiles based on data from millions of other babies and know the difference between babies murmuring in their sleep and babies in distress or in need of attention.

Digital enables connectivity. Data makes it useful. Data native customers have much higher expectations of organisations.

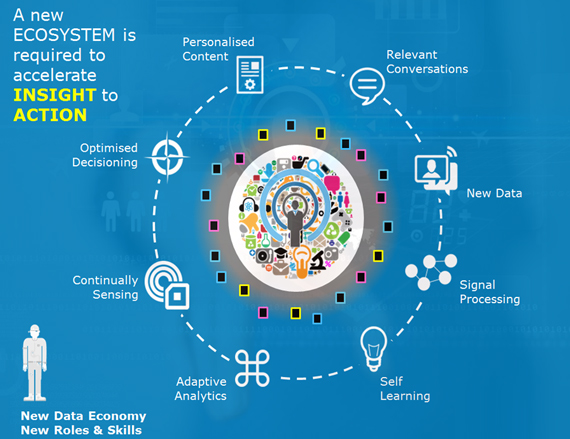

As a bank we are working on new capabilities that build a “sense and respond” capability across all of our channels. Our aim is to be continually scanning for customer events and to be able to understand the context, formulate a decision and deliver the right response, all integrated into our operational systems and tailored to the customer across any channel or device.

A simple example might be identifying when a high value customer has received an unexpected bill and is about to have their card declined. We need to be able to make a split second decision whether we contact the customer, requesting approval to transfer funds between accounts to enable the transaction.

Responding to expectations of data native customers requires significant changes not just to technology but also to business processes and our culture. Our platforms are becoming more integrated with a streamlined flow of information managed by context aware decision engines. And we are shifting our culture to consider new processes and new skills and capabilities.

Macro Trends

Trust has always been a key currency for banks but customers have different attitudes to privacy and protecting their data. One of the most popular free apps before it came as standard issue with your phone was the flashlight app – which merely enabled your camera flash. In exchange for downloading the app for free, rather than pay $5 for it, users had to provide their geo-location all day long without any notion of who would get this data or what they would do with it.

Non-traditional competitors – such as merchant acquirers, supermarkets and peer-to-peer lending – offer similar products and services to banks and are influencing customer expectations and changing our industry.

Mobility and wearables offer companies and individuals unique insights into consumer behavior. The likes of fitbit and jawbone offer insights into your health and will in time provide data for insurance policies. Disney’s MagicBands – like magic beans but they grow data, represent a billion dollar investment by Disney. They are individually coded to each visitor and allow Disney to track individuals wherever they go in their resorts. MagicBands let you check into rides, skip longer lines, pay for purchases and open your Disney hotel room.

The pitch that Disney is making is personalisation but the insights and data that they will get for models on itineraries, line length and weather will help them figure out what influences length of stay and cash expenditure and these have big prizes attached.

Expectations are higher

Sales and service experiences are measured against Apple, Google and Amazon not against other banks and retailers. But trust is a key advantage for banks and we need to find ways to demonstrate to customers we protect their data and use the information to add value back to them. With trust, customers can be persuaded to share more data with you, as long as they see the benefits.

The skill shortage

Addressing the skills gap will be one of our toughest challenges. We need new capabilities such as anthropologists, behavioural scientists and psychologists working alongside bankers, data scientists and software developers. It will be challenging to hire and retain these people in a ‘traditional’ banking culture – and that means that we need to adapt our culture to be successful.

Next generation analytics moves the focus away from managing data – organising and understanding it, to using and applying it in a contextual way. It’s what you do with the data that creates the value.

We need to bring new capabilities together into an eco-system. It’s not about predictive models but highly personalised content that creates relevant conversations with our customers. We are informed by new types of data – like video or tone of voice, that pick up on key behavourial signals, and we need to create systems that continually adapt and self-learn.

One of our key challenges will not be adopting new technologies – it will be creating new roles and skills to work in the data economy. We will no longer need people to manage campaigns - we will need people to manage the machines that manage the campaigns and thousands of micro models each day.

Consider the world of unstructured analytics - already providing great insights to the sports world. Let’s take a look at last month’s World Cup semi-final between Germany and Brazil. Prior to the match, the German team used analytics as part of their planning. They looked at how players responded on the field to stressful situations, how players reacted when fouled and their preferred routes on the pitch. The team analysed data from on-field cameras, looking at player positions and speed using SAP software. The data was analysed in real time and feedback was provided to managers and coaches via mobile devices.

Germany cut their average possession time down from 3.4 seconds to 1.1 seconds increasing the velocity of play - a factor in their victory over Brazil. And as we know crushed Brazil on the way to becoming world champions.

ANZ and unstructured data

At ANZ, we are looking at unstructured data to improve our service to customers through biometrics and voice analytics that support an improved experience through the call centre with intelligent routing capabilities.

We are investing heavily in streaming capabilities to enhance our fraud detection, across both payments and digital channels. This capability is also helping us identify patterns of customer behaviour to help us service our customers better and identify opportunities for timely and relevant conversations.

As banks, we can detect customer signals that point towards an unmet need – for example, when a customer looks at a home loan calculator or makes an unusual deposit – this is a signal that another event is going to occur. We need to predict this event and provide the right advice, the right price and related information to add value to the customer through their preferred channel and in a way that the customer deems to be helpful and not intrusive.

Unstructured data in the world

The car industry has embraced next gen analytics and our cars are becoming smarter. Self-parking cars are now routine, in-built sat nav systems are automatically re-routing to avoid traffic and self-drive cars are just around the corner. Volvo is currently testing 100 self-drive cars in Gothenberg; Google is going it alone following its initial JV with Toyota Prius to develop its own self-driving car and most major manufacturers have pilots underway. The Institute of Electrical and Electronics Engineers (IEEE) have estimated that up to 75 per cent of all vehicles will be autonomous by 2040.

Adaptive Analytics

Assurant, a US based insurance company, uses real-time predictive analytics in their call centres. They have found affinity patterns between customers and specific agents and they use these to route customers to individuals – they have found that matching accents, heritages and attitudes increases retention rates. And if the ideal agent is busy, the system calculates when other agents will be free and integrates the prediction with real-time affinity matching – the result is up to a 60 per cent improvement in customer service scores and retention. Extrapolate that 60 per cent improvement into dollar values and you can see the power of emotional analytics.

Personalised Content – Artificial Intelligence

Tesco in the UK are currently trialing the use of Occulus Rift to create a virtual supermarket. Customers navigate the supermarket using a headset - no need for them to actually visit a bricks and mortar store. Potentially each store could be tailored to the customer - custom products, custom promotions, custom look and feel. We could certainly trial new ‘stores’ using this technology – and in the future maybe customers could visit virtual branches without leaving their home?

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

Share

anzcomau:Bluenotes/technology-innovation,anzcomau:Bluenotes/technology-innovation/culture,anzcomau:Bluenotes/technology-innovation/digital,anzcomau:Bluenotes/technology-innovation/tech

The natives are restless – what does it mean when data natives replace digital natives?

2014-08-14