-

In Melbourne’s Docklands precinct, where the ANZ mothership is berthed, there’s dozens of small cafes and lunch spots. Almost all accept contactless card payments, the so-called “tap and go” system.

Recently a new, funky coffee joint opened, great coffee, interesting cakes, stylish – but it had a sign saying “$10 minimum” for card payments. Ignore, for the moment, there is no economic rationalisation for such limits, the only real decision is to accept or not accept.

But my colleague pointed out to the owners Docklands was home to not just two major bank HQs but a regional bank office and a major retailer’s head office. Coffee drinkers in the area – particularly coffee snobs – are early adopters of technology and hardly carried any cash. The café now happily takes tap and go, the proprietor accepts it’s a great technology which helps sales.

Yet there’s an odd phenomenon in Docklands: given the high usage of such cards, Docklands should be a hot bed of petty crime because, according to the Victorian Police, contactless payment cards are encouraging crims to target purses and wallets because of these cards which can be used for purchases up to $99 with no signature or PIN.

However, while detailed Docklands data is not available, local government sources I have spoken to said there was no evidence, anecdotal or otherwise, of more bag snatching, cars broken into or wallets taken. The hot beds for such activity remain certain crowded areas in the CBD.

The Victorian Police didn’t offer any evidence either and the official fraud data collated by the Australian Payments Clearing Association has nothing to support the argument. Yet the use of contactless cards is the fastest growing component of payments in Australia.

Now maybe the police have some anecdotal evidence from testimony by apprehended perps saying “yeah, I knocked off the old dear’s handbag because I suspected it may have contained a PayWave or PayPass card which I could use to buy $99 worth of coffees”. But they didn’t mention this.

To the extent data is available, it suggests fraud on such cards is actually lower relative to usage, probably because they are modern chip cards and so can’t be illegally copied or “skimmed” by crims and used for much bigger illegal transactions or to obtain actual cash.

The NSW police have said they haven’t seen any evidence of increased card fraud due to contactless payments. According to Visa, the contactless fraud rate has declined over the last 12 months and is half the rate of other “card present” – ie not online - fraud in Australia.

According to MasterCard, they "have met and held several discussions with the Victorian Police Fraud Squad since they first raised this issue publically a few months ago. As both MasterCard and industry data reveals no increase in fraud specifically relating to contactless technology, we have asked Victorian Police to clarify the source and nature of their crime statistics relating to contactless fraud."

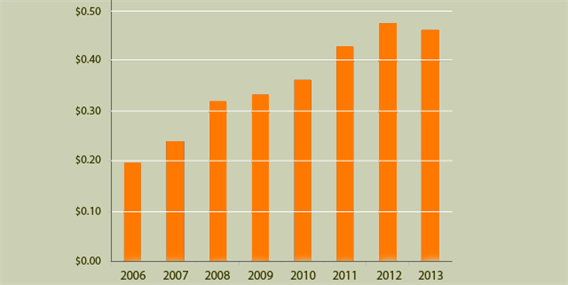

Fraud per $1,000 on Australian payment cards (12 months to 30 June) Source: APCA

{CF_IMAGE}

As consumers, we make risk and reward decisions constantly during the day. They’re not conscious but we decide whether a merchant looks reliable, can they be trusted with a card, a myriad of choices. The most obvious one we make is how much cash to carry.

Cash of course can’t be traced or replaced. A fraudulent card transaction in the vast majority of cases is not borne by the owner of the card but by the issuer of the card (or in some cases, particularly with some online transactions) by the merchant.

(Online fraud is certainly growing but of course tap-and-go transactions can’t be made online.)

More and more, people are choosing to carry less cash. That’s due to security concerns but also convenience. Cash has to be withdrawn, from a bank, an ATM or via an Eftpos cash withdrawal.

ATM usage is a good proxy for the desire to carry cash. According to APCA, Australian ATM usage is declining faster than most developed countries while tap-and-go payments are understood to be growing around 30 per cent per annum. ATM transactions have peaked. In 2013, the monthly volumes of ATM withdrawals fell about 5 per cent to $67.7 million, according to APCA.

Meanwhile, there was a 7 per cent growth in credit card transactions and a 14 per cent growth in debit card transactions over 2013.

Tap-and-go replaces cash. The average transaction size is lower even than a debit transaction.

As a cadet journalist with the old Melbourne Sun News Pictorial, I did my fair share of police rounds stints and the underlying causes of petty crime were always the same: the perps were opportunistic and after cash or items that could easily be turned into cash.

As Visa notes “the attraction of a low value purchase card using contactless is not consistent with the drivers of fraud perpetrators looking for high value saleable items”.

You can’t make a tap-and-go cash withdrawal. Cybercrime of course is a different and far more serious matter. Organised crime aims to systematically obtain large sums of money, corrupting whole tranches of transactions.

APCA chief Chris Hamilton has said when signatures finally are removed as an authorising protocol for credit cards, making PINs mandatory for larger transactions, there may be a blip in old school theft - as there was in the United Kingdom - as the crims look to replace the business case for skimming.

(BlueNotes carried a recent comprehensive explanation of the shift away from signatures by Lance Blockley who lead the project.)

Chip cards can’t – yet – be skimmed, only the old fashioned magnetic stripe.

Victoria Police Commissioner Ken Lay argued the banks were not concerned enough about tap-and-go driven petty crime because they saw it as a cost of doing business. Yet the logic here is unclear: costs are one of the major focuses of all banks in the current low growth environment. While banks do write off bad debts as a matter of normal business that hardly means they are not trying to reduce them.

Any reduction in the cost of doing business is something card issuers have a very clear incentive to pursue.

There is a broader social amenity in this debate as well: cash has costs.

Some retailers and consumers tend to assume non-cash payments have a fee and cash doesn’t. This is simply wrong.

MasterCard has done extensive research on the costs of cash in recent times and while the card scheme may have a vested interest, the thrust of the research has been widely replicated and indeed is obvious when considered.

Merchants only receive credit for cash when it is actually banked. There are transport and security risks with carrying cash. Cash restricts sales - consumers with cards are more likely to make an extra purchase. And cash is readily pilfered.

For society as a whole, cash has a cost because it facilitates the black economy. Tax avoidance is much easier with cash. Organised crime is not typically a big merchant base for American Express or Visa.

It may be that the Victorian Police has some extra data which demonstrates trends seen elsewhere in Australia and the world are not applying in Victoria. It should release that data and evidence as it is something the participants in the payments business would no doubt want to respond to – because they have a profit incentive, not just in lower bad debts but in reassuring a public already pre-disposed to replace more and more cash transactions with a card that the risks and rewards are known.

There’s ample opportunity to share this information. There’s the Interbank Forum which meets every 3 to 4 months with participants from financial institutions and law enforcement across Australia. There’s also the APCA-organised Law Enforcement and banks meeting every 3-4 months with participants including APCA and superintendent level law enforcement.

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

-

Share

anzcomau:Bluenotes/business-finance,anzcomau:Bluenotes/business-finance/your-money,anzcomau:Bluenotes/business-finance/payments,anzcomau:Bluenotes/business-finance/tech

Do crims tap-and-go?

2014-06-09